Download

1 / 3

30 likes | 225 Views

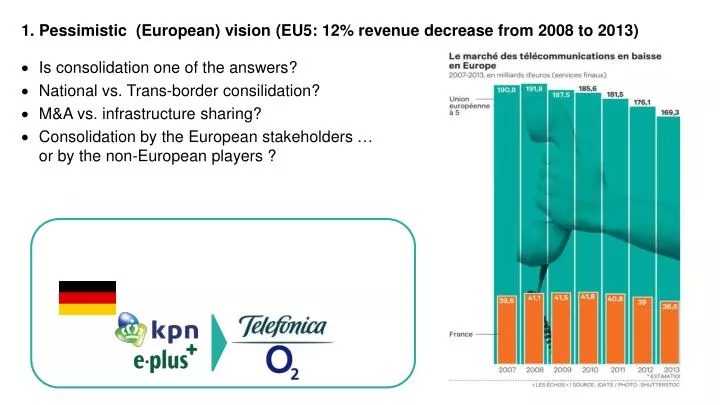

1. Pessimistic (European) vision ( EU5: 12% revenue decrease from 2008 to 2013 ). Is consolidation one of the answers? National vs. Trans-border consilidation ? M&A vs. infrastructure sharing? Consolidation by the European stakeholders … or by the non-European players ?.

E N D

1. Pessimistic (European) vision (EU5: 12% revenue decrease from 2008 to 2013) • Is consolidation one of the answers? • National vs. Trans-border consilidation? • M&A vs. infrastructure sharing? • Consolidation by the European stakeholders …or by the non-European players ?

2. Optimistic vision : telecoms are not condemned to finish like the “polaroid cameras” … but they have to reinvent their footprint and business models in the Internet ecosystem - Ex. : a “2 sided model” as one of possible scenarios Others $ Telcos $ Users service service Platform & APIs Brokering New business models Popularservices, telcodevices Data sales(personal and network) Personalinformation management, Up/cross sell QoS and interconnection(paidpeering, CDN, QoS, data centres) Tieredpricing and OTT bundles

Check up list : • consolidation • Infrastructure sharing… • Fixed-Mobile convergence • 4G/aLTE –Fiber • Differentiation/segmentation/tiered pricing • Policy management and real time billing • M2M • Big data • Cloud • SDN • … • Questions: • Where are the short term priorities for the telcos? • What are the most promising sources of new revenues? • What roles will telcos play in the evolving digital ecosystem? • What will be a telecom operator in 10 years? • …