Download

1 / 3

0 likes | 11 Views

Many Non-resident Indians (NRIs) might not know that they can jump into the exciting Indian market. It's not just about mutual funds - there are more ways for NRIs to start investing in India and make their money work in their home country, opening doors to more financial possibilities and security.

E N D

What are the Ways NRIs Can Invest in India? Many Non-resident Indians (NRIs) might not know that they can jump into the exciting Indian market. It's not just about mutual funds - there are more ways for NRIs to start investing in India and make their money work in their home country, opening doors to more financial possibilities and security. Ways NRIs Can Invest in India 1. Equities: NRIs can directly invest in Indian equities through the Portfolio Investment Scheme (PIS) route sanctioned by the Reserve Bank of India (RBI). This avenue offers a direct stake in the growth and performance of Indian companies, providing a comprehensive investment experience. 2. Mutual Funds: A versatile choice, Mutual Funds offer NRIs access to various categories such as Equity, Balanced, Bond, and Liquid Funds. Unlike direct equities, Mutual Fund investments do not necessitate PIS permission from the RBI. However, it's crucial to note that certain limitations apply to US and Canada-based NRIs due to reporting requirements under FATCA/CRS rules.

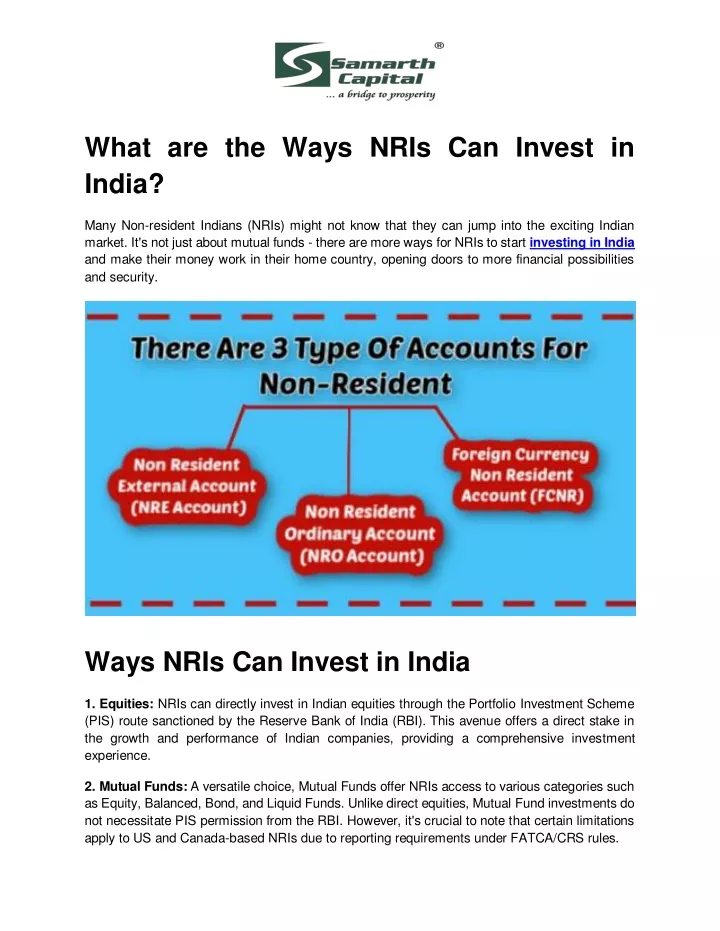

3. Government Securities: NRIs can venture into government securities on an NRE or NRO basis. While interest on NRE investments remains tax-exempt, NRO investments attract taxable interest, subject to withholding tax (TDS). 4. Fixed Deposits: Investing in fixed deposits of banks or Non-Banking Financial Companies (NBFCs) is another avenue for NRIs. Depending on the terms of the issue, investments can be made on both NRE and NRO bases. Interest on NRO deposits is taxable with TDS implications, whereas interest on NRE deposits remains tax-exempt. 5. Real Estate: NRIs have the opportunity to invest in residential and commercial properties in India. However, certain restrictions apply, barring the acquisition of agricultural land, farmland, or plantations. These restrictions don't extend to inheritance or gifts, offering flexibility in property ownership. 6. National Pension Scheme (NPS): A government-backed retirement savings plan, NPS operates under the EET tax structure (Exempt-Exempt-Tax). Contributions and accrued capital gains enjoy tax exemption, while withdrawals are subject to taxation. This cost-effective scheme is an ideal choice for NRIs planning to spend their retired life in India. Contributions to NPS can be made from NRE or NRO accounts, but the pension must be received in India and is non- repatriable. Types of Accounts For NRIs 1. NRE (Non-Resident External) Account: ○ For NRIs to park foreign income in India. ○ Fully repatriable, allowing funds to be taken back abroad. ○ Ideal for seamless international transactions. 2. NRO (Non-Resident Ordinary) Account: ○ For managing income earned in India. ○ Partially repatriable, with certain conditions. ○ Useful for local transactions and bill payments. 3. FCNR (Foreign Currency Non-Resident) Account: ○ Maintained in foreign currencies to curb exchange rate risks. ○ Fully repatriable, ensuring flexibility in moving funds. ○ Suitable for NRIs looking to retain foreign currency holdings.

Conclusion As NRIs consider their investment journey in India, Samarth Capital offers a diverse range of options from equities and Mutual Funds in India to real estate and more. NRIs can not only invest in India but also foster financial growth and security for the long term in their homeland. Email Id: samarthcapital@gmail.com Office Address: 13, Malad Ambika Premises, Upper Govind Nagar, Malad (E), Mumbai 400097 Mobile No: 9820331713