Download

1 / 22

220 likes | 329 Views

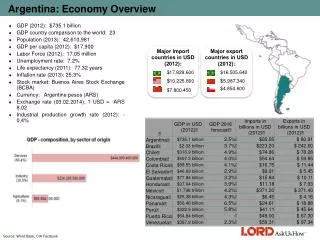

Georgian Economy Overview. June 2009 www.mof.ge. Economic Growth. GDP. Nominal GDP (US$bn). Real GDP growth, y-o-y (%). Source: Department of Statistics of Georgia, Ministry of Finance of Georgia. Components of nominal GDP (2008). Nominal 2008 GDP is US$12,797 mln.

E N D

Georgian Economy Overview June 2009 www.mof.ge

Economic Growth GDP Nominal GDP (US$bn) Real GDP growth, y-o-y (%) Source: Department of Statistics of Georgia, Ministry of Finance of Georgia Components of nominal GDP (2008) Nominal 2008 GDP is US$12,797 mln Source: Department of Statistics of Georgia Source: International Monetary Fund Georgian Economy Overview

Current Account Deficit Current account deficit Note: Updated as of 10 April 2009 *Donor inflows include both public and private sectors. Donor inflows in 2009 is adjusted according to the banking sector foreign debt outflows Source: National Bank of Georgia , Minister of Finance of Georgia Exports and imports** CAGR (‘04-‘09F): 16% CAGR (‘04-‘09F): 10% **Export & import of goods and services Source: National Bank of Georgia www.georgia.gov.ge Georgian Economy Overview May 2009

Diversified Trade Structure • WTO member since 2000 • Simplified customs regime since August 2006, new customs code became effective in 2007 and was upgraded in 2009 • No quantitative restrictions on trade • Zero tariff on the majority of goods • One of the two beneficiaries of the EU GSP+ Scheme in the CIS since 2006, granting local companies the right to export 7,200 categories of goods duty-free • Share of EU in exports up to 26% from 17% in 2003 • Georgia Turkey FTA was signed in 2008 Import structure* by country, 2008 Export structure* by country, 2008 Source: Department of Statistics of Georgia Source: Department of Statistics of Georgia Import structure* by product, 2008 Export structure* by product, 2008 Pharmaceuticals, 3.3% Source: Department of Statistics of Georgia * Export & import of goods only Source: Department of Statistics of Georgia www.georgia.gov.ge Georgian Economy Overview May 2009

Investment Inflows • Georgia has bilateral treaties on investment promotion and protection with 25 countries Net FDI breakdown by origin Net FDI Source: Department of Statistics of Georgia Source: Department of Statistics of Georgia Cumulative Net FDI Net FDI breakdown by sectors (2007 – 2008) Source: National Bank of Georgia, International Monetary Fund Source: Department of Statistics of Georgia Georgian Economy Overview May 2009 www.georgia.gov.ge

Fiscal and Monetary Performance Tax revenue performance Exchange rate evolution (GEL mln) Source: National Bank of Georgia Source: Ministry of Finance of Georgia Consumer price index (y-o-y) Source: National Bank of Georgia www.georgia.gov.ge Georgian Economy Overview May 2009

Monetary Performance NBG’s Gross FX Reserves Source: National Bank of Georgia NBG Interventions In 4m ‘09 gross FX reserves declined by US$ 85 mln only Source: National Bank of Georgia Georgian Economy Overview

The Donors’ Pledges of US$4.5 billion Aid by donors Aid by sectors Source: World Bank, European Commission Source: World Bank, European Commission • As of 1 May 2009, Georgia has already entered into agreements for or received 38.2%(US$1,731.2 million, 13.4% of 2009 forecast GDP) of the total donors pledge to private and public sectors • Additional projects have already been indentified and agreements have been reached on the amount of US$1,879.4 million (41.4% of total pledge, 14.6% of 2009 forecast GDP) to be formally committed in 2009 • Government of Georgia has been working and negotiating the terms and conditions on the remaining amount of US$924.4 million, 20.4% of total pledged amount www.georgia.gov.ge Georgian Economy Overview May 2009

The Donors’ Pledges of US$4.5 billion, cont’d Source: Ministry of Finance of Georgia Georgian Economy Overview May 2009

Economy’s Stimulus Package - GEL 2.2 bn, Social Package - GEL1.6 bn Source: Ministry of Finance of Georgia Georgian Economy Overview

Robust Banking Sector 2009 2008 1999 2000 2001 2002 2003 2004 2005 2006 2007 Dhabi Group • Georgia’s banking sector represents only a moderate contingent liability of the sovereign • Entirely privately owned since 1996 • No restrictions on foreign ownership of banks • Well capitalised with average BIS capital adequacy ratio of 19% www.georgia.gov.ge Georgian Economy Overview May 2009

Banking Sector Resilient Capital Adequacy Ratio (CAR) NPL to total loans Source: National Bank of Georgia, FSA Source: National Bank of Georgia, FSA Foreign debt outflow Foreign debt refinancing US$468.5 mln of US$548.5 mln banking sector debt, due in Q1 and Q2 0f ‘09, has already been repaid Source: National Bank of Georgia, FSA Source: National Bank of Georgia, FSA www.georgia.gov.ge Georgian Economy Overview May 2009

Recent Reforms - Taxation • Out of 21 taxes under the former tax code, only 6 exist today • Tax rates reduction timetable has been further accelerated in key tax rates in 2008 • This will provide a significant stimulus for the economy in 2009 and beyond • Georgia, over the last five years, has evolved into one of the most attractive low-tax jurisdictions in Europe Georgian Economy Overview

Special taxation systems have been adopted for the different regimes aimed at establishing new international financial institutions in the country, encourage economic growth, support sustainable development and the trade-transit function of Georgia Special Taxation Regimes Adopted www.georgia.gov.ge Georgian Economy Overview May 2009

Increasing Integration Into the Global Economy • The taxation in Georgia provides low, flat tax rates and double taxation avoidance treaties with 24 countries – a unique combination in the world • FTA with the CIS countries • FTA with Turkey • GSP+ with the EU • GSP with the US • Possible developments in the nearest future: • FTA with EU • FTA with USA Georgian Economy Overview

Customs Code Amendments Existing Requirements: The customs value of goods carried into the Georgian customs territory, processed from the goods carried out under the customs regime for processing the goods outside the customs territory will be diminished by the customs value of Goods declared and carried out for proscessing purposes. It is not defined whether the cost of transportation (carrying in and out) should be included. Proposal: It will be determined, that when carring in the processed good, as customs value shall be considered only the value added through the processing, with no regard to transportation costs. Georgian Economy Overview

Tax Code Amendments VAT Treatment During Exporting Services Existing Requirements: Under the existing requirements taxpayer rendering services outside the territory of Georgia is not eligible to claim VAT paybacks Proposal: Taxpayer acquires the right to claim VAT paybacks for services rendered outside the territory of Georgia Georgian Economy Overview

Tax Code Amendments Financial Lease Reason: According to the current law leasing is considered as supply of goods, yet for the purposes of VAT, it is considered as service and is taxed accordingly. Leased assets in its total value is considered as supply of goods, although essentially it is divided in two parts, because the lessor transfers an asset in discounted value to the lessee and receives interest from the given asset, which basically means income from certain financial service rendered, but not income generated from the supply of goods. Given the abovementioned, regulation of leasing is vague and inaccurate. Proposal: leasing must be considered as provision of service, taking into account certain conditions; Discounted value of income generated from leasing (10% rate applicable) shall not be less than the difference between the present value of a given asset and its expected residual value. At the end of the lease term, lessee may acquire the leased-asset at its residual value, which may not be higher than 15% of the fair market value of the asset at the beginning of the lease term. Georgian Economy Overview

Tax Code Amendments Partnership and Taxation of Income Reason: according to the existing tax code a partnership is obliged to allocate taxable income (profit) to the shareholders (partners), however, there is no complete mechanism of partnership taxation that would regulate total income, deductions, calculations, tax payment, tax declaration and other matters related to tax liabilities of the partnership and its members. Proposal: Taxable income of partnership will be allocated to its shareholders, in accordance with their shares, and will be included in the total income of the shareholders; Shareholder is obliged to tax the abovementioned income, with no regard whether the partnership has distributed the profit or not; Obligation of a partnership to submit the declaration is defined, and a partnership becomes liable to submit to the tax authority the information on the income received per share and the distribution of profit among the shareholders; If a member of a partnership is not a registered taxpayer, a partnership is obliged to withhold the tax, whereas the member may claim the credit in the same amount as taxed at source. Losses of a partnership will not be allocated to the shareholders and will be carried forward and reimbursed through the profit generated in the following years. Is effective from 1 January 2011 Georgian Economy Overview

Economy Remains Resilient Economy remains resilient due to the following reasons Donor support Diversified economy Reforms – strong economic fundamentals Georgia is committed to continuing reforms Continue building strong democratic institutions Rule of Law and judiciary reform Further lighting tax burden Economic liberalisation Georgian Economy Overview

Contacts Georgian Economy Overview