Download

1 / 18

220 likes | 933 Views

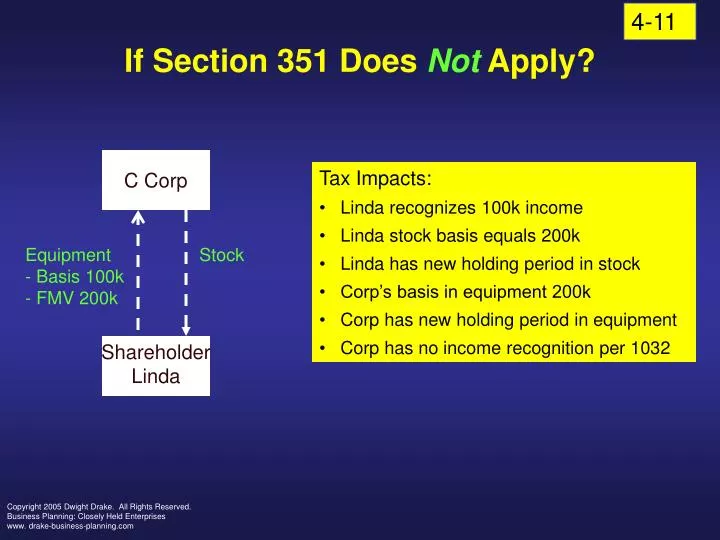

4-11. If Section 351 Does Not Apply?. C Corp. Tax Impacts: Linda recognizes 100k income Linda stock basis equals 200k Linda has new holding period in stock Corp’s basis in equipment 200k Corp has new holding period in equipment Corp has no income recognition per 1032.

E N D

4-11 If Section 351 Does Not Apply? C Corp • Tax Impacts: • Linda recognizes 100k income • Linda stock basis equals 200k • Linda has new holding period in stock • Corp’s basis in equipment 200k • Corp has new holding period in equipment • Corp has no income recognition per 1032 • Equipment • Basis 100k • FMV 200k Stock Shareholder Linda Copyright 2005 Dwight Drake. All Rights Reserved. Business Planning: Closely Held Enterprises www. drake-business-planning.com

4-12 Rule 1: The 351 Rule No gain or loss is recognized by the transferor on the transfer of property to a corporation in exchange for stock of the corporation if: 1. Property is transferred 2. Solely in exchange for stock 3. Transferor(s) in “control” “immediately after exchange. Two 80% requirements – 80% of all voting stock and 80% of total shares of all classes of stock. Example: XYZ Inc issues 100 share of its stock to its sole shareholder Jim for equipment worth 200k that has a basis of 100k. Jim recognizes no gain or loss on the exchange. Copyright 2005 Dwight Drake. All Rights Reserved. Business Planning: Closely Held Enterprises www. drake-business-planning.com

4-13 If Section 351 Does Apply? • Tax Impacts: • Linda recognizes no income (Rule 1) • Linda stock basis equals 100k (Rule 3) • Linda has tacked holding period in stock • (Rule 4) • Corp’s basis in equipment 100k (Rule 6) • Corp has tacked holding period in equipment • (Rule 7) • Corp has no income recognition per 1032 • (Rule 5) C Corp • Equipment • Basis 100k • FMV 200k Stock Shareholder Linda Note: Double basis impact trade-off for shareholder non-recognition.What is future impact? Copyright 2005 Dwight Drake. All Rights Reserved. Business Planning: Closely Held Enterprises www. drake-business-planning.com

4-14 Section 351 Eligibility Traps Trap Solution Stock for services Keep under 20% or have dual consideration and meet 10% standard of Rev. Proc. 77-37 Multiple transfers Document part of integrated plan at different times Subsequent stock sale Prohibit; require time lapse; no prearrangement; gifts generally not a problem Accommodation transfers Meet 10% threshold of Rev. Proc. 77-37 Subsequent corp property Consistent with ordinary business or insure sales time lapse and no pre-arrangement Nonvoting stock 80% of each class. Only direct ownership counts Nonqualified preferred Boot for income recognition purposes Investment company risk? Diversification issue is ballgame Copyright 2005 Dwight Drake. All Rights Reserved. Business Planning: Closely Held Enterprises www. drake-business-planning.com

4-15 Rule 2: The 351(b) Boot Rule If 351 would apply except that corporation issues property in addition to stock (“boot”) to the shareholder, then shareholder recognizes gain on the property transferred to corporation equal to the lesser of: 1. The built-in gain on the property transferred – the excess of FMV over basis 2. The FMV of boot received by the shareholder. Example: XYZ Inc issues 100 share of its stock and 80k cash to its sole shareholder Jim for equipment worth 200k that has a basis of 100k. Jim recognizes gain equal to boot – 80k. If 120k boot was paid by XYZ Inc in addition to stock, Jim would recognize gain equal to 100k – excess of 200k FMV over 100k basis. Copyright 2005 Dwight Drake. All Rights Reserved. Business Planning: Closely Held Enterprises www. drake-business-planning.com

4-16 Section 351 With Boot • Tax Impacts: • Linda recognizes 80k income (Rule 2) • Linda stock basis equals 100k (Rule 3) • Linda has tacked holding period in stock • (Rule 4) • Corp’s basis in equipment 180k (Rule 6) • Corp has tacked holding period in equipment • (Rule 7) • Corp has no income recognition per 1032 • (Rule 5) C Corp • Equipment • Basis 100k • FMV 200k Stock and 80k cash Shareholder Linda Copyright 2005 Dwight Drake. All Rights Reserved. Business Planning: Closely Held Enterprises www. drake-business-planning.com

4-17 Rule 3: The 358 Basis Rule If 351 applies to an exchange of property for stock in a corporation, the basis of the stock received by the shareholder equals: 1. The basis of the property transferred to the corporation in the hands of the shareholder, plus 2. Any gain recognized the shareholder ala the 351(b) rule, less 3. The FMV of any boot received. Example: XYZ Inc issues 100 share of its stock and 80k cash to its sole shareholder Jim for equipment worth 200k that has a basis of 100k. Jim recognizes gain equal to boot – 80k. Jim’s basis in stock is equal to 100k (basis in equipment), plus 80k gain less 80k boot = 100k. If 120k boot was paid by XYZ Inc in addition to stock, Jim would recognize gain equal to 100k. Basis in stock would equal 100k, plus 100k gain, less 120k boot = 80k basis. Copyright 2005 Dwight Drake. All Rights Reserved. Business Planning: Closely Held Enterprises www. drake-business-planning.com

4-18 Rule 4: The Shareholder Tacking Rule If 351 applies to an exchange of property for stock in a corporation, the holding period of the property transferred by the shareholder is “tacked on” to the holding period of the stock if the transferred property was a capital asset or a 1231 asset (asset used in trade or business). No inventories or receivables.: Example: XYZ Inc issues 100 share of its stock and 80k cash to its sole shareholder Jim for equipment worth 200k that has a basis of 100k. Jim’s holding period of equipment is “tacked on” in determining holding period of stock. Copyright 2005 Dwight Drake. All Rights Reserved. Business Planning: Closely Held Enterprises www. drake-business-planning.com

4-19 Rule 5: The 1032 Rule Corporation recognizes no gain or loss on receipt of money or property in exchange for its own stock Example: XYZ Inc issues 100 share of its stock and 80k cash to its sole shareholder Jim for equipment worth 200k that has a basis of 100k. XYZ Inc recognizes no gain or loss. Copyright 2005 Dwight Drake. All Rights Reserved. Business Planning: Closely Held Enterprises www. drake-business-planning.com

4-20 Rule 6: The 362 Rule A corporation’s basis in property acquired in exchange for its stock in a transaction that qualifies under 351 equals the shareholder’s basis in the property’s basis plus any gain recognized by the shareholder. But if net built-in loss, basis limited to FMV of property unless all elect to reduce stock basis of shareholder to FMV. Example: XYZ Inc issues 100 share of its stock and 80k cash to its sole shareholder Jim for equipment worth 200k that has a basis of 100k. Jim recognizes gain equal to boot – 80k. XYZ Inc.’s basis in equipment is 100k (Jim’s basis in equipment), plus 80k gain recognized by Jim = 180K. Copyright 2005 Dwight Drake. All Rights Reserved. Business Planning: Closely Held Enterprises www. drake-business-planning.com

4-21 Rule 7: The Corp Tacking Rule If 351 applies to an exchange of property for stock in a corporation, the holding period of the property transferred by the shareholder is “tacked on” in determining the holding period of the property in the hands of the corporation. Example: XYZ Inc issues 100 share of its stock and 80k cash to its sole shareholder Jim for equipment worth 200k that has a basis of 100k. Jim’s holding period of equipment is “tacked on” in determining XYZ Inc.’s holding period of equipment. Copyright 2005 Dwight Drake. All Rights Reserved. Business Planning: Closely Held Enterprises www. drake-business-planning.com

4-22 Rule 8: The Assumed Liability Rule General Rule: If corporation assumes liability of shareholder in 351 exchange: 1. Assumption not considered “boot” for gain or loss purposes. 357(a) 2. Assumption does reduce shareholder stock basis by debt amount. 358(d) Exception: Debt treated as “boot” for gain purposes if: 1. Tax avoidance purpose or not bona fide business purpose. Burden on taxpayer to prove by clear preponderance of evidence. 2. Debt exceeds basis of all property transferred to corp – then excess treated as taxable boot. Copyright 2005 Dwight Drake. All Rights Reserved. Business Planning: Closely Held Enterprises www. drake-business-planning.com

4-23 Section 351 With Assume Debt • Tax Impacts: • Linda recognizes 20k income (Rule 8) • Linda stock basis equals 0 (Rule 3) • Linda has tacked holding period in stock • (Rule 4) • Corp’s basis in equipment 120k (Rule 6) • Corp has tacked holding period in equipment • (Rule 7) • Corp has no income recognition per 1032 • (Rule 5) C Corp Stock and 120k debt assumed • Equipment • Basis 100k • FMV 300k Shareholder Linda Copyright 2005 Dwight Drake. All Rights Reserved. Business Planning: Closely Held Enterprises www. drake-business-planning.com

4-24 Section 351 Assumed Debt Traps Trap Solution Tax avoidance purpose Bad purpose taints all debt. Proof burden on taxpayer. Recent debts suspect. Lingering shareholder Leave no doubt as to parties’ expectations. Liability Nonrecourse debts Specify amount to be paid from outside assets. Amount should never exceed FMV. Future accountable debts Not debt for 351 purposes. Identity and exclude. Both deductibles (cash basis APs) and capital expenditures excluded. Rev. Rule 95-74 Basis pumping Helps to avoid debt in excess of basis problem. Will personal notes do job? The Peracchi impact. Copyright 2005 Dwight Drake. All Rights Reserved. Business Planning: Closely Held Enterprises www. drake-business-planning.com

4-30 Partnership Rules Comparison Corporate Partnership Rule 1: The 351 Rule 721: No gain or loss to partner and control requirement. But built-in gain allocated back to partner on sale per 704(c) Rule 2: The 351(b) Boot Rule Allocate portion of contributed property basis to Boot and treat Boot portion of transaction as sale or exchange. Reg. 1.707-3(f) Example 1. Rule 3: The 358 Basis Rule 722: Carryover basis plus any investment company gain recognized under 721(b). Copyright 2005 Dwight Drake. All Rights Reserved. Business Planning: Closely Held Enterprises www. drake-business-planning.com

4-31 Partnership Rules Comparison Corporate Partnership Rule 4: Shareholder Tacking Rule Same per 1223 (1) Rule 5: The 1032 Rule Same per 721 if for property Rule 6: The 362 Rule Same per 723, but no built-in- loss rule Rule 7: The Corp Tacking Rule Same per 1223(2) Rule 8: The Assumed Liability Rule New Game Copyright 2005 Dwight Drake. All Rights Reserved. Business Planning: Closely Held Enterprises www. drake-business-planning.com

4-32 Partnership Liability Game 1. 752 Upside Twist: Increase in partner’s share of partnership’s liabilities deemed contribution of money to partnership. Basis increase. 2. 752 Downside Twist: Decrease in partner’s share of partnership’s liabilities deemed money distribution. If money distribution exceeds basis before distribution, then gain recognized to extent of excess per 731. No negative basis. 3. Recourse liability allocation: Allocated to partners according to how partners agree to bear ultimate risk for liability. 4. Non-recourse liability: Allocated to partners according to profits interests with some flexibility. But if property contributed with NR debt in excess of basis, debt first allocated to contributing partner to amount of gain allocated to such partner under 704(c) if property sold for debt. Copyright 2005 Dwight Drake. All Rights Reserved. Business Planning: Closely Held Enterprises www. drake-business-planning.com

4-33 Partnership Capital Interest For Services Capital Interest:An interest that gives service partner a share of the partnership’s existing capital and future profits. A profits interest only gives share of future profits. Test: If partnership liquidated now, would service partner get anything? Triple Impact:Capital interest for services 1. Partner has section 61 compensation income equal to FMV of interest, subject to section 83 game. 2. Partnership gets section 162 deduction in same amount, allocated to existing partners (not new partner) 3. Existing partners may share gain equal to FMV of interest transferred over allocable basis of each partner. Deemed sale from existing to new. Proposed Regs would eliminate deemed sale Copyright 2005 Dwight Drake. All Rights Reserved. Business Planning: Closely Held Enterprises www. drake-business-planning.com