Download

1 / 18

840 likes | 1.9k Views

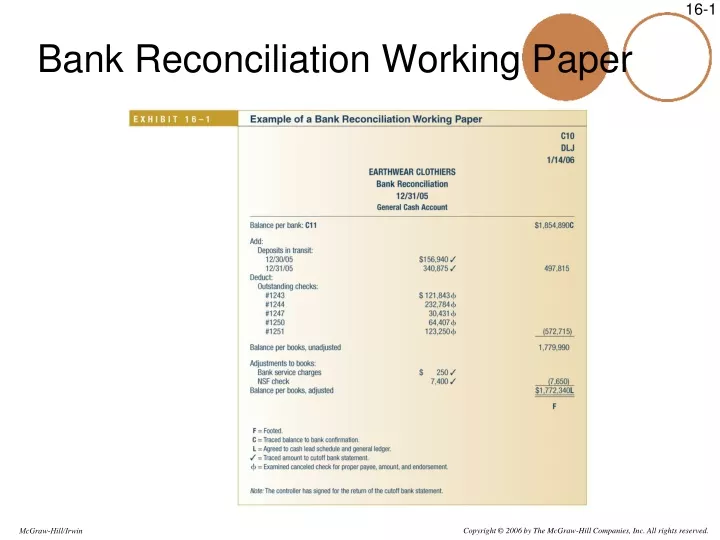

Bank Reconciliation Working Paper. Standard Bank Confirmation Form. Date of Last Bank Reconciliation. 7 to 10 Days. Cutoff Bank Statement. A cutoff bank statement normally covers the 7- to 10-day period after the date on which the bank account is reconciled.

E N D

Date of Last Bank Reconciliation 7 to 10 Days Cutoff Bank Statement A cutoff bank statement normally covers the 7- to 10-day period after the date on which the bank account is reconciled. Any reconciling item should have cleared the client’s bank account during the 7- to 10-day period.

Tests of the Bank Reconciliation • The auditor uses the following audit procedures to test the bank reconciliation: • Test the mathematical accuracy and agree the balance per the books to the general ledger. • Agree the bank balance on the reconciliation with the balance shown on the standard bank confirmation. • Trace the deposits in transit on the bank reconciliation to the cutoff bank statement. • Compare the outstanding checks on the bank reconciliation with the canceled checks in the cutoff bank statement for proper payee, amount and endorsement. • Agree any charges included on the bank statement to the bank reconciliation. • Agree the adjusted book balance to the cash account lead schedule.

Fraud-Related Audit Procedures Extended Bank Reconciliation Procedures Proof of Cash Tests for Kiting

Auditing a Payroll or Branch Imprest Account The audit of any imprest cash account such as payroll or a branch account follows the same basic audit steps discussed under the audit of the general cash account.

Obtain an Understanding of Internal Control The auditor should obtain an understanding of each of the five components of internal control in order to plan the audit. This knowledge is used to: Identify types of potential misstatements Consider factors that affect the risk of material misstatement Design tests of controls Design substantive procedures

Auditing Petty Cash Usually not material. Potential for defalcation. Seldom perform substantive tests. Document controls.

Investments Common Stock Preferred Stock Debt Securities Hybrid Securities

Control Risk Assessment—Investments Here are some of the more important assertions for investments. Occurrence and Authorization Completeness Accuracy and Classification