Download

1 / 10

100 likes | 177 Views

Learn how to adjust rent based on repair and insurance liabilities in different lease types such as FRI, IRI, and IR. Understand the calculations and considerations involved in determining rent adjustments for outgoing costs. Explore examples for practical application in the valuation of lease purposes.

E N D

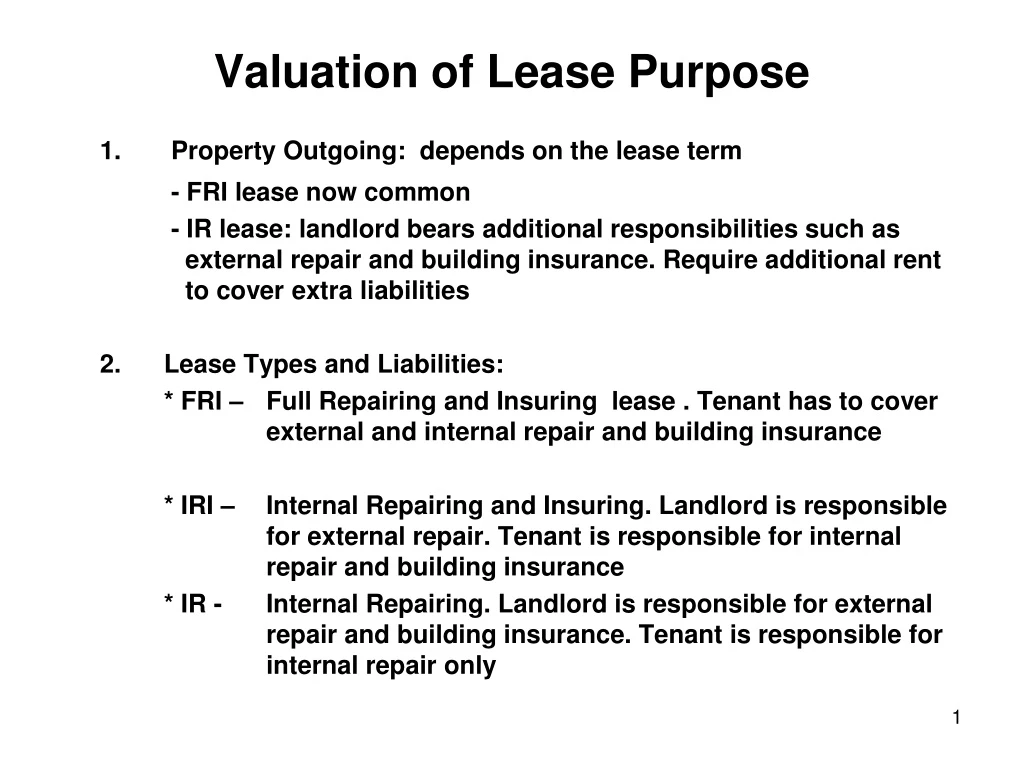

Valuation of Lease Purpose 1. Property Outgoing: depends on the lease term - FRI lease now common - IR lease: landlord bears additional responsibilities such as external repair and building insurance. Require additional rent to cover extra liabilities 2. Lease Types and Liabilities: * FRI – Full Repairing and Insuring lease . Tenant has to cover external and internal repair and building insurance * IRI – Internal Repairing and Insuring. Landlord is responsible for external repair. Tenant is responsible for internal repair and building insurance * IR - Internal Repairing. Landlord is responsible for external repair and building insurance. Tenant is responsible for internal repair only

Valuation of Lease Purpose a. Adjustment for repairing liabilities: - Examine lease to determine responsibilities - Estimate cost and adjust rent : + Reference to part cost + Use planned maintenance program information + Landlord sets aside what he can afford + Percentage of market rent (MR) : # Commercial 5/10% ext reps 5% int. reps # Retail 5 % ext reps 5% int. reps # Residential 30/40 % ext reps 10/20% int. reps b. Adjustment for insurance liabilities: - Not content but building ( fire etc) - Costs take into account + Cost of replacement of building + Professional fee + Cost converted into annual premium - Rent adjusted on following basis: + Annual cost ( premium) + Percentage basis – 2.5% - 5% market rent

Valuation of Lease Purpose c. Adjustment for liabilities: - Rent may include : + Business Rates + Management Expenses # Management Agents charge 5% to 10 % rent passing + Service charges ( provided not charge separately) # Common part maintenance/ decoration # Concierge/Reception # Heating # Lighting # Lift maintenance

Valuation of Lease Purpose 3. Rent Adjustment for Outgoing: Example : Value the freehold interest in unit C , a 1000 sq. factory on small industrial estate which is to be let to a mobile phone distributor on an FRI lease Reference: - Unit A on same estate just let at a rent of £32,500 p.a. on 10 years FRI lease with a rent review in year 5. The property is 500sq. m and freehold sold for £300,000. - Unit D on same estate is 2000sq. m and let 6 months ago on a 20 years IR lease with 5 year rent reviews at rent of £135,500p.a. - Unit B on the same estate and of the same size let 12 months ago at a rent of £61,000. The property was in poor condition needing substantial repair work to the roof, wall and services. The landlord agreed to bear responsibility for external repair

Valuation of Lease Purpose Solution: Adjust rent to conform the subject Unit ( Unit C): Analyze: Unit A : 1. Smaller so the rental value £/m² may be higher than 1000m² unit. 2. Recent letting and FRI lease 3. FRI lease so no need to adjust this rent Unit D : 1. Twice the size, so rental value £/m² may be lower for 1000m² 2. Relatively recent letting and slow market. 3. IR lease means landlord responsible for external repair and insurance

Valuation of Lease Purpose Unit B : 1. Same size as subject unit 2. Poorer condition 3. Land lord responsible for external repair Unit Rent AdjustmentNet RentArea M² Rent per m² A £32,500 None £32,500 500 £65 D £135,500 7.5% ext. reps £119,000 2000 £59.50 5% ins B £61,000 10% ext. reps. £54,900 1000 £55

Valuation of Lease Purpose Unit C : - Range will probably fall £60 - £65/m² on FRI basis - Say £62/m² - 1000m² x £62 = £62,000 - Freehold valuation: FRV £62,000 YP perp. At 11% 9.09 Capital Value = £565,000 Yield adopted based on sale price achieved on unit A

Valuation of Lease Purpose 4. Premiums - Traditional ( capital incentive) * A lump sum paid by tenant at start of lease in return for a reduction in rent. * Tenant immediately enjoys profit rent * Landlord takes capital sum lieu of rent. - Assignment Premium (leasehold valuation) * Paid by a purchaser or a leasehold interest i.e. new lessee buys existing lessee’s interest. * Equates to : capital value of profit rent * May include sum for goodwill, fixtures etc. so unable to reliably analyze. - Value from both tenant /leaseholder( YP Dual rate ) and freehold/ landlord’s( YP single rate) perspective.

Valuation of Lease Purpose Example 1 - A lessee has been granted a 15 year lease of a shop having a market rental value of £21,750. The agreement with the landlord is to pay £17,000 subject to the payment of a premium. There is a single review after 10 years. Freehold yield assumed to be 5% . Sinking fund rates currently at 3%. How much should be the premium be? Solution: - Profit rent is capitalized until point at which market rent is reached. Tenant’s perspective : Landlord’s perspective: MR pa: £21,750 MR pa. £21,750 Less Rent paid £17,000 Less rent to be paid £17,000 Profit Rent £4,750 Reduction in Rent £4,750 x x YP 10 yrs@ 6% & 3% 6.7921 YP 10yrs@5% 7.7217 (tax ignored) Premium £32,262 Premium £36,678 Agree at £34,500

Valuation of Lease Purpose Other Examples: Please refer to note for 5 year rent reviews example. Example of calculation of rent reduction.