Download

1 / 31

310 likes | 445 Views

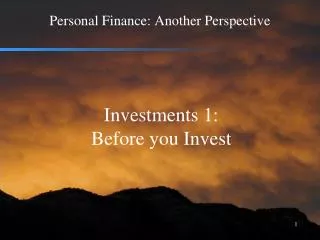

Why Do We Invest?. Certificates of Deposit After Taxes and Inflation. CD Returns After Taxes and Inflation. $150,000. $140,000. $130,000. $120,000. $110,000. $100,000. 2011. 1997. 1994. 1998. 2000. 2002. 2004. 1996.

E N D

Certificates of DepositAfter Taxes and Inflation CD Returns After Taxes and Inflation $150,000 $140,000 $130,000 $120,000 $110,000 $100,000 2011 1997 1994 1998 2000 2002 2004 1996 Sources: Six-month CD rates were obtained from Wiesenberger. Inflation rates were obtained from the Bureau of Labor Statistics.

Inflation Today In 10 Yrs In 20 Yrs In 30 Yrs Car $ 25,000.00 $ 35,265.00 $ 49,744.00 $ 70,170.00Condo $140,000.00 $197,484.00 $278,570.00 $392,951.00Cup of Coffee $ 1.50 $ 2.12 $ 2.98 $ 4.21Auto Oil Change $ 35.00 $ 49.00 $ 70.00 $ 98.00Restaurant Dinner $ 20.00 $ 28.00 $ 40.00 $ 56.00Monthly Health Insurance $ 300.00 $ 778.00 $ 2,018.00 $ 5,235.00Prescription Medicine $ 45.00 $ 116.00 $ 302.00 $ 785.00Gallon of Gas $ 3.50 $ 6.57 $ 12.33 $ 23.15Hospital Visit $ 4,500.00 $ 11,672.00 $ 30,274.00 $ 78,522.00Monthly Electric Bill $ 200.00 $ 375.00 $ 704.00 $ 1,323.00 Nominal Inflation Rate: 3.5% Energy Inflation Rate: 6.5% Medical Inflation: 10%

How Does a StockholderMake Money? CAPITAL CORPORATION INVESTORS DIVIDENDS CAPITAL GAINS

Shareholder Risks 1. Specific risk 2. Market risk 3. Economic risk 6

How Do Bonds Work? INVESTORS LOAN BOND ISSUER INTEREST PAYMENTS

Bond Issuers FEDERAL GOVERNMENT FEDERAL GOVERNMENT AGENCIES MUNICIPAL GOVERNMENT FOREIGN GOVERNMENT CORPORATIONS

Interest Rate Risk INTEREST RATES VALUE OF THE BOND

How DoMutual Funds Work? DIVIDENDS/CAPITAL GAINS INVESTORS INVESTMENT COMPANY CAPITAL DIVIDENDS/CAPITAL GAINS

Types of Mutual Funds 1. Aggressive growth funds 2. Growth funds 3. Growth and income funds 4. Balanced funds 5. Income funds 6. Tax-exempt funds 7. Specialized funds 8

Tax-Deferred Growth $10,000 @ 6% in 28% tax bracket $57,435 $10,000 @ 6% tax deferred $44,153 Tax-deferred account after taxes $35,565 $32,071 $23,300 $17,908 $15,264 10 years 20 years 30 years Mortality and expense charges, sales charges, and administrative fees are not taken into account and would reduce the performance shown if they were. A 10% tax penalty applies for withdrawals prior to age 59½.

How Does anAnnuity Work? $179,085 $100,000 payout phase accumulation phase MONTHLY INCOME $1,974

Fixed or Variable Rate of Return?

InvestmentConsiderations 1. Objectives / time frame 2. Risk tolerance 13

Historically, Long-TermInvesting Reduces Risk S&P 500 Composite Total Return 1966–2011 # of Periods % of Periods Holding Period with a Loss Total Periods with a Loss 1 Year 13 45 28.8% 5 Years 4 41 9.7% 10 Years 1 36 2.7% Source: Wiesenberger

Long-TermInvestment Strategy GROWTH IN THE VALUE OF $100 FROM 1987–2011 $4,000 $3,523 $3,000 $2,000 $995 $1,000 $514 $314 $0 INFLATION TREASURY BILLS CORPORATE BONDS STOCKS Sources: Bureau of Labor Statistics (CPI); Wiesenberger (3-month T-bills, Salomon Brothers Corporate Bond Composite Index, S&P 500 Composite Total Return)

Investment Spectrum HIGHER RISKHIGHER POTENTIAL RETURN CASH EQUIVALENTS FIXED INTEREST BONDS STOCKS LOWER RISKLOWER POTENTIAL RETURN

Sources of Risk 1. Economy 2. Interest rates 3. Market 4. Specific risks 5. Inflation 14

STOCKS 30% BONDS 50% MONEY MARKET 20% Conservative Investor

STOCKS 80% BONDS 15% MONEY MARKET 5% Aggressive Investor

Where Do You Go from Here? • Do it yourself • Work with others • Work with us • Procrastinate