Download

1 / 27

270 likes | 348 Views

COPS/Metro Workshop on the Health Insurance Marketplace. An Organizing Strategy. COPS/Metro. A broad-based organization with 33 dues-paying member institutions Foster a relational culture among institutions Develop leadership and capacity to shape the common good Organizing Process

E N D

COPS/Metro Workshop on the Health Insurance Marketplace An Organizing Strategy

COPS/Metro • A broad-based organization with 33 dues-paying member institutions • Foster a relational culture among institutions • Develop leadership and capacity to shape the common good • Organizing Process • Learn issues affecting families • Research possibilities to act • Act to shape public policy • Evaluate & Reflect on our actions, our development

Workshop Topics • Background on the state of healthcare • What is the Health Insurance Marketplace? • Who can benefit from it? • How does it work? • Small Group Conversations • Next steps

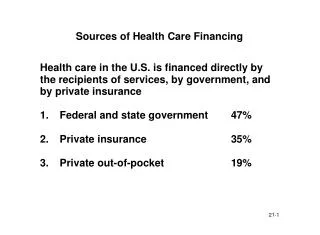

Background • There are 6.1 million uninsured Texans • 1 million of whom are children • Texas leads the nation • 390,000 uninsured in Bexar County • This is 23% of the population Source: Center for Public Policy Priorities www.cppp.org

What is the Health Insurance Marketplace? • In 2010, the Affordable Care Act (ACA) created the Marketplace (Exchange) • A one-stop shop to compare plans, benefits, costs • Provides tax subsidies to make insurance more affordable

What is the Health Insurance Marketplace? • Benefits include: • Preventive Care covered at 100% • Maternity & Newborn care • Prescription Drugs • Mental health and substance use disorder services, including behavioral health treatment • Children covered under parents’ plan until age 26 • Caps out of pocket expenses

Status of Insurance Marketplace? • Enrollment period: 10/1/13 – 3/31/14 • Coverage begins 1/1/14 • So do penalties for those qualified & not covered • 110,000 residents in Bexar County may qualify • HHS has granted resources to agencies to hire “Navigators” who can enroll participants • “Certified Application Counselors” can also enroll

Status of Insurance Marketplace? • Three Navigator agencies in Bexar County • About $1.2 million in federal grants • 22 Navigators • HHS requires 30 hours of training, including strict privacy protections • Governor Perry asked TDI to draft tighter regulations for navigators • Additional 40 hours of training; US citizenship

Four Health Plan CategoriesBased on % the plan pays on average

Terms to Know • Premium: The amount you pay monthly for health insurance coverage • Deductible:A fixed amount you pay per year before your insurance starts to make payments for covered medical services • Co-Pay: A fixed amount you pay for each healthcare service. • Lifetime Cap: The maximum amount your insurance will pay over your lifetime.

Terms to Know • Out-of-pocket: The amount you pay out of your own pocket for healthcare services. • Healthcare Navigators, • Application Assisters, • Certified Application Counselors, and • Champions for Coverage: • Different terms for people certified, trained and knowledgeable to help you understand your health coverage options

What determines my costs? • Your health insurance cost will be based only on four things: • Age • Where you live • Family Size • Whether you smoke *Pre-existing conditions will NOT be a factor*

Who can use the marketplace? • Small businesses • Families • Individuals who: • Are US citizens or legal residents • Live in the US • Are not in jail

Who cannot use the marketplace? • Undocumented residents • Residents with “deferred action” status (such as DACA) • People with Medicaid, CHIP or Medicare

Tax credits • Tax credits will be given on a sliding scale to those who qualify (family size/income) • People will pay no more than 9.5% of their income in health insurance premiums • For people who qualify, the government will send money directly to the insurance company.

For more information www.healthcare.gov 1-800-318-2596

To Enroll • Beginning October 1, 2013 • Online: www.healthcare.gov • By phone: 1-800-318-2596 • In person

Documents you need to apply • Social security card (or document number for legal immigrants) • Employer and income information for every member of your household who needs coverage (pay stubs, W-2) • Policy numbers of current health insurance plans covering members of your household • An Employer Coverage Tool for every job-based plan you or someone in your household is eligible for (even if not enrolled)

What happens if I don't get coverage? • If you don't have coverage as of 1/1/14 (employer, Marketplace, CHIP, Medicaid or Medicare) you will have to pay a tax penalty • 2014: 1% of income or $95 per person/year, whichever is higher • The fee for uninsured children is $47.50 per child/year • The most a family would have to pay in 2014 is $285/year • 2016: 2.5% of income or $695 per person/year, whichever is higher

Catastrophic Plans • People under 30 and some people with limited incomes may buy a "catastrophic" health plan. • Will have lower premiums, but high deductible • Protects you from very high medical costs (worst-case scenarios) • Generally requires you to pay all of your medical costs up to a certain amount, usually several thousand dollars. • Will include 3 annual primary care/preventive care visits with no out of pocket costs • People 30 and over who have received a “hardship” exemption may be able to buy catastrophic plans

*Disclaimer* • COPS/Metro will provide information with respect to the Affordable Care Act and how it may affect our families • COPS/Metro will not be engaged in the enrollment process. We can, however, refer families to reputable enrollment agencies who can assist with enrollment • While our organization accepts contributions for the broad purposes of the organization, we will not accept any contributions stemming from the Affordable Care Act (or any other public funds)