Download

1 / 26

260 likes | 419 Views

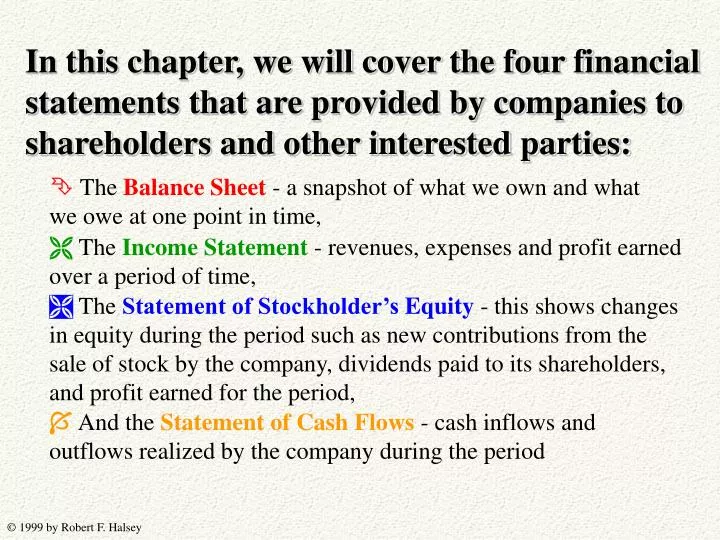

In this chapter, we will cover the four financial statements that are provided by companies to shareholders and other interested parties:. The Balance Sheet - a snapshot of what we own and what we owe at one point in time,.

E N D

In this chapter, we will cover the four financial statements that are provided by companies to shareholders and other interested parties: TheBalance Sheet - a snapshot of what we own and what we owe at one point in time, TheIncome Statement - revenues, expenses and profit earned over a period of time, TheStatement of Stockholder’sEquity - this shows changes in equity during the period such as new contributions from the sale of stock by the company, dividends paid to its shareholders, and profit earned for the period, And theStatement of Cash Flows - cash inflows and outflows realized by the company during the period

Balance Sheet The Balance sheet is divided into 2 sections: The first of these is a listing of the company’s Assets - Assets are things that the company ownsas of the date of the balance sheet. Another characteristic of an asset is that it is expected to provide the company with future benefits in the form of inflows of other assets (like cash) or decreases in the company’s indebtedness to others.

The second section of the balance sheet is a listing of the company’s liabilities and stockholder’s equity - Liabilities are what the company owesto outsiders as of the date of the balance sheet. Another characteristic of liabilities is that they are expected to require a futuresacrifice by the company, like the payment of cash or the giving up of assets.

Stockholder’sequityrepresents the investment that has been made into the company by its shareholders, less the amount of investment that has been returned to the shareholders in the form of dividends. This investment is comprised of 2 components: Contributedcapital - these are the funds that have been invested into the company through purchases of stock Earnedcapital - these are the net profits of the company that have not been paid out as dividends. Shareholders have made an additional investment in the company through their decision to retain the profits in the company rather than to pay them out in the form of dividends.

Another way to think about the balance sheet is that liabilities and equity represent sources of funds. Companies generate cash by borrowing from creditors as well as from selling their shares to investors. Likewise, assets represent uses of funds by the company. The company has invested its cash in assets that are expected to provide future benefits. Since sources of funds must equal the uses of those funds, assets must equal liabilities plus equity. This is the basic accounting equation: ASSETS = LIABILITIES + STOCKHOLDER’S EQUITY

ASSETS What we own Provides future benefits (i.e., cash inflows) Uses of Cash Liabilities and Stockholder’s Equity What we owe Requires future sacrifices (i.e., cash outflows) Sources of cash This is a summary of the Balance Sheet = =

This is the balance sheet from Colgate-Palmolive’s annual report Total assets equal $7.6 billion As do Total Liabilities and Shareholder’s Equity Now … take a moment to look at the format of this statement

Income Statement The second of the 4 financial statements in the Incomestatement. It reports the revenues that have been earned and the expenses that have been incurred during the period. Revenues are increases in assets or reductions of liabilities resulting from business transactions. Expensesare outflows of assets or increases in liabilities resulting from business transactions Net Profit is equal to Revenues - Expenses Notice that revenues, expenses, and net income refer to assets and liabilities and, therefore, do not necessarily relate to the receipt and payment of cash. Companies can, therefore, report profits without receiving net cash inflows.

Colgate reported revenues of $8.9 billion And net profit of $848 million Here is Colgate’s income statement: Now … take a moment to look at the format of this statement

Statement of Stockholder’s Equity • The Statement of Stockholder’s Equity reconciles changes in stockholder’s equity from beginning of period to end of period. • Basically, these changes result from sales and repurchases of stock and net profits less dividends paid to shareholders.

This is Colgate’s statement of Stockholder’s Equity: Notice, also, that Colgate’s retained earnings increased by the amount of profit earned during the year Notice that Colgate sold 3.3 million shares and repurchased 7.1 million shares during the year And decreased by the amount of dividends paid to shareholders Now … take a moment to look at the format of this statement

Here is the connection between the Balance Sheet and the Income Statement: • Stockholder’s equity changes each period by the amount of net profit via changes in Retained Earnings which increase with profit and decrease with losses • The Income Statement provides the detail of the changes in Retained Earnings (other than from dividends)

Statement of Cash Flows • Revenues are recorded when “earned” and expenses are recorded when “incurred” whether or not cash is received or paid • Income Statement provides detail of revenues and expenses, but not of cash inflows and outflows • The Statement of Cash Flows is needed to provide users with information about cash inflows and outflows

The statement of cash flows is organized into 3 sections as follows: Net cash flows from Operating Activities + Net cash flows from Investing Activities + Net cash flows from Financing Activities = Net change in CASH Operating activities refer to the normal business activities of the company, that is, the sale of its products. Investing activities refer to purchases and sales of long-term assets Financing activities refer to cash inflows and outflows from sales or repurchases of stock, borrowing and repayment of debt and dividends.

Colgate realized $1.1 billion net cash inflow from operating activities A net cash outflow of $351 million related to investing activities And, a net cash outflow of $830 million relating to financing activities This is Colgate’s statement of cash flows Now … take a moment to look at the format of this statement

Let’s run through an example to give you a feel for how transactions are reflected in the balance sheet and the income statement. Assume that an individual starts up a retail company, selling dresses, with an initial investment of $250. The funds are used to purchase 5 dresses for $200 that will be resold for $75 each. The company issues stock to reflect the investment. How would this be reflected on the company’s opening balance sheet?

First, cash (an asset) is increased by $250 when the stock is sold, then decreased by $200 for the purchase of the dresses. The net increase in cash is, therefore, $50. Second, the company records the dresses on its books as inventory (another asset) at its cost of $200. Inventories are goods that a company holds for resale. Finally, shareholder’s equity is increased by $250 to reflect the initial investment. The company’s balance sheet at this point in time is as follows:

Assets Cash 50 Inventories 200 Total Assets 250 Liabilities and Stockholder’s Equity Liabilities 0 SH Equity 250 Total L & SH E 250 Dress Company, Inc.Balance Sheet ASSETS = LIABILITIES + STOCKHOLDER’S EQUITY

Now, assume that the business sells 2 dresses for $75 each and that the business incurs $50 in expenses for the period which is paid in cash. Cash increased by $150 as payment is received for the dresses, then decreased by $50 for expenses incurred during the period. The net increase is, therefore, $100. When we add this to the balance in the account at the end of the previous period ($50), the new balance in cash is $150. Two somewhat difficult questions are, How do we account for the cost of the dresses that were sold? How do we account for the profit earned during the period?

The dresses are initially accounted for as inventory, an asset. When purchased, they are recorded on the balance sheet at their cost ($200 in this case). When the dresses are sold, the cost of the dresses sold is removed from the balance sheet and transferred to the income statement as an expense, called cost of goods sold (2 * $40 per dress = $80 in this case). The remaining cost in inventory for the 3 unsold dresses is $200 - 2 * 40 = $120 The company’s income statement for the period would look like this:

Dress Company, Inc.Income Statement Sales (2 * $75) 150 Cost of Goods Sold 80 Gross Profit 70 Expenses50 Net Profit 20 And the company’s balance sheet at the end of the period would look like this:

Assets Cash 150 Inventories 120 Total Assets 270 Liabilities and Stockholder’s Equity Liabilities 0 SH Equity 270 Tot L & SH E 270 Dress Company, Inc.Balance Sheet Why is Stockholder’s equity reported as $270?

Remember that stockholder’s equity is comprised of 2 components: contributed capital and earned capital. Contributed capital increased by $250 when stock was sold to the owner to raise funds to start the business. Now, earned capital increases by $20 to reflect the profit that has been earned by the company that has not been paid out to the stockholder as dividends. These accumulated profits are reported in a stockholder’s equity account called Retained Earnings. The balance in stockholder’s equity of $270, then, is comprised of $250 in contributed capital and $20 of retained earnings (look back at the Colgate-Palmolive Balance Sheet and the Statement of Stockholder’s Equity to see how this is reported in practice).

Let’s finish by reviewing, once again, the balance sheet and income statements to provide you with a definition of the most commonly used accounts...

Here is Colgate-Palmolive’s balance sheet that we reviewed earlier: Goodwill is the excess of the purchase price for another company less the fair market value of the net assets purchased. It is reported at cost less accumulated amortization Accounts receivable represent amounts owed to the company. They are reported at the net amount the company expects to collect, after deducting expected uncollectable accounts Marketable securities consist of stocks, bonds, commercial paper, etc. that the company holds as short-term investments. Inventories are goods that the company holds for sale. They are reported at the cost the company paid for them (if purchased) or their manufacturing cost (e.g., raw materials, labor and overhead). Cash refers to currency on hand as well as short-term investments expected to mature within 3 months Long-term debt represent bonds and other obligations with maturities in excess of 1 year Stockholder’s equity is divided into paid in capital (preferred, common stock and additional paid in capital) and earned capital (retained earnings) Notes payable refer to short-term debt and may also include current payments on long-term debt Property, plant and equipment represent long-term assets. They are reported at their original cost less accumulated depreciation Accounts payable are amounts owed to other companies for goods or serviced purchased Accruals represent other short-term obligations, such as amounts due for taxes, wages, or interest