Download

1 / 18

190 likes | 411 Views

2. About the Australian Taxation Office. Net revenue collection of 232.6 billion*Operating budget of $2,533.2 million*21,511 staff nationally*67 sites across all states and territories*Currently in the midst of a Change Program incorporating a redesign of systems

E N D

1. Tax Office Fraud Control Planning: Tools and Techniques PRESENTED BY:

Annalissa Hilton

Fraud Prevention & Control

2. 2 About the Australian Taxation Office Net revenue collection of 232.6 billion*

Operating budget of $2,533.2 million*

21,511 staff nationally*

67 sites across all states and territories*

Currently in the midst of a Change Program incorporating a redesign of systems � integrating 120 existing systems into one interface

Policy initiatives designed to improve taxpayer interactions

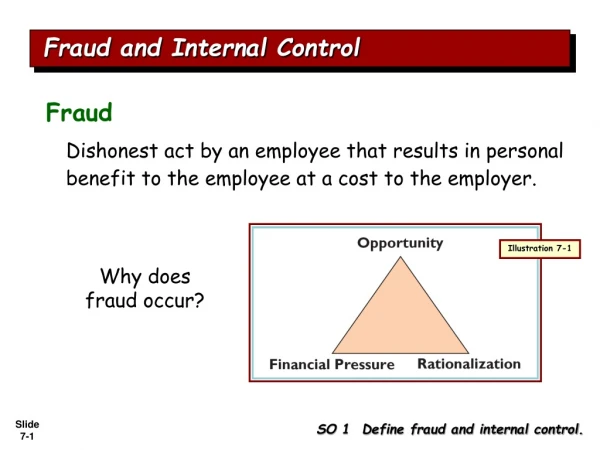

3. 3 Fraud in the Australian Taxation Office In the 2005-2006 financial year, we finalised 167 allegations of fraud and serious misconduct by employees.

29 of these cases were found to be substantiated.

This included:

two cases of unauthorised access, with one offender receiving community service and the other a fine

two cases of fraud against the revenue, with the severest penalty being four years and seven months imprisonment

A further 11 matters are either with the Commonwealth Director of Public Prosecutions or before the courts.

4. 4 Our fraud prevention strategy Governance framework

Integrity framework

Fraud awareness training

Security and privacy training

Internal investigations

Fraud control planning

5. 5

6. 6

7. 7 TOOLS AND TECHNIQUES

8. 8 Use of intelligence

Consolidation of intelligence from internal and external sources

Chief Knowledge Officer

Internal Audits

External Audits

Change Program design parameters

Previous Fraud Control Plans

External agencies

Professional bodies

Appointment of �Fraud Liaison Officers�

9. 9 Health Check Survey With the permission of the Audit Office of New South Wales, we have adapted the Fraud Health Check Survey from the Audit Office of New South Wales Fraud Control Improvement Kit Better Practice Guide to fit the Tax Office.

The Tax Office has an electronic system available to deliver the survey to all employees in a BSL and receive anonymous responses.

The results are depicted in a dashboard generated using the Excel spreadsheet tool provided by the Audit Office of NSW. The dashboard results are presented in the fraud control plan chapter for that BSL.

The survey offers the opportunity to obtain the fraud risk perceptions and any offered comments from all employees within the BSLs.

10. 10 Asymmetrically linked assessment methodology The ASLAM methodology considers both threat and risk assessment

This concept evolved from ASIO�s T4 threat assessment methodology

Allows for forecasting and the identification of environmental factors which can help to indicate a fraud is imminent

Allows for better understanding of a perpetrators intent and expectations, therefore allowing us to tailor internal awareness training strategies

11. 11 T4 model of threat assessment

12. 12 Facilitated workshops and interviews Provisional classification based on intelligence

Provides time to robustly assess high risk activities

More targeted approach to fraud threats

Testing provisional classification of functions

13. 13 Control Testing Proactive testing of control effectiveness

Three perspectives:

Recommendations reported as �implemented�

Control deficiencies identified through investigations

Hot topics (unauthorised access, proof of identity)

Every fraud control plan chapter is accompanied by at LEAST one control test

14. 14 Data Mining In 2006, the Reporting, Intelligence and Training team was established

Further expand on control testing to include proactive data mining of systems based intelligence

Responsible for most assessments within our Corporate Risk Fraud Control Plan Chapter

15. 15 Monitoring of recommendations Recommendations are reported quarterly to the Tax Office�s Audit Committee

Scrutiny of responses and the endorsement of mitigation strategies rest with the Fraud Prevention Group

Reporting feeds back into control testing

16. 16 We have learnt that: Facilitated assessment, while time consuming, creates a more consistent overall picture of the threats we face

A mixture of individual perspectives and concrete evidence provides a more rounded view of potential fraud threats.

Prescriptive process assessments allow for the retention of corporate knowledge

17. 17 The future Staffing

Getting the right people and retraining them

Developing in-house training

Responding to change

Gaining further advantages from the consolidation of intelligence

Benchmarking against international revenue agencies

�Like� agencies

Change Program environments

Similar systems

18. 18 Contact Annalissa Hilton

Fraud Prevention Group

Fraud Prevention and Control

Australian Taxation Office

annalissahilton@ato.gov.au

02 6216 3260