Download

1 / 28

280 likes | 458 Views

Chapter 3 Criteria for the Regulation of Financial Reporting and the Conceptual Framework. Lecture Topics. Company disclosures Objectives of financial reporting The conceptual framework Applying the conceptual framework to financial reporting issues. Lecture References.

E N D

Chapter 3 Criteria for the Regulation of Financial Reporting and the Conceptual Framework

Lecture Topics • Company disclosures • Objectives of financial reporting • The conceptual framework • Applying the conceptual framework to financial reporting issues

Lecture References • Text - Chapter 3 • SACs - 1, 2, 3 and 4

Key Concepts • Stewardship • Accountability • Conceptual framework • Reporting entity • General purpose financial reports (GPFRs) • Qualitative characteristics

The Nature of Company Disclosure • Rationale for mandatory corporate disclosure • Public interest • Protection of members • Predicting investment returns • Stewardship

The Nature of Company Disclosure • Regulated by: • Corporations Act • ASX listing rules • Accounting Standards • SACs • UIG Abstracts

The Nature of Company Disclosure • Compulsory reporting • Decision usefulness • Self-interest of profession • Accountability Information overload !??

Objectives of Financial Reporting and the Corporations Act • Quality of information • Corporations Act • True and fair view • Financial position • Financial performance

The Conceptual Framework • The reporting entity and GPFRs • Information needs of users • Accountability relationship • separation of ownership and control • economic and political importance • financial characteristics • Role of SACs

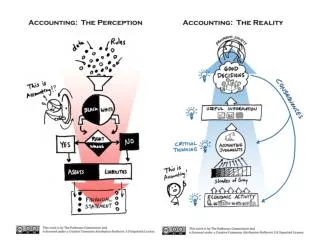

evaluations assists Reports on decision- making Financial Performance and the Accountability Relationship performance financial position GPFR’s investing financing compliance

The Conceptual Framework • The role of SACs • Requirements for GPFRs • non-mandatory • Special purpose financial reports • do not specifically address

The Conceptual Framework • Classification of entities • Reporting entity - SAC 2 • listed corporation • borrowing corporation • some foreign owned/controlled entities • other entities where users need GPFRs • Other entities

The Conceptual Framework • Relationship between qualitative standard and qualitative characteristics • Qualitative Characteristics - SAC 3 • Relevance • Reliability • Materiality • Comparability • Understandability

The Conceptual Framework • Qualitative characteristics and development of accounting standards • Elements of financial reporting • Recognition • Defining the elements

The Conceptual Framework • Elements of Financial Reporting SAC 4 • Assets • Liabilities • Owner’s Equity • Revenues • Expenses • Contributions • Distributions

The Conceptual Framework • Assets • Future economic benefits • Controlled by the entity • Resulting form past transactions or other past events

The Conceptual Framework • Liabilities • Future sacrifices • Of economic benefits • The entity is presently obliged • To make to other entities • Resulting from past transactions or events

The Conceptual Framework • Owner’s Equity • The residual interest • In the assets of the entity • After deduction of its liabilities

The Conceptual Framework • Revenues • Inflows or other enhancements • Or savings in outflows • Of future economic benefits • That increase assets or reduce liabilities • Other than contributions by owners • That increase equity

The Conceptual Framework • Expenses • Consumption or losses • Of future economic benefits • That decrease assets or increase liabilities • Other than distributions to owners • That decrease equity

The Conceptual Framework • Contributions • Future economic benefits • Contributed by external parties • That do not result in a liability • That give rise to a financial interest in the net assets • That conveys entitlement and/or • Can be sold/transferred/redeemed

The Conceptual Framework • Distributions • Future economic benefits • Distributed by the entity • To all or some of its owners • As a return on investment, or • As a return of investment

The Conceptual Framework • SAC 4 and capital maintenance • The nature of capital maintenance • relevance to ‘profit’ • capital maintenance adjustment • purchasing power • capital maintenance models • SAC 4

The Conceptual Framework • Use in accounting standards • Measurement • Balance sheet and income statement emphasis and matching • International comparability

Conceptual Framework • Applying the conceptual framework to financial reporting issues • Provides a context • Normative theory base • Identifies inconsistencies • Resolves disputes about practice

Conceptual Framework • Benchmarking Financial Reporting Practice • Between reporting practices • With reporting frameworks • Appropriate benchmark • Empirical • Normative

Conceptual Framework • The Corporations Act and the Reporting Entity • Differential reporting and disclosing entities • Approach to the study of financial reporting • Continual questioning • Recognition and measurement of elements

Where to get more information • Other courses • List books, articles, electronic sources