Download

1 / 7

70 likes | 90 Views

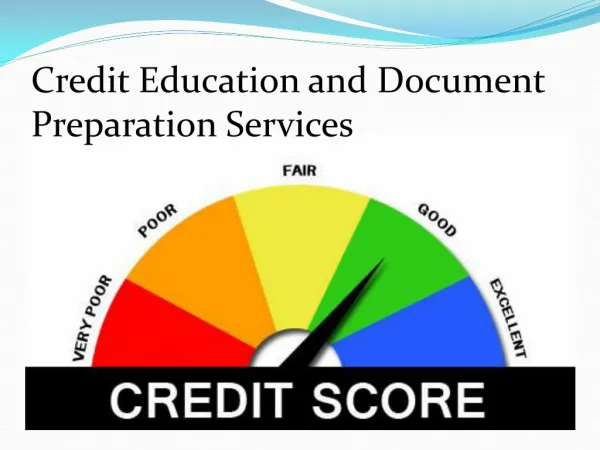

CIBIL score is a three digit number assigned to individuals by the credit information company, TransUnion CIBIL, in order to help banks and Non-Banking Financial Companies gauge the credit track record of the individual. This score is a mandatory check factor done by lenders before giving loans and credit cards. CIBIL score is checked to determine whether the individual has the capability to repay the loan or not.

E N D

CIBIL score is a three digit number assigned to individuals by the credit information company, TransUnion CIBIL, in order to help banks and Non-Banking Financial Companies gauge the credit track record of the individual. This score is a mandatory check factor done by lenders before giving loans and credit cards. CIBIL score is checked to determine whether the individual has the capability to repay the loan or not.

There are many companies who provide credit information services in India. But the scores by TransUnion Credit Information Bureau of India holds prime importance because 80-90% of the banks in India accept it. Also, some lending products like personal loans and credit cards, are unsecured in nature, meaning lenders don’t ask customers to pledge securities against it. The question then follows is, “How and why will the bank trust me with the loan amount?” This is when CIBIL score has a major role to play. CIBIL score is a reflection of your repayment ability. It gives the lender confidence in you to offer you the loan.

What is Considered to be a Good CIBIL Score? As stated above, CIBIL Score is a three digit number, which ranges between 300 to 900. Lower end of the spectrum represents the worst score, whereas, higher end, which is 900, represent the best score. Ideally, a score of 750 and above is considered to be a good score. If you reside in this bracket, getting lending products shouldn’t be a problem.

4 Ways on how to improve CIBIL Score! 1. Make All the Due Payments - We often end up exhausting our credit limit in a month and then don’t pay our dues on time. This happens due to mismanagement. Set a lower limit than your credit limit for every month. That way you’ll end up spending less and can pay your dues easily. The same applies for loan account also. Check with the bank about your unpaid dues and pay it off as soon as possible for a better CIBIL reflection.

2. EMI payment on time: This is one of the way that organically boosts your CIBIL score. All it takes is to be committed to get over the loan or credit card dues as soon as possible. Never bite more than you chew. Know your limit and spend accordingly so that you won’t face any difficulty in paying your monthly installments. 3. Dispute Settlement: CIBIL prepares the credit score report on the basis of the information collected from Member Banks. There can be a scope for errors cause humans are involved in the data entry process. If you find any transaction that you’re not sure about, you can raise a dispute on CIBIL’s website. By doing this, the damage done on your CIBIL website can be easily rectified.

4. Increased Credit Limit: Ask your credit card bank to give you a higher credit limit. This does not mean that you can spend more. This is just to show CIBIL that you’ve kept your credit utilisation ratio low by spending less and servicing your debt at time. Seeing this, CIBIL restores confidence in you and increases your CIBIL score. These were four essential hacks on how to improve CIBIL score. With a more disciplined approach towards spending, you can increase your CIBIL score without any difficulty.