Download

1 / 54

540 likes | 554 Views

Explore the global growth paradox and learn how living standards are rising worldwide, yet the median global citizen may be poorer in 2020 than today. Discover the impact on the US economy and the challenges faced by different demographic groups.

E N D

21st Annual APTC Property Tax Seminar The Economy in 2020: Growth or Stagnation? October 23, 2015 William R. Emmons Federal Reserve Bank of St. Louis William.R.Emmons@stls.frb.org These comments do not necessarily represent the views of the Federal Reserve Bank of St. Louis or the Federal Reserve System.

The Economy in 2020: Growth or Stagnation? • My prediction: Both—it depends on how you define it. • A global growth paradox • Living standards are rising around the world. • The U.S. (and other rich countries’) share of world population is shrinking; the poorest countries are growing fastest. • The paradox: Despite growth in living standards everywhere, the median global citizen may be poorer in 2020 than today. • U.S. economy in 2020: Growth and stagnation • Overall U.S. economic output will be larger in 2020. • The rewards are going increasingly to a few demographic groups defined by age, education and race or ethnicity. • The fastest-growing parts of U.S. population are benefiting less. • Our home-grown growth paradox: • Living standards are likely to stagnate for the “typical” citizen even though overall GDP and wealth are increasing.

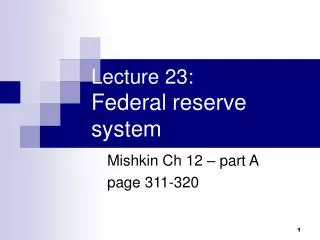

Vast Differences in the Standard of Living Around the World Median per-capita income in U.S. dollars Rich countries Poor countries Middle-income countries Source: International Monetary Fund, 2009

Economic Growth Generally is Faster in Countries that Are Poorer Rich countries Less-developed countries Source: International Monetary Fund, World Economic Outlook, April 2015

U.S. Share of World Population Is In Decline Percent Source: U.S. Census Bureau

Population is Slow-Growing or Stagnant in Other Advanced Economies, Too Percent Source: U.S. Census Bureau

Populations in Less-Developed Countries Are Growing Faster Percent Source: U.S. Census Bureau

Fastest Population Growth in the Least-Developed Countries (Africa and S. Asia) Percent Source: U.S. Census Bureau

Hypothetical Illustration of the Global Growth Paradox • Split the world into three regions • Advanced (rich) countries • Developing (middle-income) countries • Least-developed (poor) countries • Highlight two countervailing trends at work • Incomes grow fast in poor countries, raising average incomes locally and globally. • Population also grows fast in poor countries, lowering mean and median global incomes (because more poor people get counted). • Which force will win—rising quality or quantity of poor people? • Income must grow very fast in poor countries to offset the relative shrinkage of population in rich countries. • From a global perspective, adding a person with $1,000 annual income—even if it is growing fast—cannot offset the “loss” of a person making a stagnant $50,000 income.

The Global Growth Paradox: A Race Between Income and Population Growth Median per-capita income in U.S. dollars Rich countries: Slow population growth Poor countries: Fast population growth Middle-income countries: Moderate population growth Source: International Monetary Fund, 2009

A Simulated Example With 100 People in the World Dollars (log scale) People in rich countries (17% of global population) People in middle-income countries (70% of global population) People in poor countries (13% of global population) People ranked by income within their country group (highest to lowest)

2020 Scenario: Income Grows in Every Region; Population Shifts from Rich to Poor Dollars (log scale) People in rich countries (13% of global population) People in middle-income countries (70% of global population) People in poor countries (17% of global population) People ranked by income within their country group (highest to lowest)

Mean and Median Incomes Grow Faster in Middle and Poor Countries

What‘s Going On Here? My Pet Example • You are a pet lover. • Last year you owned one cat and two dogs. • Your cat weighed 8 pounds; each dog weighed 12 pounds. • Mean weight of pets = 10.7 lbs.; median weight of pets = 12 lbs.

What‘s Going On Here? My Pet Example • You are a pet lover. • Last year you owned one cat and two dogs. • Your cat weighed 8 pounds; each dog weighed 12 pounds. • Mean weight of pets = 10.7 lbs.; median weight of pets = 12 lbs. • Today you own two heavier cats and one heavier dog. • Your cats weigh 10 pounds each; your dog weighs 14 pounds. • Mean weight of pets = 11.3 lbs.; median weight of pets = 10 lbs.

What‘s Going On Here? My Pet Example • You are a pet lover. • Last year you owned one cat and two dogs. • Your cat weighed 8 pounds; each dog weighed 12 pounds. • Mean weight of pets = 10.7 lbs.; median weight of pets = 12 lbs. • Today you own two heavier cats and one heavier dog. • Your cats weigh 10 pounds each; your dog weighs 14 pounds. • Mean weight of pets = 11.3 lbs.; median weight of pets = 10 lbs. • Results of growing animals and changing mix • The mean weight of all of your pets increased (10.7 to 11.3 lbs.). • The mean weight of both your cats and your dogs increased (cats increased from 8 to 10 lbs., dogs from 12 to 14 lbs.). • But the median weight of your pets decreased.

What‘s Going On Here? My Pet Example • You are a pet lover. • Last year you owned one cat and two dogs. • Your cat weighed 8 pounds; each dog weighed 12 pounds. • Mean weight of pets = 10.7 lbs.; median weight of pets = 12 lbs. • Today you own two heavier cats and one heavier dog. • Your cats weigh 10 pounds each; your dog weighs 14 pounds. • Mean weight of pets = 11.3 lbs.; median weight of pets = 10 lbs. • Results of growing animals and changing mix • The mean weight of all of your pets increased (10.7 to 11.3 lbs.). • The mean weight of both your cats and your dogs increased (cats increased from 8 to 10 lbs., dogs from 12 to 14 lbs.). • But the median weight of your pets decreased. • The key point • An adverse change in the composition of the group can reverse overall trends that occur in each of the individual groups.

Back to the Hypothetical Example of the Global Growth Paradox Dollars (log scale) 2015 global income distribution Median = 50th percentile Ranking of all people in the world (highest to lowest)

2020 Income Distribution Lies Above 2015 Distribution At the Top—Rich Get Richer 2020 global income distribution Dollars (log scale) 2015 global income distribution Median = 50th percentile Ranking of all people in the world (highest to lowest)

But the Growing Number of Poor People Pulls Down the Median Dollars (log scale) 2015 global income distribution Median = 50th percentile Global income ranking (highest to lowest)

2020 Median Global Income Is Below 2015 Median Global Income Dollars (log scale) 2020 global income distribution 2015 global income distribution Median = 50th percentile Global income ranking (highest to lowest)

So Will the World Be Richer in 2020 Than It Is Today? • Yes and no. • Within each country or even within groups of similar countries, it is likely that both mean and median income and wealth will be higher in 2020 than in 2015. • But the composition of the world’s population is changing. • Poor countries are growing fast both in terms of income and population. • Rich countries are growing slowly in both income and population terms. • It is possible that global mean income (and top incomes) will increase while global median income stagnates or declines.

The U.S. Version of the Global Growth Paradox • Income and wealth are likely to increase in the U.S. between 2015 and 2020 as measured by • Overall means = real GDP and real household wealth. • Sub-group means and medians (many but not all). • But overall median income and median wealth may stagnate or decline, as they have for many years. • Overall (mean) income and wealth are likely to grow slowly. • Some low-income and low-wealth groups are growing in size. • How you ask the question determines how you answer it • The approach I have been pursuing: The demographics of income and wealth. • Key demographics: Birth year, age, education, race or ethnicity. • Prediction: Young, less-educated and non-white Americans will continue to struggle as they become a larger share of population.

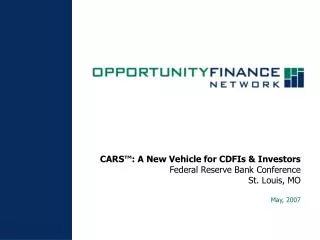

The U.S. Economy Will Continue to Grow—But More Slowly Percent Last year of 3% growth: 2005 Average annualized real-GDP growth, 2006-14: 1.4% Source: Bureau of Economic Analysis Annual data through 2014

The US Economy‘s “Speed Limit“ Has Declined to 2 Percent Percent History CBO forecast Growth rate of real potential GDP Contribution to GDP growth of labor inputs Source: Congressional Budget Office Projections as of Aug. 25, 2015

Contributions of Both Productivity and Labor Input Have Declined Percent History CBO forecast Growth rate of real potential GDP Contribution to GDP growth of productivity improvements Contribution to GDP growth of labor inputs Source: Congressional Budget Office Projections as of Aug. 25, 2015

An Important Reason Labor Inputs are Slowing—Shrinking Share of Youth Percent Source: U.S. Census Bureau

Productivity Growth Should Return to Normal; Population Growth is Slow Percent History CBO forecast Contribution to GDP growth of productivity improvements Contribution to GDP growth of labor inputs Source: Congressional Budget Office Projections as of Aug. 25, 2015

Confirming Evidence: Investors Expect Very Low Interest Rates for Many Years Percent Aug. 28, 2015: 3.57% nominal short-term yield in 2035 Aug. 28, 2015: 1.45% real short-term yield in 2025 Source: Federal Reserve Board Daily data through Aug. 28, 2015

Real Household Wealth Likely to Grow Slowly Index values equal 100 in 1995 Real household wealth Real GDP Sources: Congressional Budget Office, Federal Reserve Board Projections as of Aug. 25, 2015

Mean Income Grew Overall and for Most Demographic Groups, 1989-2013 Percent Source: Federal Reserve Board, Survey of Consumer Finances

Mean Wealth Grew Overall and for Most Demographic Groups, 1989-2013 Percent Source: Federal Reserve Board, Survey of Consumer Finances

Median Income Growth Was Weak During 1989-2013, Hinting At Composition Effects Percent Source: Federal Reserve Board, Survey of Consumer Finances

Median Wealth Declined Overall and for Several Groups, 1989-2013 Percent Source: Federal Reserve Board, Survey of Consumer Finances

This Pattern Likely to Continue—Typical Family Struggles Despite Overall Growth Percent Source: Federal Reserve Board, Survey of Consumer Finances

Clearest Illustration of the Growth Paradox in the U.S.—Race and Ethnicity • Virtually all measures of income and wealth have increased for each major racial and ethnic group, 1989-2013. • But overall measures of median income and median wealth—representing the experience of the “typical” American family—have declined. • How? The low-income and low-wealth parts of the population increased as share of the total. • This pattern is likely to continue.

Overall Median Income and Wealth Stagnated While Most Groups Enjoyed Growth Percent Source: Federal Reserve Board, Survey of Consumer Finances

The Non-White Population is Growing Faster than the White Population People Source: Federal Reserve Board, Survey of Consumer Finances

Non-White Groups Generally Have Lower Incomes and Wealth than Whites Dollars Source: Federal Reserve Board, Survey of Consumer Finances

Non-White Groups Generally Have Lower Incomes and Wealth than Whites Dollars Source: Federal Reserve Board, Survey of Consumer Finances

Non-White Groups Generally Have Lower Incomes and Wealth than Whites Dollars Source: Federal Reserve Board, Survey of Consumer Finances

Non-White Groups Generally Have Lower Incomes and Wealth than Whites Dollars Source: Federal Reserve Board, Survey of Consumer Finances

Non-White Groups Represent Increasing Shares of the Population Share of population Source: Federal Reserve Board, Survey of Consumer Finances

Non-White Groups Represent Increasing Shares of the Population Share of population Source: Federal Reserve Board, Survey of Consumer Finances

Non-White Groups Represent Increasing Shares of the Population Share of population Source: Federal Reserve Board, Survey of Consumer Finances

Non-White Groups Represent Increasing Shares of the Population Share of population Source: Federal Reserve Board, Survey of Consumer Finances

Non-White Groups Represent Increasing Shares of the Population Share of population Source: Federal Reserve Board, Survey of Consumer Finances