Download

1 / 1

10 likes | 119 Views

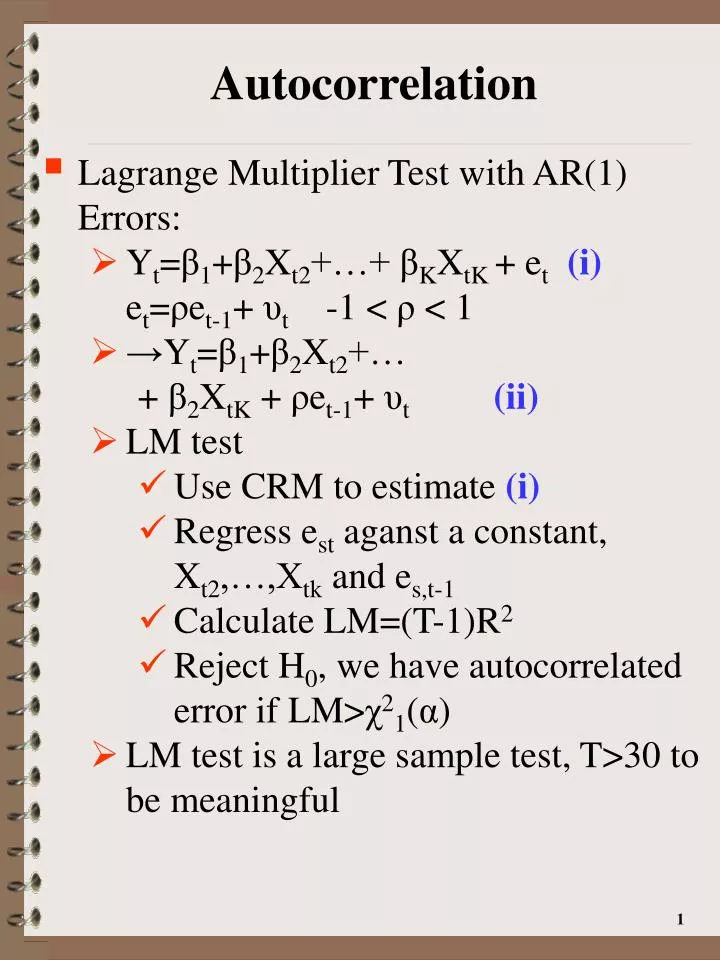

Autocorrelation. Lagrange Multiplier Test with AR(1) Errors: Y t = β 1 + β 2 X t2 +…+ β K X tK + e t (i) e t = ρ e t-1 + υ t -1 < ρ < 1 → Y t = β 1 + β 2 X t2 +… + β 2 X tK + ρ e t-1 + υ t (ii) LM test Use CRM to estimate (i)

E N D

Autocorrelation • Lagrange Multiplier Test with AR(1) Errors: • Yt=β1+β2Xt2+…+ βKXtK + et (i) et=ρet-1+ υt -1 < ρ < 1 • →Yt=β1+β2Xt2+… + β2XtK + ρet-1+ υt(ii) • LM test • Use CRM to estimate (i) • Regress est aganst a constant, Xt2,…,Xtk and es,t-1 • Calculate LM=(T-1)R2 • Reject H0, we have autocorrelated error if LM>χ21(α) • LM test is a large sample test, T>30 to be meaningful