Download

1 / 2

20 likes | 501 Views

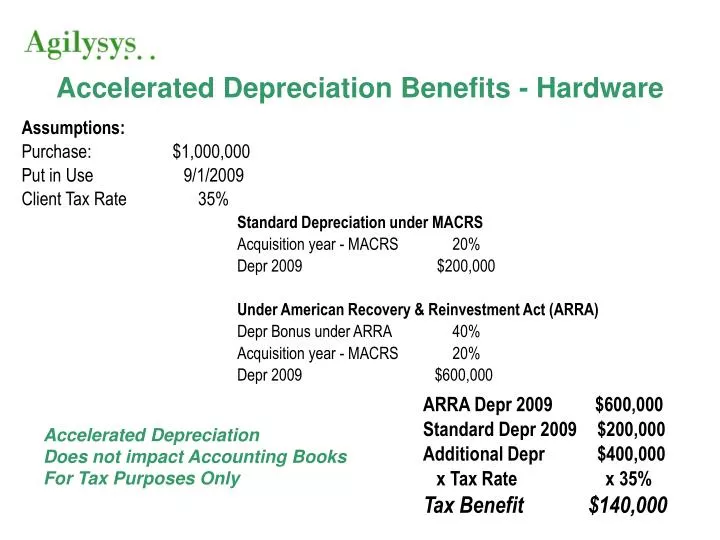

Assumptions:. Purchase:. $1,000,000. Put in Use . 9/1/2009. Client Tax Rate. 35%. Standard Depreciation under MACRS. Acquisition year - MACRS. 20%. Depr 2009. $200,000. Under American Recovery & Reinvestment Act (ARRA). Depr Bonus under ARRA. 40%. Acquisition year - MACRS. 20%.

E N D

Assumptions: Purchase: $1,000,000 Put in Use 9/1/2009 Client Tax Rate 35% Standard Depreciation under MACRS Acquisition year - MACRS 20% Depr 2009 $200,000 Under American Recovery & Reinvestment Act (ARRA) Depr Bonus under ARRA 40% Acquisition year - MACRS 20% Depr 2009 $600,000 ARRA Depr 2009 $600,000 Standard Depr 2009 $200,000 Additional Depr $400,000 x Tax Rate x 35% Tax Benefit $140,000 Accelerated Depreciation Benefits - Hardware Accelerated Depreciation Does not impact Accounting Books For Tax Purposes Only

Assumptions: Purchase: $1,000,000 Put in Use 9/1/2009 Client Tax Rate 35% Standard Depreciation - 36 month straight line Prorated for calendar year 4/36 Depr 2009 $111,111 11.1% of the purchase Depreciation Under American Recovery & Reinvestment Act (ARRA) Depr Bonus under ARRA 50% Proration of remaining 50% 4/36 (4/36 * 50% = 5.5555%) Depr 2009 $555,556 55.5% of the purchase ARRA Depr 2009 $555,556 Standard Depr 2009 $111,111 Additional Depr $444,444 x Tax Rate x 35% Tax Benefit $155,556 Accelerated Depreciation Benefits -Software Accelerated Depreciation Does not impact Accounting Books For Tax Purposes Only