Download

1 / 17

170 likes | 180 Views

The East Region, consisting of six counties including Cambridgeshire and Suffolk, is the fastest growing UK economic region with a £82bn economy and 10%+ of UK GDP. It is a hub for high-tech employment and R&D, with strong ties to Cambridge University. The region is home to numerous research centers, science parks, and technology providers, making it a thriving ecosystem for innovation and entrepreneurship.

E N D

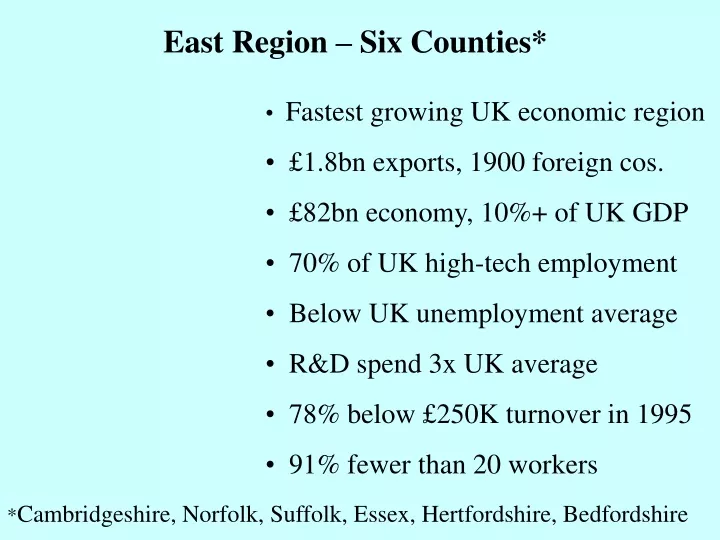

East Region – Six Counties* • Fastest growing UK economic region • £1.8bn exports, 1900 foreign cos. • £82bn economy, 10%+ of UK GDP • 70% of UK high-tech employment • Below UK unemployment average • R&D spend 3x UK average • 78% below £250K turnover in 1995 • 91% fewer than 20 workers *Cambridgeshire, Norfolk, Suffolk, Essex, Hertfordshire, Bedfordshire

750 years old • 31 Colleges, federated under • ‘umbrella’ of university • 1557 John Keys: Gonville & Caius • 1661 Isaac Newton at Trinity College • 1702/4 Chairs of Chemistry/Astronomy • 1762 Dr Richard Walker’s Botanic Garden • 1871 Cavendish Laboratory for Physics

50% of Cambridge Region hi-tech firms report research links with University 22% of research staff and 17% of directors of Cambridge region hi-tech companies possess Cambridge University degrees Cambridge University spin-outs make 16% of Cambridge hi-tech start-ups East Anglian Economy and Cambridge University source: Keeble. ESRC WP96 Publ. 1998

Centres for Research • Wellcome Genome Campus • WCMC, FFI • Babraham Institute (Biomedical) • Addenbrookes, Papworth • NIAB • “Nobel Factory” - LMB Government funded: MRC (8/40) & BBSRC (4/8)

Research Establishments and Science Parks within 15 miles of Cambridge

Biotech Cluster • 180 Companies, 10,000 employees • 25% of all biotech SMEs in Europe • 49 startups since 2000 • £1bn of VC funds in the region Technology Providers • 5 large companies - eg CCL • 1300 employees. 75% QSEs • Virtual incubators, 80-100 spin-outs

Science Parks • 1970 Cambridge Science Park • 1987 St John’s Innovation Centre • Granta Technology Park • Babraham Institute • Melbourne Science Park • Peterhouse Technology Park • Cambridge Research Park • Cambourne Business Park • Chesterford Research Park

History of the Cambridge Science Park • 1960s: First Science Park: Stanford University • 1964: Labour Government urged closer links between universities and industry • Cambridge sets up Mott Committee • 1969: Mott Committee report

Trinity College’s response • Trinity had a strong scientific tradition* • First use of the word “scientist” 1835 (Whewell) • Spare land available in a suitable location • Funds to enable it to carry out the development. • Dr John Bradfield *Alumni include Newton, Clerk-Maxwell, Rayleigh,Thomson, Walton, Rutherford, Aston, Lyle, both Braggs, Bohr, Hopkins, Klug, Kendrew

First Decade: a slow start • 1970 IBM turned down • 1971 Planning permission • 1973 Laserscan moves in • Other companies follow – including some UK subsidiaries of multinationals • By the end of the 70’s, 25 companies installed

Second Decade: clustering • Cluster developing - critical mass reached • 1984: The Trinity Centre • 3i, Venture Capital company • Labour unions, BTG monopoly broken • Academics start companies (IPR relaxation) • Spin-outs & collaborative ventures from existing companies (e.g. Cambridge Consultants)

Third Decade • Greater Cambridge cluster 3,500 cos, (85% with <10 staff) 50,000 employees • More venture funds available • Strong sectors: Life Sciences, ICT • Fewer but larger companies, more Stock Exchange launches • Same mix of spin-outs, new ventures, & UK subsidiaries of multinationals

Present • 80 companies employing 5,000 people, average age 30 • 61.5 hectares, 145,000 sq m. • Premises: 90 to 4,600 sq m. • Development by occupiers on long ground leases • Purpose-built units on 15, 20, and 25 year leases • Starter units, multi-occupancy or ‘listening posts’ on 1 month to 9 year leases

What type of tenants? • Scientific research linked to industrial production • Light industrial production closely associated with on-site or university research • Ancillary activities (e.g. Venture Capital companies, Patent & IPR law firms etc) • Not much manufacturing, except Napp, Heraeus, Polatis Trinity maintained these criteria during economic recession

Industry Sectors – company numbers • Biomedical 14 • Computers/Telecoms 25 • Consulting (technical) 6 • Energy 1 • Financial/business/non-technical 2 • Industrial Technologies 4 • Other 28 • TOTAL80

Future • New Conference Centre • Health & Fitness club • Nursery facilities (130 places) • 8.9 Hectares being developed (23,000 sq m, mostly biotech) • Cambridge Innovation Centre (60 people in 19 suites) • Continued landscaping (site density 1:5 – 18,000sq ft per acre)

Trinity’s role • Promoting contacts & interchange, website • Advertising university functions & seminars • Research sponsorship • CSP Newsletter (“Catalyst”) biannually • Provision of Conference Centre etc • Landscaping • But: Rents at normal commercial rates, minimal bureaucracy, no central management company. • Management by Bidwells, local property specialists