Download

1 / 4

40 likes | 136 Views

Suburban Detroit Office Market Posts Strong Positive Absorption In 3rd Quarter, According to Paragon Corporate Realty Services Survey

E N D

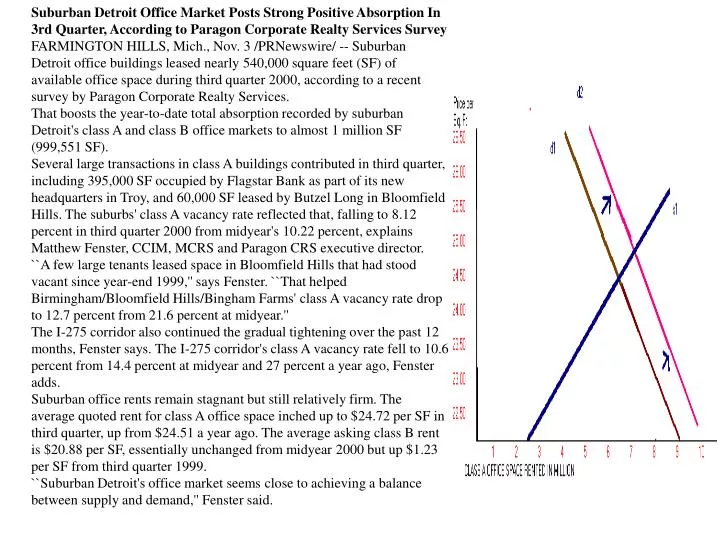

Suburban Detroit Office Market Posts Strong Positive Absorption In 3rd Quarter, According to Paragon Corporate Realty Services Survey FARMINGTON HILLS, Mich., Nov. 3 /PRNewswire/ -- Suburban Detroit office buildings leased nearly 540,000 square feet (SF) of available office space during third quarter 2000, according to a recent survey by Paragon Corporate Realty Services. That boosts the year-to-date total absorption recorded by suburban Detroit's class A and class B office markets to almost 1 million SF (999,551 SF). Several large transactions in class A buildings contributed in third quarter, including 395,000 SF occupied by Flagstar Bank as part of its new headquarters in Troy, and 60,000 SF leased by Butzel Long in Bloomfield Hills. The suburbs' class A vacancy rate reflected that, falling to 8.12 percent in third quarter 2000 from midyear's 10.22 percent, explains Matthew Fenster, CCIM, MCRS and Paragon CRS executive director. ``A few large tenants leased space in Bloomfield Hills that had stood vacant since year-end 1999,'' says Fenster. ``That helped Birmingham/Bloomfield Hills/Bingham Farms' class A vacancy rate drop to 12.7 percent from 21.6 percent at midyear.'' The I-275 corridor also continued the gradual tightening over the past 12 months, Fenster says. The I-275 corridor's class A vacancy rate fell to 10.6 percent from 14.4 percent at midyear and 27 percent a year ago, Fenster adds. Suburban office rents remain stagnant but still relatively firm. The average quoted rent for class A office space inched up to $24.72 per SF in third quarter, up from $24.51 a year ago. The average asking class B rent is $20.88 per SF, essentially unchanged from midyear 2000 but up $1.23 per SF from third quarter 1999. ``Suburban Detroit's office market seems close to achieving a balance between supply and demand,'' Fenster said.

Factors contributing to increase in demand & prices • Larger companies looking for new HQ in 2000 • More technology companies looking for space • Less office space being built in respect to demand than in 1999 • How much less?

1999 1.9 million Sq ft of new office space Compared to…………….. 2000 1.15 million Sq ft of new office space. Notable results from increase in demand • Birmingham/Bloomfield/Bingham Farms vacancy dropped to 12.7% from 21.7 from a year ago • I-275 corridor vacancy dropped to 10.6 % from 21.6 %

Conclusion • Rent prices for year 2000 Class A office space were inelastic when compared to the huge decrease in vacancy rates • A large supply of office space available in other parts of Metro Detroit are contributing to the small increase in rent prices. • Very competitive environment with lots of location options for companies • Rental market is approaching equilibrium,but is not there yet