Download

1 / 37

430 likes | 664 Views

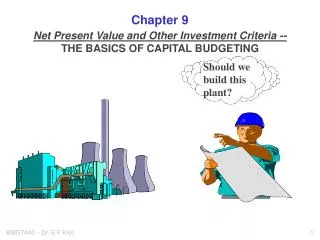

Chapter 8 Cost Estimating / Budgeting. Project Management for Business, Engineering, and Technology. Cost Overruns on Projects. 300. 200. Cost overrun %. 100. 0. -100. 1910. 1930. 1950. 1970. 1990. 1920. 1940. 1960. 1980. 2000. Year of decision to build.

E N D

Chapter 8Cost Estimating / Budgeting Project Management for Business, Engineering, and Technology

Cost Overruns on Projects 300 200 Cost overrun % 100 0 -100 1910 1930 1950 1970 1990 1920 1940 1960 1980 2000 Year of decision to build Projects versus Percent Cost Overrun (Flyvbjerg, B., Bruzelius, N., & Rothengatter, W., Megaprojects and Risk: An Anatomy of Ambition. Cambridge:Cambridge University Press, 2003, p. 17. With permission.)

Sources of Cost Escalation and Overruns • Uncertainty and Lack of Accurate Information • Changes in Requirements or Design • Economic and Social Factors • Inefficiency, Poor Communication, and Lack of Control • Ego Involvement of the Estimator • Project Contract • Bias and Ambition

Cost Estimating and the Systems Development Life Cycle At project initiation Regions of time- cost uncertainty At project definition At project execution Contingency fund Cumulative cost Cost estimate Time

System Life Cycle Costs Life cycle costs (LCC) • All costs of a system throughout its full cradle-to-grave life cycle, i.e.: • all costs incurred during the project life cycle phases of Definition and Execution • PLUS all costs associated with the Operations phase of the system and the eventual disposal of the system

System Life Cycle Costs Purpose of life cycle cost analysis • To anticipate the realities of operating, maintaining, and (ultimately) disposing of the end-item system • To establish target costs for operating, maintaining, and disposing of the end-item system. • To design the system so it will meet those target costs.

Estimating Process Estimate versus Target or Goal • Estimate: a realistic assessment based upon known facts about the work, required resources, constraints, and the environment, derived from estimating methods • Target or goal: a desired outcome, commitment, or promise. • Don’t confuse estimates with goals. The estimating process is directed at producing good estimates, not restating targets or goals.

Estimating Process Accuracy versus Precision • Accuracy: the closeness of the estimated value to the actual value • Precision: the number of decimal places in the estimate. • Accuracy of estimates is more important than precision

Estimating Process Estimating Methods • Expert opinion • Analogy + compensation for differences • Parametric: Formula or Cost Function, e.g., Cost, engine A = (Cost, engine B) Cost, cabling = 150 (total area + 10%) + 300 (number of rooms) + 125 (number of floors) ( ) 0.7 Thrust, engine A Thrust, engine B

Estimating Methods (cont’d) • Cost engineering Detailed cost breakdown of labor, materials, etc. at the work package or task level.

Total, 1 = 60 Total, 2 = 30

Estimating Process • Any of these methods can be used in any area of project • Parametric and cost engineering methods are the best

Estimating Process • Rule of Thumb: The smaller the work packages or portion of the end-item estimated, the better the estimate

Estimation Process Procedure for larger projects Project Management (PM) 1. WBS information Functional Management (FM) 2. 3. Work Team Leads

Project Management WBS information 1. Functional Management 2. 3. Work team Estimation Process • PM: Uses WBS to identify work packages • FM: Subdivide work packages into identifiable tasks; determine labor, material, facilities, and resources requirements for each • Supervisors/team leads: Estimate number of labor hours and quantities of materials needed

Estimation Process Project Management 6. Labor and cost estimates Functional Management 4., 5. Work team

Estimation Process Project Management • FM: check and aggregate time and material estimates • FM: convert time estimates into costs • PM: checks over and approves all estimates aggregates costs; added in overhead costs: Project cost = ∑direct costs + ∑ overhead costs 6. WBS information Procedure for larger projects, steps 4-6 4., 5. Functional Management Work team

Estimation Process Project Management 7., 8. WBS information Functional Management Work team

Estimating Process (cont’d) Project Management 7., 8.. • PM: Adds in contingency amounts. Two possible contingencies • Base estimate = Σ (WP estimates + WP contingency) (to handle “known-unknowns”) • Final estimate = Base estimate + overheads + project contingency (to handle “unknown unknowns”; PM controls this) • PM: Compares bottom-up estimates to top-down targets or goals. Attempt to reconcile differences. WBS information Procedure for larger projects, steps 7-8 Functional Management Work team

Project Budget • Specific for each project • Not a fiscal budget. • Subdivided into Control Accounts, one for each work package • Each cost account is a portion of the project total budget • Rosebud Example

Project budget subdivided into control accounts ROSEBUD Project Budget $ 356,755 Basic design Hardware Software Projectmanagement Final Tests $179,868 $122,228 J $31,362 $10,857 $ 12,550 User Test Cost Accounts Procedures Materials Installation $100,846 $20,352 Q M $138,571 Y X $6,622 Assembly Specifications System Test V $20,945 $21,272 L $4,235 W

Performance Analysis • BCWS - Budgeted Cost of the Work Scheduled • ACWP - Actual Cost of the Work Performed • BCWP - Budgeted Cost of the Work Performed (Earned Value) • BCWP = BCWS for task completed • BCWP subjective estimate of costs for tasks started but not yet completed

Example • Parmete Co. is to remove 1,000 parking meters and replacing them with new ones for which they will receive $200 per meter. Estimate they can install 25 meters / day. For day 18, BCWS = 18 x 25 x 200 = $90,000

Example (cont.) If by day 18, only 400 meters are finished, then BCWP = 400 x 200 = $80,000 Variance = BCWS - BCWP = -$10,000 Note: -$10,000 does not represent a cost savings, but rather that the project is 2 days behind schedule

Scheduled Project Costs 200,000 150,000 BCWS 100,000 BCWP Costs 50,000 0 0 10 20 30 40 Time Example (cont.)

Variances • Accounting Variance AV = BCWS - ACWP • Schedule Variance SV = BCWP - BCWS • Time Variance TV = SD - BCSP SD = Status Date BCSP = date BCWS = BCWP • Cost Variance CV = BCWP - ACWP

Logon Project Status 600 AV 500 SV 400 BCWS 300 BCWP Cost ($1,000) ACWP 200 100 0 0 5 10 15 20 25 Week Logon Project (Week 20) SV = BCWP - BCWS = -$80,000

Performance Indices • SPI = Schedule Performance Index SPI = BCWP/BCWS SPI > 1 work ahead of schedule • CPI = Cost Performance Index CPI = BCWP/ACWP CPI > 1 project underbudget

Logon Project (Week 20) • SPI = BCWP/BCWS = 432/512 = .84 • CPI = BCWP/ACWP = 432/560 = .77 Project is behind schedule and over cost

Forecast Cost At Completion FCAC = Forecast Cost At Completion = % by which on schedule x BCAC = (ACWP/BCWP) x BCAC = BCAC/CPI where BCAC = Budgeted Cost At Completion

Logon Example For Logon, the Budgeted Cost at Completion is given by BCAC = $990,000 At week 20, BCWP = 432 whereas ACWP = 560 we are running 560/432 = 1.30 times over budget FCAC = 1.3 x 990,000 = $1,283,333

Forecast Cost To Complete FCTC = Forecast Cost To Complete = Forecast Cost At Completion - ACWP = FCAC - ACWP = BCAC/CPI - ACWP = (BCAC - BCWP)/CPI

Logon Example FCTC = (BCAC - BCWP)/CPI = (990,000 - 432,000)/.77 = $724,675 Summary: In week 20 we have completed 432,000 of budgeted work at a cost of 560,000. Given the current trend, we expect to complete the project at cost remaining of $724,675 for a final project cost of $1,283,333.

Logon Status & Forecast 1400 FCAC SD 1200 BCAC 1000 BCWS 800 FBCWP Cost ($1,000's) 600 FACWP 400 200 0 0 10 20 30 40 50 Week Logon Example

Logon Example Logon Status & Forecast 1400 FCAC SD 1200 BCAC 1000 BCWS 800 FBCWP Cost ($1,000's) 600 FACWP 400 200 0 0 10 20 30 40 50 Scheduled Completion Revised Completion Week