Download

1 / 15

150 likes | 165 Views

Explore the Adjusted Present Value (APV) rule in corporate finance with detailed examples and calculations in this informative guide. Learn about interactions between capital budgeting and financing.

E N D

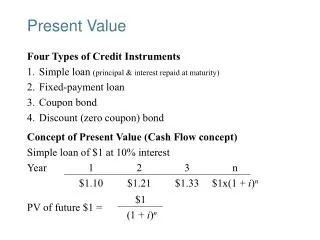

Advanced Finance2007-2008Adjusted Present Value Professor André Farber Solvay Business School Université Libre de Bruxelles

Interactions between capital budgeting and financing • The NPV for a project could be affected by its financing. (1) Transactions costs (2) Interest tax shield • There are two ways to proceed: • The APV Approach: • Compute a base case NPV, and add to it the NPV of the financing decision ensuing from project acceptance • APV = Base-case NPV + NPV(FinancingDecision) • The Adjusted Cost of Capital Approach: • Adjust the discount rate to account for the financing decision Advanced Finance 2008 04 APV

The Adjusted Present Value Rule • The most straightforward. Permits the user to see the sources of value in the project, if it's accepted • Procedure: • (1) Compute the base-case NPV using a discount rate that employs all equity financing (rA), applied to the project's cash flows • (2) Then, adjust for the effects of financing which arise from: • Flotation costs • Tax Shields on Debt Issued • Effects of Financing Subsidies • APV = NPV + NPVF Advanced Finance 2008 04 APV

APV - Example • Data • Cost of investment 10,000 • Incremental earnings 1,800 / year • Duration 10 years • Discount rate rA12% • NPV = -10,000 + 1,800 x a10 = 170 • (1) Stock issue: • Issue cost : 5% from gross proceed • Size of issue : 10,526 (= 10,000 / (1-5%)) • Issue cost = 526 • APV = + 170 - 526 = - 356 Advanced Finance 2008 04 APV

APV calculation with borrowing • Suppose now that 5,000 are borrowed to finance partly the project • Cost of borrowing : 8% • Constant annuity: 1,252/year for 5 years • Corporate tax rate = 40% Year Balance Interest Principal Tax Shield 1 5,000 400 852 160 2 4,148 332 920 133 3 3,227 258 994 103 4 2,223 179 1,074 72 5 1,160 93 1,160 37 • PV(Tax Shield) = 422 • APV = 170 + 422 = 592 Advanced Finance 2008 04 APV

Discounting Safe, Nominal Cash Flows “The correct discount rate for safe, nominal cash flows is your company’s after-tax, unsubsidized borrowing rate” (Brealey and Myers sChap19 – 19.5) • Discounting • after-tax cash flows • at an after-tax borrowing rate rD(1-TC) • leads to the equivalent loan (the amount borrowed through normal channels) • Examples: • Payout fixed by contract • Depreciation tax shield • Financial lease Advanced Finance 2008 04 APV

APV calculation with subsidized borrowing • Suppose now that you have an opportunity to borrow at 5% when the market rate is 8%. • What is the NPV resulting from this lower borrowing cost? • (1) Compute after taxes cash flows from borrowing • (2) Discount at cost of debt after taxes • (3) Subtract from amount borrowed • The approach developed in this section is also applicable for the analysis of leasing contracts (See B&M Chap 25) Advanced Finance 2008 04 APV

Subsidized loan • To understand the procedure, let’s start with a very simple setting: • 1 period, certainty • Cash flows after taxes: C0 = -100 C1 = + 105 • Corporate tax rate: 40%, rA=rD=8% • Base case: NPV0= -100 + 105/1.08 = -2.78 <0 • Debt financing at market rate (8%) • PV(Tax Shield) = (0.40)(8) / 1.08 = 2.96 • APV = - 2.78 + 2.96 = 0.18 >0 Advanced Finance 2008 04 APV

NPV of subsidized loan • You can borrow 100 at 5% (below market borrowing rate -8%). What is the NPV of this interest subsidy? Net cash flow with subsidy at time t=1: -105 + 0.40 × 5 = -103 • How much could I borrow without subsidy for the same future net cash flow? • Solve: B + 8% B - 0.40 × 8% × B = 103 • Solution: • NPVsubsidy = +100 – 98.28 = 1.72 Net cash flow After-tax interest rate PV(Interest Saving)=(8 – 5)/1.048 = 2.86 PV(∆TaxShield)=0.40(5 – 8)/1.048 = -1.14 + Advanced Finance 2008 04 APV

APV calculation • NPV base case NPV0 = - 2.78 • PV(Tax Shield) no subsidy PV(TaxShield) = 2.96 • NPV interest subsidy NPVsubsidy = 1.72 • Adjusted NPV APV = 1.90 • Check After tax cash flows • t = 0 t = 1 • Project - 100 + 105 • Subsidized loan +100 - 103 • Net cash flow 0 + 2 • How much could borrow today against this future cash flow? • X + 8% X - (0.40)(8%) X = 2 →X = 2/1.048 = 1.90 Advanced Finance 2008 04 APV

A formal proof • Ct:net cash flow for subsidized loan • r : market rate • D :amount borrowed with interest subsidy • B0 : amount borrowed without interest subsidy to produce identical future net cash flows • Bt: remaining balance at the end of year t • For final year T: CT = BT-1 + r(1-TC) BT-1 • (final reimbursement + interest after taxes) • 1 year before: CT-1 = (BT-2 - BT-1) + r(1-TC) BT-2 • (partial reimbursement + interest after taxes) • At time 0: • NPVsubsidy = D – B0 Advanced Finance 2008 04 APV

Back to initial example Data Market rate 8% Amount borrowed 5,000 Borrowing rate 5% Maturity 5 years Tax rate 40% Annuity 1,155 Net Cash Flows Calculation Year Balance Interest Repayment TaxShield Net CF 1 5,000 250 905 100 1,055 2 4,095 205 950 82 1,073 3 3,145 157 998 63 1,092 4 2,147 107 1,048 43 1,112 5 1,100 55 1,100 22 1,133 B0 = PV(NetCashFlows) @ 4.80% = 4,750 NPVsubsidy = 5,000 - 4,750 = + 250 APV calculation: NPV base case NPV0 = + 170 PV Tax Shield without subsidy PV(TaxShield) = + 422 NPV Subsidy NPVsubsidy = + 250 APV = + 842 Advanced Finance 2008 04 APV

Financial lease • A source of financing: • Extends over most of the economic life of the asset • Cannot be canceled • Similar to a secured loan • 2 parties: • Lessor: legal owner of the leased assset • Receives rental income (taxable) • Uses the depreciation tax shield • Lessee: user of the the leased asset • Lease payment tax deductible Advanced Finance 2008 04 APV

Lease versus borrow Advanced Finance 2008 04 APV

Calculating NPV of lease versus buy • Discount after-tax cash flow at the after-tax interest rate. = Cost of asset – Equivalent loan • Example: After-tax interest rate = 7.58% * (1-0.34) = 5% • NPV = 10,000 – 10,087.68 = -87.68 => buy and borrow Advanced Finance 2008 04 APV