Download

1 / 15

170 likes | 375 Views

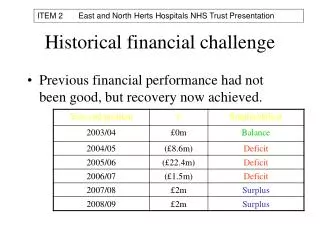

Treating Customers Fairly - the challenge for financial services marketers . Tony Katz, Financial Promotions Team, FSA. How consumers feel about financial providers. 79%. 76%. 63%. 60%. 59%. 57%. 46%. They’re not interested in helping you understand what’s best for your needs.

E N D

Treating Customers Fairly - the challenge for financial services marketers Tony Katz, Financial Promotions Team, FSA

How consumers feel about financial providers 79% 76% 63% 60% 59% 57% 46% They’re not interestedin helping youunderstand what’s best for your needs They don’treward loyalty It’s hard to know ifyou’re gettinga good deal You can trustthem You have to change your provider regularly or you end up with a poorer deal They make it so complicated youend up confused The language they use is difficult to understand Source: BMRB Online - regular newspaper readers who have acquired or renewed home or motor insurance within the last 6 months or acquired or renewed a mortgage, loan or credit card within the last 12 months, 3753

Principles-based regulation • A fantastic opportunity to innovate! • Greater responsibility for firms and senior management

TCF outcomes 1: Consumers can be confident that they are dealing with firms where the fair treatment of customers is central to the corporate culture. 2: Products and services marketed and sold in the retail market are designed to meet the needs of identified consumer groups and are targeted accordingly. 3: Consumers are provided with clear information and are kept appropriately informed before, during and after the point of sale. 4: Where consumers receive advice, the advice is suitable and takes account of their circumstances. 5: Consumers are provided with products that perform as firms have led them to expect, and the associated service is of an acceptable standard and as they have been led to expect. 6: Consumers do not face unreasonable post-sale barriers imposed by firms to change product, switch provider, submit a claim or make a complaint.

“Management must think of itself not as producing products, but as providing customer-creating value satisfactions. It must push this idea..into every nook and cranny of the organisation. It has to do this continuously and with the kind of flair that excites and stimulates the people in it”Ted Levitt

COBS: high-level requirements for financial promotions Communications must be accurate and sufficient for their purpose They must be presented in a way that is likely to be understood by the average member of the group to whom they are directed Where benefits are discussed, there must be a fair and prominent indication of any relevant risks Firms must not disguise, diminish or obscure important items, statements or warnings

Issues to consider in designing KFDs Type size Attractiveness of the text Clarity of the key messages about cancelling Relevance Repetition Amount of process detail (which is better explained elsewhere) Style: – use active verbs and positive language; – stick to precise and short sentences; – avoid the use of abstractions and redundant phrases; and – avoid legal terms and bureaucratic language. Key Features

Good practice: price/savings claim representative of likely customer benefit clear basis on which such saving is to be achieved Poor practice: unclear or hidden explanation of savings claim misleading claim, false customer expectations Savings claims

Good practice Risk information appears prominently on the first page of the website the customer arrives at and near to the product description. Devices such as fixed risk warnings remain on the screen even when the customer scrolls up and down. The customer is encouraged to think about whether the product is right for them. The risks are repeated further into the application process. Poor practice The risk information can be easily overlooked which could also result in the consumer being taken straight to an application form (e.g. by clicking on to a banner advertisement or accepting a cookie). Key information, such as on fees or exclusions are buried within the website or placed in a separate section such as FAQs. Internet promotions

Fewer rules do not mean lower standards Stand-alone compliance Culture is the key to it all Last word