Download

1 / 4

0 likes | 11 Views

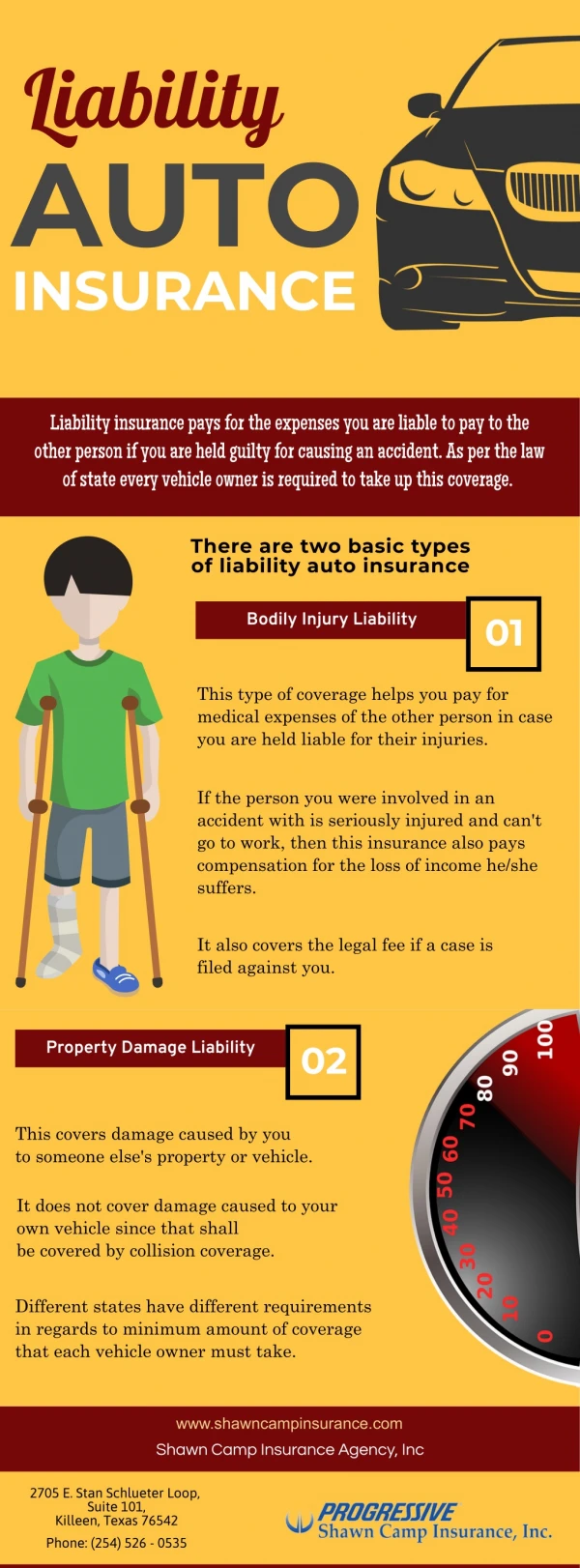

Insurer has a maximum payout for incidents on your auto liability policy, known as coverage limit. Exceeding it means covering extra costs. Let us understand these limits to optimize coverage and reduce financial risks in accidents.

E N D

There's a maximum amount that your insurer can pay for a covered incident on your auto liability policy. This figure is the coverage limit for the specific event. If the cost of the covered accident exceeds your policy's coverage limit, you'll have to pay for the extra liability out of pocket. It's important to understand how car insurance liability limits work. Also, figure out the best way to maximize coverage and minimize the risk of a financial loss if you're ever held liable for an auto accident. Read on to learn more. Liability Coverage Limits Explained To legally drive in any state, you should meet the minimum auto liability coverage requirement. A typical coverage limit is expressed in three numbers, such as 25/50/25. If these are the figures on your auto liability policy, your coverage limits work out as follows: Your insurance can only pay a maximum of $25,000 per person for bodily injury per accident Your insurance can only pay a total of $50,000 per accident for bodily injury, regardless of the number of injured persons The last 25 is the maximum dollar amount ($25,000) per accident that your auto insurance policy can pay for property damage Why It's Best to Have Higher Liability Coverage Limits Assume your existing auto liability coverage limits are $25,000/$50,000/$25,000, as explained above. If you got involved in an at-fault accident and three people got injured, your policy would pay for their medical bills, wages, and other losses only up to $50,000. If the total treatment cost for the three is $76,000, you'd have to pay for the extra $26,000 out of your own pocket. If the cost of repairing the other driver's car is $35,000, your insurance would only pay $25,000, and you'd be responsible for the remaining $10,000.

You could avoid or significantly reduce your out-of-pocket expenses in the above scenario by increasing your liability coverage limits from the basic 25/50/25 requirement. What about Uninsured Driver Coverage Limits? A recent study showed that about 13% of drivers don't have auto liability insurance. Uninsured coverage could help pay for your car repair and medical costs if you got injured in a car accident caused by one of these drivers. Some states require motorists to have this coverage, but you should consider having it even if it's not mandatory where you live. The limits for this coverage are also expressed in numbers such as 25,000/50,000. What if the at-fault driver is underinsured? You can carry both underinsured and uninsured coverages to maximize your protection. Understanding Uninsured Driver Property Damage (UMPD) Limits UMPD coverage can help pay to repair your car after an accident if the at-fault motorist is uninsured. The limit for this coverage is expressed as a maximum amount per accident, such as $10,000 or $25,000. Consider including this insurance protection if you don't have collision coverage. How Coverage Limits May Impact Your Insurance Cost When you increase your auto coverage limits, your insurance stands to pay more if a covered accident occurs. This is why you'll pay higher monthly premiums for the extra coverage. While decreasing your limits will lower your rate, it's generally not recommended as it exposes you to higher out-of-pocket expenses when you're liable for auto accident injuries/damages. Could you afford to pay for third-party losses/damages out of your own pocket if an accident ever happened? To ensure you're adequately covered for auto liability, consider your financial situation and assess the total value of your assets.

Do you have sufficient auto liability coverage to avoid out-of-pocket costs after an at- fault accident? At Spotlight Insurance Agency, we can help review your existing policy and close any coverage gaps. Contact us today to get started!