Download

1 / 21

210 likes | 350 Views

The Euro Crisis & Greece: 5 Mistakes Jeffrey Frankel Harpel Professor. MIT, Stata Center, room 32-155 5pm , Friday, Dec. 2 nd , 2011. 5 mistakes made by euroland’s leaders regarding Greece Slender rays of hope: The hour of the technocrats Proposals for the future.

E N D

The Euro Crisis & Greece: 5 MistakesJeffrey FrankelHarpel Professor MIT, Stata Center, room 32-155 5pm , Friday, Dec. 2nd, 2011

5 mistakes made by euroland’s leaders regarding Greece • Slender rays of hope: • The hour of the technocrats • Proposals for the future

5 mistakes made by euro leaders • Admitting Greece to the €, a country that was not ready. • Pretending to enforce the fiscal criteria: • The Maastricht criteria • “No bail out” clause • Stability & Growth Pact. • Allowing Mediterranean countries’ bonds spreads near 0 • helped by investors’ under-perception of risk (2003-07) • and artificial high credit ratings. But also • ECB acceptance of Greek bonds as collateral. When the crisis hit, the leaders buried their heads in the sand: • 2 years ago, sending Greece to the IMF was “unthinkable.” • 1 year ago, restructuring of the debt was “unthinkable.”

The Treaty of Maastricht (1991) surprised many economists by emphasizing fiscal criteria as qualifications for membership: BD < 3% of GDP & Debt < 60% of GDP. Why did the designers do it? • Theory I: Jason & the Golden Fleece • Theory II: Theseus& the stone • Theory III: Odysseus & the mast. Frankel, Economic Policy (London) 16, April 1993, 92-97.

The motivationfor the Maastricht fiscal criteria is clear • the same as for the No Bailout Clause • and the Stability & Growth Pact (1997): • Skeptical German taxpayers believed that, before the € was done, they would be asked to bail out profligate Mediterranean countries. • European elites adopted the fiscal rules to demonstrate that these fears were groundless.

After the euro came into existence • it became clear the German taxpayers had been right • and the European elites were wrong. • E.g., Greece persistently violated the 3% rule. • The large countries violated the rule too. • SGP targets were “met” by overly optimistic forecasts. • SGP threats of penalty had zero credibility. • Yet each year the ostrich elites stuck their heads deeper & deeper into the sands.

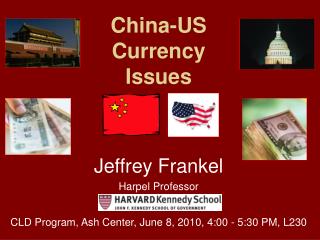

In most years, the true Greek budget deficit was far in excess of the supposed limit (3% of GDP). and yetthe official budget forecasts were always rosy. Until, in 2009, the bottom fell out of the budget. Source: Frankel & Schreger (2011)

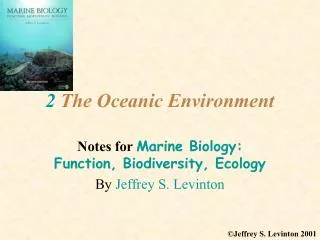

At the time of Maastricht, some economists had hoped that euro countries with deficits/debts would be kept in line, as U.S. states are, • esp. by an automatic market rise in interest rates, • with no expectation of federal bailout. • Alesina, et al (EP, 1992) and Goldstein &Woglom(1992). • Why didn’t that mechanism work?

Spreads help keep profligate US states in line= reason why no state has ever been bailed out by the Federal government, despite some defaults. Yield tomaturity in % 9 Source: W.B. English, „Understanding the costs of sovereign default …,“ p. 269. as used by Holtfrerich (2011)

California Municipal Bonds(now the lowest rated of the 50- states)Credit Default Swapshttp://blogs.reuters.com/muniland/2011/06/08/muni-sweeps-lockyer-rides-again/

Spreads for Italy, Greece, & other Mediterranean members of € were near zero, from 2001 until 2008. Market Nighshift Nov. 16, 2011

When PASOK leader George Papandreou became PM in Oct. 2009, • he announced • that “foul play” had misstated the fiscal statistics under the previous government: • the 2009 budget deficit ≠ 3.7%, as previously claimed, but > 12.7 % !

Missed opportunity • The euro elites had to know that someday a member country would face a debt crisis. • In early 2010 they should have viewed Greece as a good opportunity to set a precedent for moral hazard: • The fault egregiously lay with Greece itself. • Unlike Ireland or Spain, which had done much right. • It is small enough that the damage from debt restructuring could have been contained at that time. • Unlike Italy now, if the worst happens. • They should have applied the familiar IMF formula: serious bailout, but only conditional on serious policyreforms & serious PrivateSectorInvolvement.

But the ostriches stuck their heads ever further down in the sand. • There is even less reason now to think Brussels can impose fiscal constaints on borrowers or ask unlimited transfers from creditor country taxpayers than before.

Slender rays of hope, #1 • Greece, Ireland & Portugal did finally go to the IMF; Germany & banks did finally agree to write down Greek debt. • But it has always been much too little, too late. • The only solution for the short-term: • a lot more money • from ECB & • national governments, • conditional country-by-country on reforms + PSI.

Slender rays of hope, #2 • A government of technocrats under Mario Montiin Italy is a huge improvement over the disaster of Berlusconi. • Similarly Lucas Papademos in Greece • But he has been given even less freedom of action than Monti: his term is only 3 months and he wasn’t allowed to pick his cabinet.

Proposals for the future: #1 Emulate Chile’s successful fiscal institutions • Phrase budget targets in structural terms. • Give responsibility for determining what is structural to an independent professional agency, to avoid forecast bias.(Frankel, 2011)

Proposals for the future: #2 Penaltywhen a euro country misses its target: • The ECB then stops accepting new bonds as collateral. • => Sovereign spread rises, with automaticity. • Proposal from Brueghel(JvW & ZD): All of euroland is liable for blue bonds (issued up to SGP limits); Issuing country is liable for red bonds (beyond those limits) . • Blue bonds share advantages with other eurobond proposals: • ● ECB can conduct monetary policy. • ● They could offer an alternative to US TBillsfor PBoC & other desperate global investors

EMU Ostrich

References by the speaker • “The ECB’s Three Big Mistakes,” VoxEU, May 16, 2011. • “Optimal Currency Areas & Governance", slides session on the Challenge of Europe at the Annual Conference of George Soros’ INET, April 2011; video available, including my presentation. • "Let Greece Go to the IMF," Jeff Frankel’s blog, Feb.11, 2010. • Over-optimism in Forecasts by Official Budget Agencies and Its Implications," 2011, forthcoming in Oxford Review of Economic Policy. • “A Solution to Fiscal Procyclicality: The Structural Budget Institutions Pioneered by Chile,” Fiscal Policy and Macroeconomic Performance, Central Bank of Chile, 2011. NBER WP 16945, April 2011. • “The Estimated Effects of the Euro on Trade: Why are They Below Historical Evidence on Effects of Monetary Unions Among Smaller Countries?” in Europe and the Euro, Alberto Alesina & Francesco Giavazzi, eds. (U.Chic.Press), 2010. • "Comments on 'The euro: It can’t happen, It’s a bad idea, It won’t last. U.S. economists on the EMU, 1989-2002,' by L.Jonung & E.Drea," slides. Euro at 10: Reflections on American Views, ASSA meetings, San Francisco, 2009. • "The UK Decision re EMU: Implications of Currency Blocs for Trade and Business Cycle Correlations," in Submissions on EMU from Leading Academics (H.M. Treasury: London), 2003. • "The Endogeneity of the Optimum Currency Area Criterion" (with Andrew Rose), The Economic Journal, 108, no.449, July 1998. • “‘Excessive Deficits’: Sense and Nonsense in the Treaty of Maastricht; Comments on Buiter, Corsetti and Roubini,” Economic Policy, Vol.16, 1993.

Appendix: Blue bonds & red bonds Gavyn Davies, FT