Download

1 / 36

360 likes | 376 Views

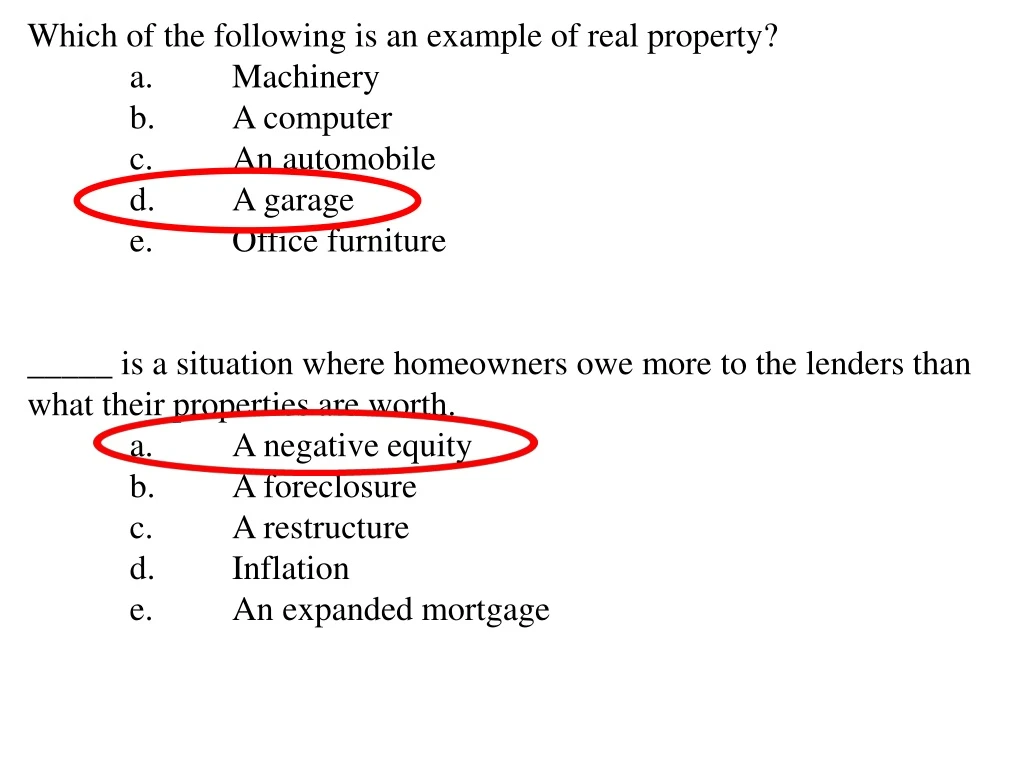

Which of the following is an example of real property? a. Machinery b. A computer c. An automobile d. A garage e. Office furniture _____ is a situation where homeowners owe more to the lenders than what their properties are worth. a. A negative equity b. A foreclosure

E N D

Which of the following is an example of real property? a. Machinery b. A computer c. An automobile d. A garage e. Office furniture _____ is a situation where homeowners owe more to the lenders than what their properties are worth. a. A negative equity b. A foreclosure c. A restructure d. Inflation e. An expanded mortgage

The majority of each monthly payment at the beginning of the loan goes to pay the: a. principal. b. interest. c. real estate taxes. d. homeowner’s insurance. e. private mortgage insurance. Which of the following is true of loan maturity? a. The longer the loan maturity, the higher the monthly payments. b. The shorter the loan maturity, the higher the total finance cost. c. The shorter the loan maturity, the higher the monthly payments. d. The longer the loan maturity, the lower the total finance cost. e. The shorter the loan maturity, the higher the prepayment penalty.

Russ and Lois have a home valued at $96,000 with an outstanding mortgage of $60,000. If their lender is willing to provide a home equity loan of up to 75% of the equity value of the home, how much can they borrow using a home equity loan? a. $0 b. $12,000 c. $27,000 d. $28,000 e. $36,000 Any credit card purchase will effectively be an interest-free loan if you: a. pay for the purchase within six months. b. make the minimum payment. c. pay off the entire balance on or before the due date. d. pay off the previous balance by the due date. e. receive a cash advance.

Are You Credit Worthy? 5 Factors of Credit Checks 1. Capacity to Pay-- -how long on job -how much -what other debts

2. Character -reputation -reliability -run-ins w/ law? -anything questionable 3. Collateral -size of capital -amount of wealth

4. Capital -down payment -savings/cash on had -pay closing costs -assures lender that you can manage money

5. Conditions -health of the economy -credit improvements -bounced back from a bad situation such as unemployment or identity theft.

*Secured Loans -loan with collateral *Unsecured Loans -loan guaranteed only with a promise to pay. *Your Responsibilities -pay on time -keep records

Mason Corporation borrows funds for the expansion of its business. The loan is secured with the office building. Therefore, the office building serves as _____ for the loan. a. a liability b. a collateral c. a debt d. an insurance e. a corporate deposit A legal claim that allows creditors to liquidate loan collateral is a: a. loan application. b. note. c. security claim. d. lien. e. loan rollover.

The cost of credit • **Whenever you use someone else’s money there is a cost. • Two Factors Affecting the Cost of Credit • Time- -longer the time to pay off, the • more interest you will pay. • Rate- -the higher the rate, the more • you pay.

**One way to calculate interest is by using the Simple Interest Formula. I=PxRxT I= Interest P=PrincipalR=Rate T=Time Borrowing $8,000 at 8% interest for 4 yrs. I = 8,000 x .08 x 4 I = $2,560- -Added to the payment **You will pay $10,560 total. **If your loan is calculated based on the simple interest formula, it will cost you more in interest because it is based on the full amount of the loan and not just the amount you owe after each payment.

**Lenders use a more complex method of calculating interest and payments called the Amortization Calculation Formula. This enables interest to be calculated only on the remaining principal. A= P r(1+r) (1+r) -1 We will be using https://www.amortization-calc.com/ A=payment amount P=principal r=interest rate per period n=total number of payments n

*Finance Charges v. Annual Percentage Rates -both mean cost of credit -expressed differently *Finance Charges--cost of credit in dollars and cents -interest -membership fees -late charges $

*Annual Percentage Rate-- -cost of credit in percentages -APR -includes all fees -helps with price comparison -always look for a low APR %

When the simple interest method is used to determine finance charges, the interest is calculated based on the: a. future value of the installments. b. average outstanding balance. c. actual balance of the loan. d. present value of all finance charges. e. future value of all finance charges. You want to borrow $1,000 at an interest rate of 10%. The most expensive method of calculating the dollar cost of the interest on the installment loan will be the: a. add-on method. b. double declining balance method. c. discount method. d. simple interest method. e. amortization calculation method

The most expensive method for determining finance charges on revolving credit would be the ____________. a. average daily balance (ADB) method including new purchases b. average daily balance (ADB) method excluding new purchases c. annual percentage rate (APR) method including new purchases d. annual percentage rate (APR) method excluding new purchases

The Credit Report **One of the most valuable assets one can have is a good credit report. Credit Report- -profile of your borrowing, charging, and repayment activities. There are 3 credit bureaus: 1. Equifax 2. Experian 3. TransUnion **These bureaus collect information from banks, credit card companies, merchants, and finance companies to create a snapshot of your credit worthiness.

Who Sees Your Credit Report? • Banks and Lenders • Potential landlords. • Potential employers • Life insurance companies • Courts • Government • Graduate Schools • You

Factors Affecting Your Credit Record • Whether or not you pay on time. • How long you have had a credit history. • How many open accounts you have. • How many inquiries have been made into your • credit record. • Have you been taken to court over nonpayment • Has there been a lien put on any of your • property. • Have you filed bankruptcy. • **A bad mark on your credit report stays on there for • 7 years. A bankruptcy stays on there for 10!

Protect Your Credit Score • Pay on time. • View your report periodically. • Report mistakes to credit bureau. • Have old information removed. • Report suspicious activity. • Limit your amount of available credit. • **It is much easier to build • and maintain a good credit • score than it is to repair a • bad one.

**FICO Score - a type of credit score lenders use to assess credit risk and determine whether to extend credit. **FICO scores consist of: 1.payment history 2.current level of indebtedness 3. types of credit used 4. length of credit history 5. new credit accounts FICO scores range from 300 to 850. Any score above 650 is considered good. Any score below 620 may have trouble borrowing or may have to borrow at higher rates (subprime borrowing)

Identity Theft • - -Crime in which someone illegally uses another person's personal data in some way that involves fraud or deception, typically for economic gain.

**With enough information, a criminal can take over that another’s identity to conduct a wide range of crimes. -False applications for loans and credit cards -Fraudulent withdrawals from bank accounts -Fraudulent use of telephone calling cards or online accounts -Obtaining other goods or privileges which the criminal might be denied if he were to use his real name.

What To Do If You’re a Victim of Identity Theft? • Call the companies where you know the fraud • occurred. • 2. Place a fraud alert and get your credit reports. • 3. Report identity theft to the FTC. • 4. File a report with your local police department.

Interest will usually begin to accrue immediately when you use a bank credit card to: a. make purchases. b. send payments. c. compute finance charges. d. get cash advances. e. meet a financial emergency. A payment made using _____ is equivalent to paying by cash. a. a retail credit card b. a debit card c. an affinity card d. a reward card e. a student credit card

**Where to Get a Loan • Commercial banks (large and competitive) • Savings banks (small) • Credit Unions -must be a member -usually lower rates • Savings and Loans -decreased in numbers since 1980 **Where NOT to get a Loan • Finance Company or Check-In-to-Cash --usually those who can’t borrow from banks --worst place for a loan (high interest)

Fixed Rate v. Variable Rate -When getting a loan, always choose the fixed rate. -If variable rate is chosen, then your interest rate could suddenly go up increasing your payments. Negative amortization- an increase in the principal balance of a loan caused by a failure to make payments that cover the interest due. The remaining amount of interest owed is added to the loan's principal. The monthly interest on your adjustable-rate mortgage was $690. You paid $650 as your monthly payment on the loan leading to an increase in the principal balance.

Mortgage points, also known as discount points, are fees paid directly to the lender at closing in exchange for a reduced interest rate. This is also called “buying down the rate,” which can lower your monthly mortgage payments. One point costs 1 percent of your mortgage amount. Essentially, you pay some interest up front in exchange for a lower interest rate over the life of your loan. If your lender charges 1.5 mortgage points on a house selling for $100,000, on which there is a $90,000 loan, the points will cost you ____________. $90,000 divided by .015 = $1,350

Fees charged by lenders as a condition of a mortgage loan that raises the effective rate of interest are called: a. mortgage points. b. down payments. c. add-on charges. d. commissions. e. loan discounts. A lender will usually require a loan-to-value ratio of _____ or less for a borrower to avoid having to pay private mortgage insurance (PMI). a. 75% b. 80% c. 85% d. 90% e. 95%

If the interest rates and monthly mortgage payments do not change over the life of your mortgage, you have _____. a. a reverse-annuity mortgage b. a fixed-rate mortgage c. an adjustable-rate mortgage d. a rollover mortgage e. a graduated-payment mortgage The monthly interest on your adjustable-rate mortgage was $690. You paid $650 as your monthly payment on the loan leading to an increase in the principal balance. This is an example of: a. a growing equity. b. a negative amortization. c. a fixed interest expense. d. a shrinking principal. e. an indexed equity.

If your lender charges 1.5 mortgage points on a house selling for $100,000, on which there is a $90,000 loan, the points will cost you ____________. a. $1,350 b. $1,500 c. $2,850 d. $150 Earnest money is the sum of money the home buyer pledges with the ____________. a. lender to guarantee the purchase b. seller to indicate the intent of purchase c. realtor for finding the desired home within a preset budget d. lender to originate the loan

Straight bankruptcy is allowed under ____________ of the bankruptcy code. a. Chapter 4 b. Chapter 7 c. Chapter 13 d. Chapter 19

Charge Accounts Buy Now, Pay Later!! 3 Types of Charge Accounts 1. Regular Charge Account -30 day charge -have 30 days to pay before interest is added. -Ex. Old country store

2. Revolving Charge Acct. -can continue to charge -minimum payment required -interest on unpaid balance 3. Installment Charge Acct. -Equal payments over time -large purchases

*Credit Cards -stores, restaurants, hotels -cash advances -high interest **Competition has brought the rates down some, but bad debt keeps them from going too low.

*Debit Cards -not a loan -transfers money electronically -first appeared in the 70’s -same as writing a check