Download

1 / 5

50 likes | 260 Views

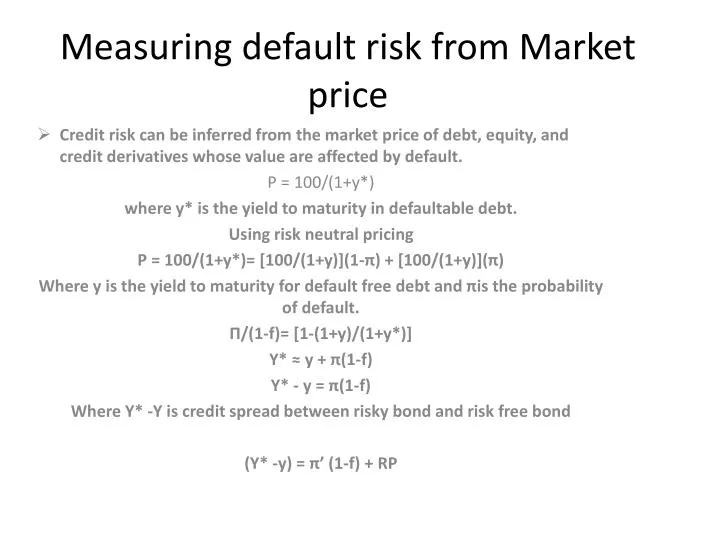

Measuring default risk from Market price. Credit risk can be inferred from the market price of debt, equity, and credit derivatives whose value are affected by default. P = 100/(1+y*) where y* is the yield to maturity in defaultable debt. Using risk neutral pricing

E N D

Measuring default risk from Market price Credit risk can be inferred from the market price of debt, equity, and credit derivatives whose value are affected by default. P = 100/(1+y*) where y* is the yield to maturity in defaultable debt. Using risk neutral pricing P = 100/(1+y*)= [100/(1+y)](1-π) + [100/(1+y)](π) Where y is the yield to maturity for default free debt and πis the probability of default. Π/(1-f)= [1-(1+y)/(1+y*)] Y* ≈ y + π(1-f) Y* - y = π(1-f) Where Y* -Y is credit spread between risky bond and risk free bond (Y* -y) = π’ (1-f) + RP

Consider 10 year US treasury strip and 10 year zero coupon bond issued by Citigroup rated A by Moody’s and S&P. The respective yields on the two bonds are 5.5 and 6.25 percent assuming semiannual compounding. Assuming recovery rate on the risky bond is 45 percent. What does the credit spread imply for the probability of default? π/(1-f) = [1-(1+y/2)^20/(1+y*/2)^20] π/(1-.45)= [1-(1+.055/2)^20/(1+.0625/2)^20] π= 12.776 percent π= 3.4 % historical default probability for an A rated credit over 10 years (Moody’s 1920-2002)

Example What would be a fair price of a $10 million loan to a counterparty with a probability of default of 2 percent and recovery rate of 40 percent, assuming the cost of the fund for the lender is equal to LIBOR? (y* -y) = π(1-f) = .02 ( 1-.40) = 120 bps Fair price = L + 1.2%

AIG: Risk Management Insurers in their main line of business are fairly diversified as the law of large numbers works for their advantage. AIG sold default insurance on all kinds of bonds issued by major corporations. Prudence required that AIG offset the potential losses stemming from bonds default, by taking short position on the underlying issuers stock. AIG sold default insurance on CDO packaged by various underwriters, Countrywide, Fanni, and Freddi

AIG: Why Did They Lose So Much? They sold default insurance, credit default swap, whose payoff is a binary; 0 or (Par)(1-f), where f is recovery rate on the bond in the event of default or Material events as covered in the ISDA master agreement. They could not or did not hedge their exposure to individual mortgagors with credit score at 650 or under in the sub-prime mortgage mess. As foreclosures mounted the protection buyers default insurance on the par value of the debts, triggered by default became liabilities due. AIG ran out of cash and unable to raise capital to pay of default insurance. Government agreed to bail out, by taking 80 percent equity interest on AIG stock for providing $85 billion loan at L+8.5%