Download

1 / 14

E N D

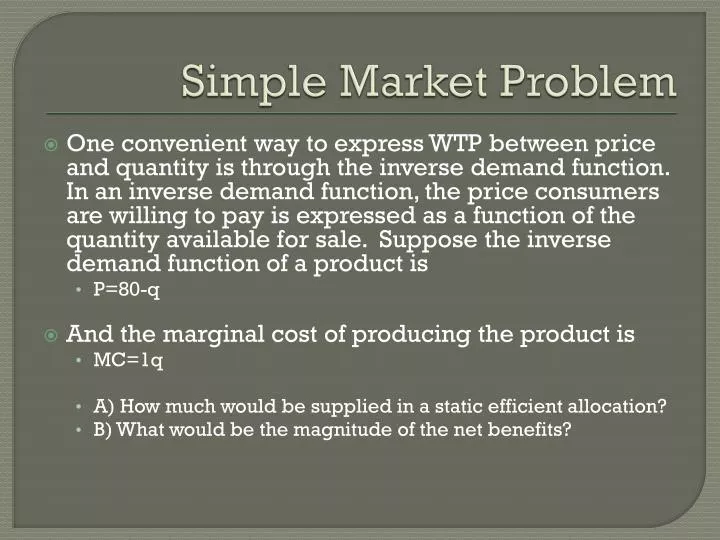

Simple Market Problem • One convenient way to express WTP between price and quantity is through the inverse demand function. In an inverse demand function, the price consumers are willing to pay is expressed as a function of the quantity available for sale. Suppose the inverse demand function of a product is • P=80-q • And the marginal cost of producing the product is • MC=1q • A) How much would be supplied in a static efficient allocation? • B) What would be the magnitude of the net benefits?

Market Equilibrium Price of Good Supply Equilibrium Price Demand Quantity of Good Equilibrium Quantity

Consumer Surplus Price of Good Supply Equilibrium Price Demand Quantity of Good Equilibrium Quantity

Producer Surplus Price of Good Supply Equilibrium Price Demand Quantity of Good Equilibrium Quantity

Total Welfare Price of Good Supply Equilibrium Price Demand Quantity of Good Equilibrium Quantity

Well-Defined Property Rights • Exclusivity – • All benefits and costs accrued as a result of owning and using the resources should accrue to the owner, and only the owner, either directly or indirectly by sale to others • Transferability – • All property rights should be transferable from one owner to another in a voluntary exchange • Enforceability – • Property rights should be secure from involuntary seizure or encroachment by others (ie. eminent domain)

Natural Resource Economics Negative Externalities – the negative impacts of a market transaction that affect those not involved in the transaction Positive Externalities – the positive impacts of a market transaction that affect those not involved in the transaction

Market Problem w/ negative externalities • Suppose the inverse demand function of a product is • P=80-q • And the marginal private cost of producing the product is • MC=1q • Suppose also that the production of this good produces a negative externality of $10 per unit produced. • A) What would be the market equilibrium? • B) What would be the socially efficient equilibrium? • C) What would be the net benefits under the market equilibrium? • D) What would be the net benefits under the socially efficient equilibrium? • E) What would external cost under the market equilibrium? • F) What would be the external cost under the socially efficient equilibrium?

Market with Externalities Price of Good Marginal Social Cost Marginal Private Cost P* Market Price Demand Quantity of Good Q* Market Quantity

Think How would you model a positive externality? Example, when Duncan Hines produces brownie mix, it pollutes a small amount of cocoa powder into the air. This makes the air smell like brownies, and increase the MSB from the production of brownies.

Steel Problem Consider the following supply and demand schedule for steel:

Steel Problem Pollution from steel production is estimated to create an external cost of sixty dollars per ton. Show the external cost, market equilibrium, and social optimum on a graph.

Steel Problem What kinds of policies might help to achieve the social optimum? How would this policy affect consumers? How would this policy affect producers? What effect would the policy have on market equilibrium price and quantity?

For next time, Finish reading Chapter 3 on the Pigovian tax and the Coase Theorem. Review the definitions of well-defined property rights.