Download

1 / 3

40 likes | 254 Views

Here is a summary of what is Letter of Credit and how to apply for, including the documents & difficulties that the buyer and seller face to realise LC.<br>

E N D

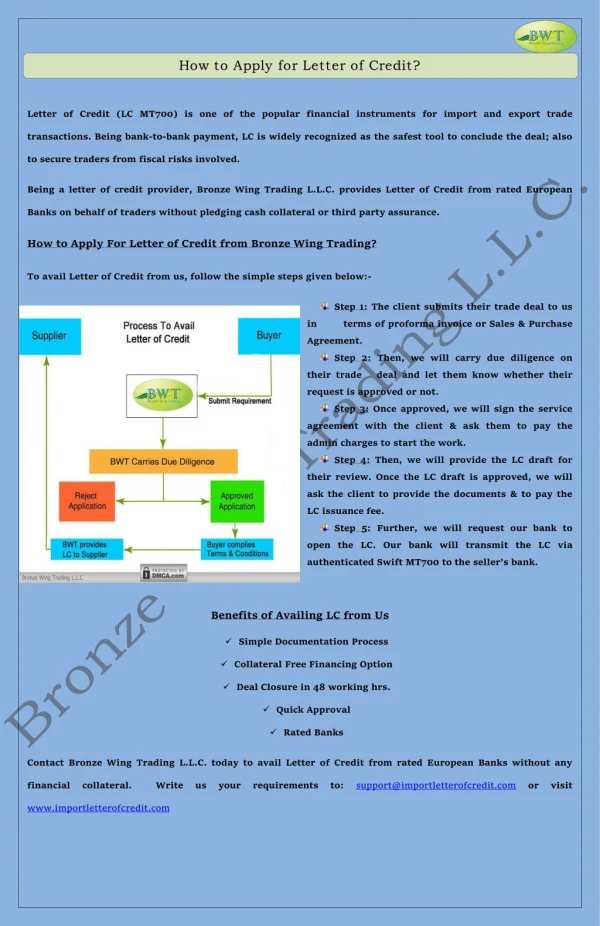

How can Letter of credit keep trading risks at bay The Letter of Credit (LC) is a documentary credit payment instrument issued by the bank. The LC guarantees that the seller shall receive full payment after the preset product delivery conditions are met. In case, if the buyer fails to fulfill his commitment of abiding the payment, the bank covers the outstanding amount to the seller. The LC is used as a secure tool for international transactions of Export, since both the parties involved are operating from different countries and they do not know about each other. The commercial letter of credit is the primary payment tool used in international trade transactions. Principles that form LC are the doctrines that are the talisman that secure the payment for both exporter and importer. Major areas of monitory risk that an Exporter might possibly encounter are, •late payment or non-payment from the buyer •damage or loss of goods during transit •Risk of rejection of goods due to differing foreign regulations and standards •Foreign exchange and interest rate changes Reimbursement transaction procedure under Letter of Credit: •Issuing bank transfers the LC to the nominated bank via swift message. •The issuing bank gives reimbursement authorisation to the reimbursing bank which issues an undertaking for reimbursement and transfers through a swift message to the issuing bank. •Nominated bank advises LC to the beneficiary and in turn, the beneficiary presents his documents. •Documents are checked and the nominated bank after negotiating upon a complying presentation, sends its claim to the reimbursing bank. •Reimbursing bank reimburses to the nominated bank in compliance with applicable terms and conditions. •Nominated bank sends documents to the issuing bank. •After the settlement is arranged between those two banks, the issuing bank gets the credit amount from the applicant and releases the original shipment documents. Documents required for Import Letter of Credit to be submitted by the importer to the importer's bank: •LC application Form •General Undertaking / Indemnity on Stamp Paper. •Recommended Board Resolution (for Companies) / Partnership Deed (for Partnership Firms) •OGL cum FEMA declaration •IE code (one time requirement) •Purchase order / Performa invoice •Insurance copy only on C&F/FOB basis •KYC report

•Annexure to the LC (Mentioning additional conditions to be incorporated in the LC if any). Documents required for Exporter Letter of Credit to be submitted by the Exporter to the Exporter's bank: •Request Letter & FEMA declaration •KYC report (One time requirement) •Copy of IEC (Importer Exporter) code •SDF and Shipping Bill ( duplicate original Exchange Control copy)/ Bill of Export/ Softex Form/ Export Declaration Form . ( GR / PP form for export of goods declared to custom till 30th Sep 2013) •NOC from respective AD if SB/EDF/Softex has been declared in the name of other Authorised Dealer. •Commercial Invoice •Original transport documents - Bill of Lading or Airway Bill •Bill of Exchange •Original L/C including amendments if any in case of documents under L/C and relevant documents as per LC. •Clarification letter for delay in submission of documents beyond 21 days from date of shipment. •Any other document as per terms and conditions between importer and exporter or as may be required as per Bank’s process and RBI guidelines from time to time. Difference between a Bank Guarantee and Letter of Credit: Letter of credit confirms full payment of the goods exported where a bank guarantee ensures minimum risk by vouching to reduce loss. Bank guarantee is more like a line of credit which guarantees a sum of money to the beneficiary. In case if the buyer cannot pay for the goods he is delivered, then the bank gives the seller the assured sum. Similarly, if the buyer is unable to deliver the goods to the importer, the assuring bank pays sum assured to the importer. Bank guarantee instrument is designed to reduce the risk of either parties involved. Difficulties that the Importers face in applying and realising the Letter of Credit: •Back to back letter of credit will be a problem because of credibility issue. Unless the party is well known and established buyer, Letter of Credit is rarely issued back to back. Under those circumstances, the buyer has to resort for the Bank Guarantee letter, or the middlemen who have an established bank reputation in repayment of credit. This also tweaks off a margin of money as commission amount. •Risks for an applicant for LC: non-delivery or receipt of inferior quality goods, risk pertaining to fluctuation of exchange rate are most common in occurrence in this case. The issuing bank's

bankruptcy is also a risk that cannot be ruled out. •When the LC is closed, the buyer should comply with the standard payment methods in seller's country. •Every detail of purchase should be kept in documents •The buyer needs to be prepared to renegotiate the terms of payment. Hence buyer also needs to hedge against the currency fluctuations by buying a forward currency contract. •Selection of the issuing bank should be done with care and with an experienced bank that regularly deals with overseas transaction and foreign trade. •Make sure that the validation time stated on the LC gives ample time for the supplier to oblige with producing the goods or pulling them off their shelves. •LC is not completely fool-proof since the credit is only based on the documents produced to the issuing bank. When the goods and contract doesn't fall in terms with the pledged documents, the credit is withheld. •When seeking LC, the documents required for customs clearance should also be furnished. Difficulties that the Exporters face in applying and realising the Letter of Credit: •Before signing contract, seller should be sure of buyer's creditworthiness. •The seller should ensure that the confirming bank overseas is a financially strong institution. •The seller's advising bank should confirm the LC issued by the buyer's bank. If it refuses, the seller should request another bank as their current bank, or the buyer's bank is in verge of insolvency. •Careful vigilance over the LC to ensure that the conditions mentioned in it can be met on time, regarding production, collection and dispatch. •Ensure that the LC is irrevocable. •Necessary amendments have to be discussed with the buyer immediately and sorted out. •The seller should confirm the coverage specified in the letter of credit and that insurance charges listed in the letter of credit are correct. Typical insurance coverage is for CIF (cost, insurance and freight) often the value of the goods plus about 10 percent. •Foreign exchange limitations need to be thoroughly familiar for the seller to avoid loss due to changing exchange rates.