Download

1 / 18

180 likes | 516 Views

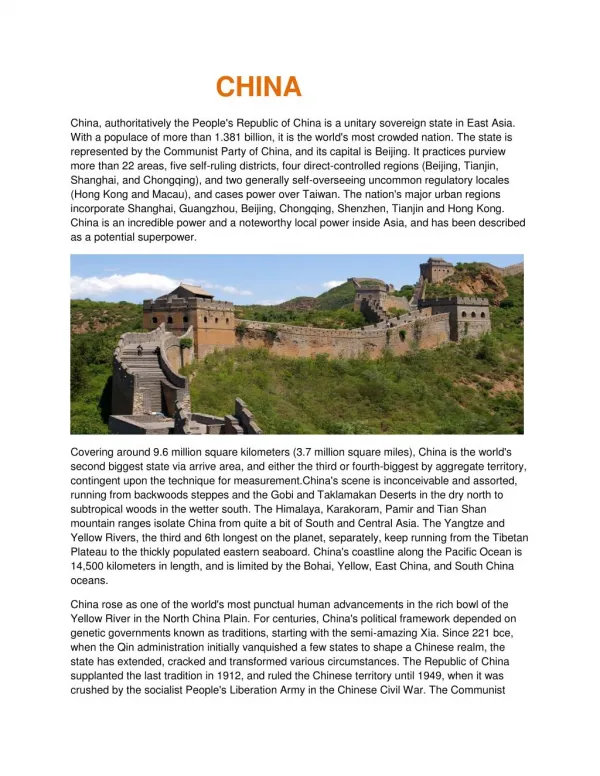

Politics and the Economy Dallas L. Salisbury President & CEO Employee Benefit Research Institute www.ebri.org Agenda The Economic Environment The Political Parties and Retirement The Candidates Conclusions US Double Dip Recession, Not Stagflation

E N D

Politics and the Economy Dallas L. Salisbury President & CEO Employee Benefit Research Institute www.ebri.org

Agenda • The Economic Environment • The Political Parties and Retirement • The Candidates • Conclusions

US Double Dip Recession, Not Stagflation • Mild, double-dip recession but slow recovery • Headwinds: Soaring energy and food prices; tighter financial conditions; housing recession; falling home prices; collateral damage to employment and output; capex weakness • Tailwinds: Monetary and fiscal stimulus; global growth still strong; pent-up capex demand • Temporarily higher inflation but not stagflation • Risks: Deeper downturn; stickier inflation; supply-induced energy shocks; broader-based deterioration in credit quality; earnings shortfalls

US Forecast at a Glance Source: Morgan Stanley Research, E = Morgan Stanley Research Estimates.

Global and Local Sources of US Inflation • Higher energy, food, nonoil import prices pushing headline inflation to 5-5½% • Domestic disinflationary forces should eventually win the tug of war with global factors pushing up inflation • Inflation tug of war • Longer-term inflation expectations rising, cyclical price hikes • Slipping operating rates will limit cost pass-through • Housing downturn to promote deceleration in OER

US Financial Conditions Have Tightened • Four dimensions to financial conditions: Rates, asset prices, credit, and the dollar • Credit spreads widening and standards are tightening • Re-intermediation of the banking system • Central banks addressed the liquidity crunch; is it over? • Sinking credit quality now driving spreads • Changes in financial conditions affect the economy with a lag

US Housing Recession Poised to Last at Least Until 2009 • Affordability rising sharply from 17-year low, but … • Scant pent-up demand • Still-high inventories of unsold homes • Lending standards will tighten further, down payments will stay high • Single-family activity to contract by 25+% • Collateral damage: Employment, home prices

A Perfect Storm for US Consumers • Employment sliding • Softening wage gains and soaring energy and food quotes will undermine “core” income • Home prices likely will decline by an additional 10% nationwide • Wealth loss and single-digit returns require that consumers eventually rebuild savings • Mortgage resets: A smaller threat?

Medicare Parts B and D Costs as a % of Average Social Security Benefit 20102080 Premiums 12% 28% Cost Sharing 1844 TOTAL 30 72 Note: Does not include premium and cost sharing assistance received by certain low-income beneficiaries or the income-related portion of Part B premiums paid by high-income participants.

Federal Spending Under CBO’s AlternativeFiscal Scenario Percentage of Gross Domestic Product

Projected Spending on Health Care as a Percentage of Gross Domestic Product Percent

IRA’s best 401k if employer must be involved DB undesirable risk SSA insolvent – IA desired Equal $ limits for all Health access IRA’s last resort 401 k with DB features DB preferred SSA essential – IA as supplement Progressive limits Health provision The Political Parties and Retirement Republicans Democrats

Nothing on website Historical support for IRA expansion and SSA individual accounts Website section Protect Social Security Strengthen Retirement Savings Affordable Health Care Protect and Honor Seniors Keep SSA with no privatization Automatic retirement savings and low income matches The Candidates and Retirement McCain Obama

Conclusions • The economy in 2009 will dominate the new Administration. • The long term projections on SSA and Medicare will force action within 8 years. • Tax incentive levels will be a focus of either President. • Retirement will not be a front burner issue.

www.ebri.org and www.choosetosave.org Dallas L. Salisbury President and CEO Employee Benefit Research Institute www.ebri.org and www.choosetosave.org