Download

1 / 31

360 likes | 538 Views

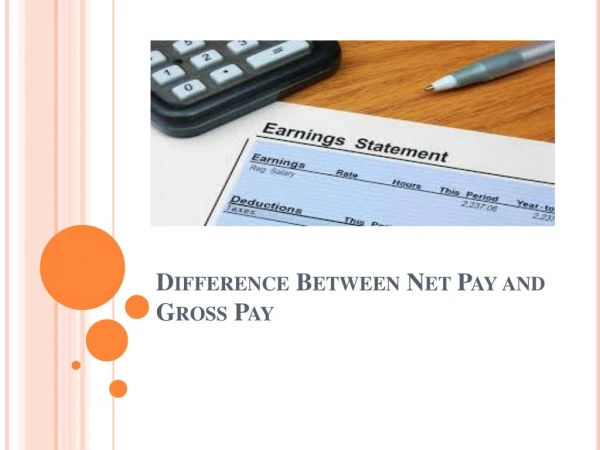

Chapter 2 Net Pay. 2.1 Deductions from Gross Pay. Federal Withholding Tax Deduction. Deductions-Subtractions from gross pay Withholding taxes-income taxes Amount of taxes depends on: Wages Marital status Number of withholding allowances claimed

E N D

Federal Withholding Tax Deduction • Deductions-Subtractions from gross pay • Withholding taxes-income taxes • Amount of taxes depends on: • Wages • Marital status • Number of withholding allowances claimed • Withholding allowance-used to reduce the amount of tax withheld

Social Security & Medicare Tax Deductions • FICA benefits include: • Disability benefits • Medicare • Retirement benefits • Survivor’s benefits • Social Security is 6.2% for first $87,900 • Medicare is 1.45% for all wages • Combined FICA is 7.65% (6.2% + 1.45%)

C. $24,000 x 0.0765 = D. $87,900 x 0.062 = $89,000 x 0.0145 = E. $460 x 0.0765 = F. $712.44 x 0.0765 = G. $1,087.30 x 0.0765 = H. $375.88 x 0.0765 =

Total Deductions and Net Pay • Withholding Taxes • Social Security • Medicare • Other Deductions • Net Pay = Take Home Pay • Gross Pay – Deductions = Net Pay

$410 x 0.0765 = $410 – 39 – 31.37 - 34.88 - 40 = J. $820 x 0.0765 = $810 – 118 – 61.97 – 74 – 45 =

Total Job Benefits • Employee benefits – Fringe benefits • What are some examples of job benefits?

Benefit 1 + Benefit 2 = Total Employee Benefits Benefit Rate x Gross Pay = Total Employee Benefits Gross Pay = Employee = Total Job Benefits Benefits

A. 1. $2,580 + $3,133 + $2,545 = 2. $31,807 + $8,258 = B. $28,089 x 0.33 = 28,089 + 9,269.37 =

Net Job Benefits • Job Expenses - Examples Total Job – Job Expenses = Net Job Benefits Benefits C. $56,102 – 329-278-475-1,077 = D. 78,299-580-1,793-2,057 =

Comparing Net Job Benefits E. Job 1 41,700 x 0.32.5 = 41,700 + 13,552.5 = 55,252.50 – 3,180 = Job 2 45,260 x 0.24 = 45,260 + 10,862.40 = 56,122.40 – 3,740 =

F. Job 1 49,500 x 0.29 = 49,500 +14,355 = 63,855 – 650-1,890-375-480 = Job 2 45,200 x 0.34 = 45,200 + 15,368 = 60,568 – 2,560 – 480 – 590 – 380 =

Adjusted Gross Income and Taxable Income • From 2.1 – withholding taxes taken out of paycheck every pay period • Dec 31 end of year and federal income tax returns prepared for April 15 • Tax returns based on income earned and taxes due • Withholding taxes are used here

Gross Income – Total income in a year Adjustments are subtracted from income. Include business losses, payment to retirement plan, alimony and certain penalties. Adjusted Gross = Gross Income – Adjustments Income to Income • Taxable Income – income you actually pay taxes on Taxable = Adjusted Gross - Deductions & Income Income Exemptions

Deductions – Expenses that reduce the amount of your taxable income • Which is more standard deductions or itemized, use the bigger of the two. • Standard deductions: • $4,850 for individual • $9,700 for married filing jointly • Exemption is an amount of income per person that is tax free • $3,100 per person

AGI 65,000 - Ded 4,850 - Exe 3,100 Tax Inc B. AGI 50,000 - Ded 10,500 - Exe 9,300 Tax Inc

Income Tax Due • Get a refund if paid too many taxes – remember withholding taxes from paychecks • Pay in if didn’t pay enough taxes through the year • Use the tax tables on pg. 56

C. From tax table 1,679 2,340 – 1,827 = refund or pay in? D. 2,874 from tax table 2,874 – 2,509 = refund or pay in?

State and City Flat Income Tax • Flat tax is the same tax to everyone usually stated as a % of earnings • 34,100 x 0.015= • 29,900 x 0.028 =

State & City Graduated Income Taxes • As your income goes up the amount of taxes you pay goes up C. 43,600 - 40,000 = 3,600 x 0.07 = 1,600 + 252 = D. 38,200 – 32,000 = 6,200 x 0.06 = 1,120 + 372 =

2.5 Cash Receipts and Payment Records • Cash receipts records – Written records of $ received A.

B. 154.40 +83.75+190.45+275.90+ 150.80 =

Columnar Cash Payments Record • Cash payments are written records of $ paid out C. 27.88+95.85+4.50+54.91+135.67+25+ 47.89 = D. 700+123.83+62.28+70+52.76+100=

Expense Percentages • Summarize expenses and receipts with percentages • Helps to compare past, present, and future • Can use specific categories to help with spending

6,400 / 128,000 = • 338,200 / 475,000 =

Budgeting • Budgets are future spending plans C. 0.05 x 4,500,000 = D. 0.025 x 5,489 = Fixed Income Variable Income Fixed Expenses Variable Expenses