Download

1 / 2

20 likes | 166 Views

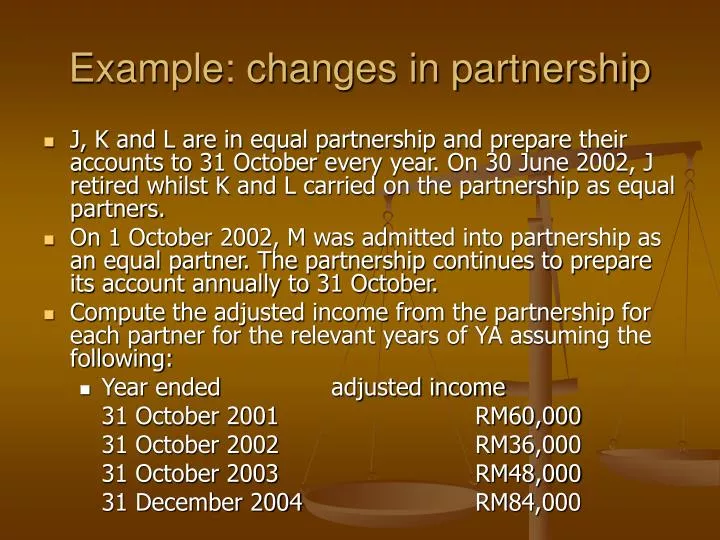

Example: changes in partnership. J, K and L are in equal partnership and prepare their accounts to 31 October every year. On 30 June 2002, J retired whilst K and L carried on the partnership as equal partners.

E N D

Example: changes in partnership • J, K and L are in equal partnership and prepare their accounts to 31 October every year. On 30 June 2002, J retired whilst K and L carried on the partnership as equal partners. • On 1 October 2002, M was admitted into partnership as an equal partner. The partnership continues to prepare its account annually to 31 October. • Compute the adjusted income from the partnership for each partner for the relevant years of YA assuming the following: • Year ended adjusted income 31 October 2001 RM60,000 31 October 2002 RM36,000 31 October 2003 RM48,000 31 December 2004 RM84,000

Example: partnership Income • A, B and C are partners of a firm of architects and prepare accounts to 31 December annually. • Up to 30 Sept. 2005, the partnership arrangement are as follows:A B C • Salary ( per annum) 30,000 30,000 20,000 • Interest on capital (per annum) 4,000 6,000 3,000 • Profit sharing ratio 1/3 1/3 1/3 • With effect from 1 October 2005, the new partnership arrangement are as follows: A B C • Salary ( per annum) 45,000 45,000 60,000 • Interest on capital (per annum) 4,000 6,000 3,000 • Profit sharing ratio 2/5 2/3 1/5 • During the year ended 31/12/2005, the partnership had an adjusted profit RM360,000 and the capital allowances due on the firm’s assets for the year amounted to RM60,000 • Approved donation amounting to RM6,000 and RM3,000 were paid on 15/1/2005 and 26/11/2005 respectively. • Compute the adjusted income for each partner.