Download

1 / 18

180 likes | 374 Views

Chapter 7.2 Savings Plans & Payment Methods. Savings Plans. Chapter 7.2. Applying for a Savings or Checking Account. Driver’s license number Social Security Number Home Address Phone Number Mother’s Maiden Name Employment Information. Types of Savings Accounts. Regular Savings Accounts

E N D

Savings Plans Chapter 7.2

Applying for a Savings or Checking Account • Driver’s license number • Social Security Number • Home Address • Phone Number • Mother’s Maiden Name • Employment Information

Types of Savings Accounts • Regular Savings Accounts • Certificates of Deposit • Money Market Accounts • US Savings Bonds Textbook page 203

Regular Savings Accounts • Passbook • Statement monthly or quarterly • Low minimum balance • Ease of withdrawal • Insured • Low rate of return

Certificates of Deposit (CD) • Savings option or alternative • Money is left on deposit for a stated period of time (term) to earn a specific rate of return. • Maturity Date – when money is available for you. • CD Portfolio (3 month, 6 month, 1 year) • Early withdrawal penalty, minimum deposit

Money Market Accounts • A savings account that requires a minimum balance and earns interest that varies from month to month. • Higher minimum balance required ($1,000) • Good rate of return • FDIC insured

US Savings Bonds • Low minimum deposit • Guaranteed by the government • Free from state and local taxes • Lower rate of return when cashed in before the bond reaches maturity date. • Example: • Megan graduated from high school and her aunt gave her a savings bond as a gift. Her aunt paid $250 for the bond, but it has a face value of $500. This means that if Megan keeps the bond until the designated maturity date, it will eventually earn enough interest to be worth $500 or more.

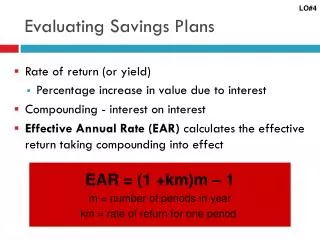

Evaluating Savings Plans • Rate of Return • Inflation • Tax Considerations • Liquidity • Safety • Restrictions and Fees

Rate of Return • Yield • The percentage of increase in the value of your savings from earned interest.

Rate of Return Example • Megan put the $100 she got on her birthday into a regular savings account last year, she earned $5 in interest. What was her rate of return? • Formula • Total Interest/Amount of Deposit = Rate of Return • Solution • $5/$100 = .05 or 5 percent

Compounding • The process in which interest is earned on both the principal and on any previously earned interest. • Multistep process • First, the interest on the principal is computed. That interest is added to the principal. The next time interest is computed, the new larger balance is used.

Compounding Annually Example • If Megan deposited $1000 in an account with a 3 percent annual interest rate that is compounded annually, how much interest will she earn after one year? • Formula • Principal x Annual Interest Rate = Amount of Interest Earned • Solution • $1000 x .03 = $30

Compounding Monthly Example • You deposited $1000 in a savings account. The bank is paying you 3 percent annually, which is compounded monthly. How much interest will you earn for the year? • Formulas • A. (Principal x Annual Interest Rate) /12 = Interest Earned for first month • B. (Principal + Previously Earned Interest) x Annual Interest Rate/12 = Interest earned for a Given Month

Compounding Monthly ExampleContinued 1. ($1000 x 3%) / 12 = $2.50 2. ($1002.50 x 3%) / 12 = $2.51 3. ($1005.01 x 3%) / 12 = $2.51 4. ($1007.52 x 3%) / 12 = $2.52 5. ($1010.04 x 3%) / 12 = $2.53 6. ($1012.57 x 3%) / 12 = $2.53

Compounding Monthly ExampleContinued 7. ($1015.10 x 3%) / 12 = $2.54 8. ($1017.64 x 3%) / 12 = $2.54 9. ($1020.18 x 3%) / 12 = $2.55 10. ($1022.73 x 3%) / 12 = $2.56 11. ($1025.29 x 3%) / 12 = $2.56 12 ($1027.85 x 3%) / 12 = $2.57 At the end of the year you will have $1,030.42 (1027.85 + 2.57 = 1030.42). You earned $27.85 in compounded interest for the year.

Truth in Savings(Federal Reserve Regulation DD) • Financial institutions have to inform you of the following information: • Fees on deposit accounts • Interest Rates • Annual percentage yield (APY) – amount of interest that a $100 deposit would earn, after compounding, for one year. • Based on the annual interest rate and the frequency of compounding. • Terms and conditions of the savings plan

Checking Accounts Chapter 7.2