Download

1 / 7

80 likes | 218 Views

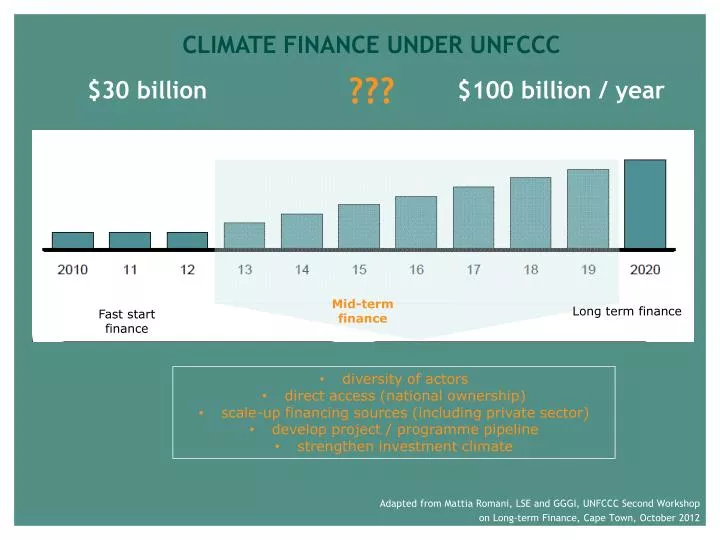

CLIMATE FINANCE UNDER UNFCCC. ???. $30 billion. $100 billion / year. Mid-term finance. Long term finance. Fast start finance. diversity of actors direct access (national ownership ) scale-up financing sources (including private sector) develop project / programme pipeline

E N D

CLIMATE FINANCE UNDER UNFCCC ??? $30 billion $100 billion / year Mid-term finance Long term finance Fast start finance • diversity of actors • direct access (national ownership) • scale-up financing sources (including private sector) • develop project / programme pipeline • strengthen investment climate Adapted from Mattia Romani, LSE and GGGI, UNFCCC Second Workshop on Long-term Finance, Cape Town, October 2012

Beyond 100 billion…OECD, McKinsey, WEF and others ‘sizing’ the investment gap…

What are the tools used by the public sector to mobilize the private sector?

Climate finance discourse • ‘tools to mobilise the private sector’ • ‘innovative instruments to leverage private capital’ • ‘de-risking tools to catalyse private capital’ • ‘investment grade national policy frameworks' • ‘supportive business environments’ • ‘smart targeted public sector interventions’ GREEN

Developing country subsidies dwarf climate finance • For the 42 developing countries where data is available, the volume FFS to consumers is 75 times that of climate finance • US$396 billion in FFS in 2011 vs. • US$5 billion avg. annual CF (2010-2012) • 5countries appear in both ‘top 12 lists’ (India, Indonesia, China, Mexico, and Egypt) • Recipients of climate finance and providers of fossil-fuel subsidies to consumers

Next steps and recommendations • It is critical that national level diagnostics, which seek to assess the ‘investment climate for climate investments’ directly include subsidy assessment(ie. Climatescope etc.) • ODI will be developing diagnostic approaches / methodologies as it expands its work on national climate finance analyses to include reviews of fiscal policies and subsidy regimes • This diagnostic work could be further supported by: • incorporating a broader range of subsidies in the reporting templates of the UNFCCC • support developing countries in undertaking subsidy estimation using climate finance – include this as part of exercises in ‘climate finance readiness’ • require diagnostic prior to disbursingbilateral and multilateral climate finance • EF Review / EF Reform NAMAs or LEDS • The G20, UNFCCC and IMF have examined links between subsidy reform in developed countries and climate finance. Greater understanding is needed on how subsidy reform can also drive energy / carbon pricing in developing countries and generate potential new domestic sources of climate finance.

“There is wide agreement on the central role that fiscal instruments must play if we are to address climate change effectively and efficiently.”Christine Lagarde, IMF, 2012“The world’s top priority must be to get finance flowing and get prices right on all aspects of energy costs to support low-carbon growth…end harmful fuel subsidies globally.”Jim Yong Kim, WB, 2013