Download

1 / 40

400 likes | 423 Views

22. Savings, Interest Rates, and the Market for Loanable Funds. Previously. CPI is the foundation of inflation calculation Computation can be difficult because the typical “ basket ” of consumer goods changes over time The BLS tries to adjust for this

E N D

22 Savings, Interest Rates, and the Market for Loanable Funds

Previously • CPI is the foundation of inflation calculation • Computation can be difficult because the typical “basket” of consumer goods changes over time • The BLS tries to adjust for this • Inflation is often misunderstood by the general public • There are several macroeconomic costs from inflation • Inflation is caused and controlled by expansions of a nation’s money supply

Big Questions • What is the loanable funds market? • What factors shift the supply of loanable funds? • What factors shift the demand for loanable funds? • How do we apply the loanable funds market model?

The Loanable Funds Market—1 • Loanable funds market • Includes such places as: • stock exchanges • investment banks • mutual fund firms • commercial banks • Borrowers use funds for businesses • Savers lend to businesses

Production Timeline:Firms Need to Borrow Firms need to borrow before production begins. That is why the loanable funds market is so important. Prepare to Produce Produce Sell Output Borrow $$ Build Capital Goods Hire Workers Repay Loans $$ Pay Workers $$ Time Today Future Periods

Notes about Borrowing • Every dollar borrowed requires a dollar saved • Lenders can’t lend money they don’t have • Savings provides funds for lenders to lend • Chain of borrowing: Savings → Borrowing → Investment → GDP • The loanable funds market makes this process efficient

Interest Rates • Interest rate • The price of loanable funds • Savers: the reward for saving • Borrowers: the cost of borrowing • Like other prices, it rises and falls • Affected by supply and demand • We can examine this market like any other market

Interest Rates and the Supply of Loanable Funds • When you save money, you are supplying funds. • The price you receive in return is the interest • Percentage (rather than dollars) • Example: • Interest rate = 3% per year • $500 ×0.03 = $15 • Saving $500 will pay $15 for the year • Loanable funds “law of supply” • The quantity of savings rises when the interest rate increases

Higher Interest Rates Yield Greater Future Returns This table represents the future value of $500 in savings at different interest rates. The interest rate is a reward for saving money.

Practice What You Know—1 • Where does the supply of funds in the loanable funds market come from? • Banks printing money • Firms borrowing money for investment • Government tax revenues from citizens • Consumers saving their money at banks

Interest Rates as a Cost of Borrowing • Interest rate on the demand side • Interest rate is the cost of borrowing • When should a firm borrow? • Do a cost-benefit analysis • Borrow funds if: Expected return on investment > Interest rate on loan

Practice What You Know—2 • The interest rate can be thought of as: • the rate at which banks loan funds. • the return on a capital investment. • the real rate of inflation. • the price of money.

Inflation and Interest Rates • Real interest rate • The interest rate corrected for inflation • Nominal interest rate • The interest rate before it is corrected for inflation • Fisher equation • Relates inflation to the real and nominal interest rate

Quick Summary • Supply of loanable funds • Comes from people saving money • Interest rate is a reward for saving • Demand of loanable funds • Comes from people wanting to borrow money • Interest rate is the cost of borrowing

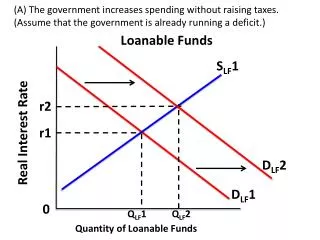

What Factors Shift the Supply of Loanable Funds? • Movement along the supply curve for loanable funds • Caused by a change in the interest rate • Shiftin the supplyof loanable funds is caused by • Changes in income and wealth • Changes in time preferences • Consumption smoothing

Shifts in the Supply of Loanable Funds—1 • Changes in income and wealth • Increases in income generally increase savings • Time preferences • People generally prefer goods sooner rather than later, and funds are no different

Time Preferences—1 • Time preferences are not uniform across individuals and societies • Less patient people prefer now to later and will save less • Time preferences help determine the savings rate

Time Preferences—2 • Application: Decision to attend college • Option 1: Get a job • Earn income immediately • Consume now • Option 2: Go to college • Forego current income and consumption • Higher future income and consumption

Practice What You Know—3 • How will an increase in time preferences affect the loanable funds market? There will be a(n): • increase in the supply of loanable funds. • decrease in the supply of loanable funds. • increase in the demand of loanable funds. • decrease in the demand of loanable funds.

Shifts in the Supply of Loanable Funds—2 • Consumption Smoothing: • No large changes in consumption with changes in income • Income changes over the course of the typical lifetime

Practice What You Know—4 • In the basic consumption-smoothing model, when are consumers dissaving? • During prime earning years • In their 20s and 30s • Very early in life • Late in life

Demand for Loanable Funds • Demanders of loanable funds are borrowers • Demand is driven largely by firms that need to borrow for large capital projects • Governments also borrow • Recall: • Borrowing must occur to build capital goods • This occurs before any production of final goods

What Factors Shift the Demand of Loanable Funds? • Movement along the demand curve for loanable funds • Caused by a change in the interest rate • Shift in the demand of loanable funds caused by • Changes in the productivity of capital • Changes in investor confidence

Shifts in the Demand for Loanable Funds—1 • Productivity of capital • If capital becomes more productive, the demand for loans will increase • The returns on investment (at any interest rate) will be greater • Example: Internet and computers • Investor confidence • If a firm is optimistic, it will borrow more today • Changes in capital productivity and investor confidence will shift the demand for loanable funds

Equilibrium in the Market for Loanable Funds—2 • In equilibrium: Savings = Investment • Supply of loanable funds is savings • Demand for loanable funds is firms wanting to borrow • Relationship between saving and borrowing • Every dollar borrowed requires a dollar saved

Practice What You Know—5 • What is true about equilibrium in the market for loanable funds? • Savings = Investment • Interest rate = Inflation • Investment = Interest Rate • Savings = GDP

Decline in Investor Confidence—1 • Investor confidence tends to decline when the economy slows • Firms expect reduced sales, and investors expect lower returns on their investments • Model predicts that this will result in a lower level of investment and a lower interest rate • Investment fell during both U.S. recessions between 2000 and 2012

Future of the Loanable Funds Market in the United States • Fall in the savings rate over past 30 years • Increase in time preferences • Leftward supply shift in loanable funds market • Foreign savings in United States could shift supply back to the right • Retirement of baby boomers • Another reason to believe there will be a leftward shift in the supply of funds • Result could be less investment and reduced GDP growth

Conclusion—1 • Loanable funds markets channel funds from savers to borrowers • Supply of loanable funds: household savings • Suppliers provide funds for firms to expand through investment, which is crucial for economic growth • The quantity of loanable funds supplied is positively related to the interest rate. • Supply increases with income and wealth but is also impacted by consumption smoothing and time preferences.

Conclusion—2 • Demand for loanable funds: loans to firms • Firms borrow to invest in capital that aids in production of future GDP • The quantity of loanable funds demanded is negatively related to the interest rate. • Demand increases with capital productivity and investor confidence. • Equilibrium in this market determines the level of savings, investment, and interest rates.