Download

1 / 22

220 likes | 260 Views

Delve into the Basic Inc. v. Levinson case of 1988 to grasp the nuances of securities fraud class actions. Learn about materiality, the bright-line tests rejected by the court, and the implications for corporate executives in disclosing information to financial markets.

E N D

Securities FraudClass Action “When talk is not cheap …” Last updated 25 Jan 12

Basic Inc. v. Levinson (US 1988) 1. F: What are the facts in the case? • What allegations did the plaintiffs make? • What kind of suit is this? What do the plaintiffs seek? • Who are the defendants? 2. I: What is the issue that the Court addresses? • What are the arguments of the defendants? • What are the responses by the plaintiffs? 3. R: What is the definition of materiality adopted by the Court? The Court’s ruling? • What alternatives did the Court have in choosing a definition? • What is an "agreement in principle" definition? a "price and structure" definition? • What is a "probability-magnitude" test? Is this how financial markets judge information's materiality? 4. A: Why does the Court adopt a case-by-case definition of materiality? • Why does the Court reject the bright-line tests urged by the defendants? • What are the advantages and disadvantages of the Court's approach? • After this case, when should corporate executives disclose merger negotiations? 5. C: What do you conclude about the case: • After this case, can corporate executives strategically misinform securities markets about merger plans? • Can a corporation engage in material silence?

Basic Inc. v. Levinson (US 1988) Issue 1: Were statements about merger negotiations "material"? ND Ohio: NO - Merger negotiations were not certain to become "agreement in principle" Summary judgment for defendants (no trial) 6th Cir: YES - statements were misleading and material, since denials were untrue Reverse and remand (send case back for further proceedings) Sup Ct: PERHAPS - materiality depends on facts of case, fact-finder must assess "probablity + magnitude" Reverse and remand (send case to 6th Circuit for further proceedings consistent with opinion / 6th Circuit will likely remand case to trial court)

Basic Inc. v. Levinson (US 1988) Issue 2: Can plaintiffs' reliance be presumed when misstatements are disseminated in public trading market? ND Ohio: YES - presumption of reliance when fraud on trading market Certify class action (common issues predominate over individual issues) 6th Cir: YES - YES - fraud-on-market theory OK Affirm Sup Ct: YES - Presumption of reliance OK, based on fraud on market theory Affirm fraud-on-market theory OK (in dicta, court explains how presumption might be rebutted)

“Loathed because he's so mean, feared because he's so powerful, Bill Lerach is the lawyer everyone in Silicon Valley hates.” Fortune Magazine, Sep. 2000 “"In 10 or 15 years you will be holding another hearing about a debacle in the securities market that will make you remember the S&L mess with fondness." Bill Lerach, congressional testimony (1995) “King of Pain” • Curriculum Vitae • 1946: born in working-class Pittsburgh • 1970: U Pittsburgh law grad • 1976: joins Milberg Weiss (San Diego) • 2004: moves to Lerach Coughlin Stoia Geller Rudman & Robbins (San Diego) • 2005: $7.2 billion recovery in Enron litigation ($45 over career) • 2007: pleads guilty to obstruction of justice (later Milberg Weiss) • 2009: disbarred by California State Bar • 2010: released from prison / “Circle of Greed” published

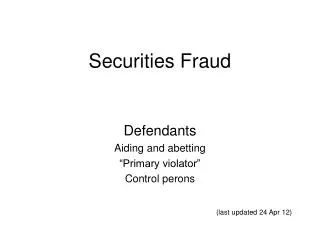

Federal Securities Fraud Class Action Litigation (lawsuits filed) Stanford Class Action Clearinghouse Pre-Reform Post-Reform

Securities Fraud Action When we deal with private actions under Rule 10b-5, we deal with a judicial oak which has grown from little more than a legislative acorn. Blue Chip Stamps v. Manor Drug Stores (US 1975) William Rehnquist

Securities Exchange Act of 1934 Section 10 -- Manipulative and Deceptive Devices It shall be unlawful for any person, directly or indirectly, by the use of any means or instrumentality of interstate commerce or of the mails, or of any facility of any national securities exchange-- (b) To use or employ, in connection with the purchase or sale of any security registered on a national securities exchange or any security not so registered … any manipulative or deceptive device or contrivance in contravention of such rules and regulations as the Commission may prescribe as necessary or appropriate in the public interest or for the protection of investors.

Rule 10b-5 • Plaintiff • Defendant • Elements • Material • Misrepresentation • Scienter (intentional) • Reliance • Causation • Damages • Transactional nexus • Jurisdictional nexus

Investigate corporate disclosures … • … identify corporate “fiction” … • … followed by “surprise” … • … resulting in price drop … • … identify “scienter” … • … file complaint …(e.g. Bay Networks, Inc) • … which must tell “fraud story” … • … to avoid “motion to dismiss”

Who pays? Average settlement: $80 MMAverage attorney fees: 20% 2006 data 2004 data 2003 data Atty fees overview

Holding shareholders (losers!) Settlement Insiders (insider trading gains) Corporation Corporate execs (D&O insurance) Buying shareholders (plaintiffs) Payment Selling shareholders (windfall winners!)

Class Counsel – Business Model • Get started • identify material corporate misrepresentations • find appropriate shareholders to act as class representatives • file a complaint in a court of class counsel’s choosing • Take care of legalities • defend the complaint against motion to dismiss (on legal grounds) • urge the judge to grant class action status to the litigation • send notice to class members, giving them an option to withdraw from the lawsuit • undertake discovery of information from the company and other sources • Close the deal • enter into settlement negotiations with company officials • champion any settlement before the judge • administer settlement funds • appeal any adverse decisions by the trial court judge