Download

1 / 18

2.09k likes | 10.43k Views

Valuation of shares. Need For Valuation of Shares. 1. At the time of amalgamation and absorption. 2 . When unquoted shares are to be bought or sold. 3. At the time of converting preference shares an d debentures into equity shares.

E N D

Need For Valuation of Shares 1. At the time of amalgamation and absorption. 2. When unquoted shares are to be bought or sold. 3. At the time of converting preference shares and debentures into equity shares. 4. Where a portion of shares is to be given by a member of proprietary company to another member as a member cannot sell it in the open market it becomes necessary to certify the fair price. 5. For the valuation of the assets of a finance or investment trust company.

6. At the time of assessment by the income tax authorities for the purpose of estate duty, capital gain, wealth tax and gift tax. 7. When a company is nationalised and the compensation is payable by the government. 8. When a company acquires majority of the shares of another company for the purpose of acquiring a controlling interest in another company. 9. When shares are pledged as a security against a loan.

10. At the time of paying court fees. 11. When shares are purchased by employees of a company to be kept by them during the tenure of their service. 12. At the time of purchase and sale of shares in private companies. 13. When partners hold shares of a company for ascertaining the amount to be distributed amongst them on dissolution of the firm. 14. For satisfying dissentient shareholders in the case of reconstruction of a company under section 494.

Factors affecting valuation of shares 1. The basic or principle factor in the valuation of shares is the dividend yield that the investor expects to get as compared to the normal rate prevailing in the market in the same industry. 2. Growth prospects of the company. 3. Demand and supply of shares. 4. The nature of the business of the company concerned. 5. Dividend policy of the company and percentage of dividend declared in the part. 6. Past performance of the company.

7. Govt. policies in relation to companies business. 8. Accumulated reserves of the company. 9. Economic climate. 10. The income yielding capacity of the company. 11. Size of the business. 12. Net Asset position of the company. 13. Availability of ready market for future sale. 14. Management of the company. 15. Prospects of bonus or right issue. 16. Political factors prevalent peace and prosperity in the country and governments attitude towards the industry.

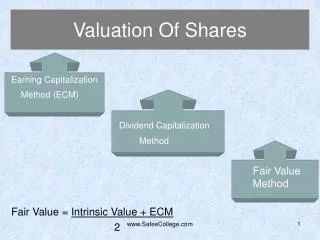

Methods of valuation of shares • Net Assets Method or Intrinsic Value or Net worth Method. (1) Including goodwill (2) Excluding goodwill • Yield Method or Earning Capacity or Market Value Method • Fair Value Method

Method 1- Net Assets Method or Intrinsic Value or Net worth Method • The value of shares is calculated by dividing the net assets of the business by the no. of equity shares. • All the assets from the asset side of balance sheet are summed up , then liabilities appearing on the liabilities side are deducted. Also less any probable loss or expenses . • The value arrived is the amount available for equity shareholders.

Points to remember- • Non-Trading assets such as investments should also be included. • Fictitious assets are excluded. • All the assets should be taken at their market value. • If preference share capital appears in the balance sheet then the total amount of preference share capital and the payment of any type of dividend in arrears on them should also be deducted from the total value of assets. • If Net Assets including goodwill is to be calculated, calculate the value of goodwill according to methods done earlier.

All Assets (Except fictitious assets) All Outside Liabilities Balance Preference Share Capital Any Dividend in arrears Net assets for equity shareholders XXX ( At realisable value, if give, otherwise at book value) (-) XXX XXX (-)XXX (-)XXX XXX

Merits • It is very simple and logical method for calculating the value of shares. • This method is mostly used by taxation authorities. • Present value of goodwill is also considered under this method. • As the net realisable value of assets is taken into consideration this method is useful for company going into liquidation. • Preference share capital is given preference over equity and deducted from assets like other liabilities.

Demerits • This method is not suitable for growing companies. • As goodwill is taken into consideration, it is difficult to calculate the value of goodwill. • This method leads to personal biasness as the market price of the asset is to be quoted which is very difficult to ascertain. • This method is not reliable one, as it includes the intangible asset such as goodwill, trademarks etc.

Method II-Yield Method or Earning Capacity or Market Value Method • Under this method the value of the shares are calculated on the basis of its prospective earnings. • Market value of assets and liabilities is not considered. • Value of shares is calculated by comparing the expected earnings of the company with normal rate of return on investment. • This method is based on the philosophy that shareholders values the return which he receives and not the earnings of the company.

1. Calculation of expected rate of return: • Profits available for dividend to equity X 100 Paid up equity share capital 2. Value of equity shares: • Expected rate of return X Paid up value of share Normal Rate of Return 3. Expected profits available for equity shareholders: Profits • Amount for tax charges • Amount to be transferred to reserves • Amount to be transferred to Debenture Redemption Fund • Preference Dividend if any

Valuation of minority and majority holdings Value of shares incase of majority holdings is ascertained by the method based upon the expected rate of earnings whereas incase of minority holdings the value of shares is better calculated by adopting expected rate of dividend rather than expected rate of earning, main reason being small investors are generally interested in the dividend rather than the expected rate of earnings. • Value of Share = Possible rate of Dividend X Paid up value of Share Normal Rate of Dividend

Merits • This method is most reasonably accepted because this method is based upon comparison between expected rate of return with normal rate of return. • This method is useful incase of minority holdings since they are interested in the profits earned by the company and dividends paid to them. • It is best suited to the company which is a going concern.

Demerits • Problems while selecting the normal rate of return. • Major drawback is that it doesn’t take into consideration the value of net assets of the company. • It is not suitable for the company which is going into losses for the past few years. • The method contains various difficulties while application of this method. • Predicting the future maintainable profits is quite difficult.

Method III- Fair Value Method Fair Value of Shares = Intrinsic value + Yield value 2 This method removes the disadvantages of both intrin.sic method and yield method