Download

1 / 13

130 likes | 309 Views

US Wireless Market Mid Year Update. US Wireless Market – Mid Year Update.

E N D

US Wireless Market – Mid Year Update • US wireless data market is growing at an impressive rate. Top 4 US carriers (Cingular, Verizon, Sprint Nextel, and T-Mobile) accounted for over $6.3B in wireless data revenues for the first half of 2006. Overall, wireless data service revenues exceeded $7B and the figures are likely to exceed $15B for the year 2006. This is almost a 75% jump from end-of-2005 number of $8.6B. The growth rate slowed down only slightly from 2004-2005 growth rate of 87%. SMS and data transport still drives bulk of data revenues but their percentage share is declining. • Among the top 4 US carriers, Verizon has made the most impressive strides in the last 4 quarters, increasing their wireless data revenues by a whopping 114%. Next Sprint with 71%, T-Mobile with 65%, and Cingular with 54% also netted impressive gains. • Verizon became the first US carrier to net over $1B in wireless data revenues in a quarter. Cingular was close second with $979M and Sprint with $935M are likely to cross the $1B mark next quarter. • Sprint retains its leadership position of highest wireless data ARPU in terms of absolute dollar amount at $7.25 but lost its number one spot in the % data ARPU to Verizon which now leads the US carriers at almost 13%. Average data ARPU is now $6.3 or 12%. • Overall ARPU (voice + data) increased slightly from Q106 but declined $0.27 from Q405. The general trend is towards slow decline. Data revenue is barely keeping up with the decline in voice ARPU. On an average voice ARPU has declined 8% from a year ago and data ARPU has increased 48%. Average Overall ARPU was $53.04. Sprint led with $62 followed by T-Mobile at $51, Verizon at $49.7, and Cingular with $48.4. • If the current trends hold, Verizon Wireless is likely to surpass Cingular Wireless as number 1 US carrier by Q307. • US had about 7M 3G subscribers by Q206, primarily from Verizon and Sprint Nextel. With Cingular joining the fray, the 3G growth is expected to accelerate with 2007 being the inflection year. • US wireless subscriber penetration stands at approximately 74% and is likely to exceed 78% by the end of the year. • Top 4 carriers added 12.7M subscribers from Jan-Jun 2006. • The top 4 US carrier account for 79% of the subscribers, 86% of the service revenues, and approximately 95% of the wireless data revenues. • US Off-net revenues for the year are likely to exceed $750M. • Data ARPU of CDMA/EV-DO carriers was 20% higher than GSM/WCDMA carriers.

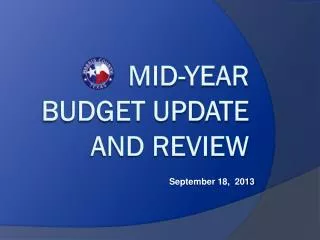

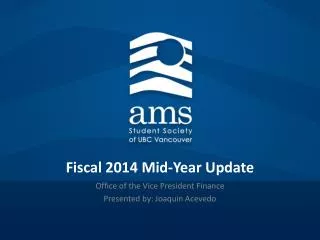

US Wireless Market – Mid Year Update • Several high-profile MVNOs were also launched in the last few months and the overall results have been disappointing primarily due to poor execution, instant crowding effect, and competition from big 4. • US wireless carriers are steadily climbing in their wireless data performance as compared to their peers worldwide. Verizon, Cingular, and Sprint ranked number 4, 5, and 6 respectively, amongst the top 10 operators worldwide in terms of total wireless data revenue generated for first half of 2006. • The #1 carrier worldwide in terms of total wireless data revenue for the first six months of 2006 is NTT DoCoMo which has maintained its position for a number of years. It is now generating almost $900M/month from wireless data revenues. • The top 10 carriers in terms of total wireless data revenues for 1H06 in order of rank are NTT DoCoMo, China Mobile, KDDI, Verizon Wireless, Cingular Wireless, Sprint Nextel, O2 UK, Vodafone Japan, SK Telecom, and China Unicom. (6 Asian, 3 US, 1 Europe. Who says US is behind). Vodafone Germany, TMO Germany, and TMO US are also closing in. • All the top 10 carriers in the list exceeded $1B in data revenues for the first six months of 2006. China Mobile and China Unicom benefited from their huge subscriber base of 274M and 135M respectively while DoCoMo and KDDI did well because they are generating over $17 (or 28%) in wireless data ARPU. • The top 10 carriers accounted for almost $24B in wireless data revenues for the first six months of 2006. The top 10 carriers account for approximately 700M (or approx 28%) subscribers worldwide. • In terms of wireless investments, over $2.8B was invested in wireless related companies/startups from Jan-Jun 2006 (this figure jumped to $4.1B in July). Source: Rutberg. Mobile TV/Video, Mobile Personalization, Mobile Search and Advertising, Semiconductor, Carrier infrastructure, Device design and development are hot areas. M&A activity also picked up quite significantly. • WiMax industry got a big boost with almost $1B investment in Clearwire and due to Sprint Nextel’s announcement of WiMax deployment. Sigh of relief for Intel and Samsung. Puts pressure on Qualcomm. Maybe Intel will renegotiate with Clearwire. • Worldwide Handset market share: Nokia and Motorola dominated with 35% and 23% market share respectively. Samsung with 12% stands third. Source: iSuppli. Though Apple’s iPhone rumors have been clouding the market, it is Motorola which continues to lead in launching must-have handsets. Windows mobile is starting to make serious inroads in the handset market but performance issues and high price points deter mass market adoption.

Worldwide Handset Market share Data Source: iSuppli

Wireless Investments in 2006 Data Source: Rutberg

Clients About CSC • Over 12 years of wireless industry experience • Strategy, Product Planning, Intellectual Property, R&D • Wrote one of the first books on Wireless Internet (2000). Coauthored 2 more since then. Numerous articles and reports. • Advisor to leading companies and startups worldwide in the wireless industry on business, product, and IP strategy. chetan@chetansharma.com http://www.chetansharma.com Blog:aorta.wordpress.com