Download

1 / 13

140 likes | 237 Views

NET PRESENT VALUE. MATHEMATICS OF THE TIME VALUE OF MONEY NPV DEPENDS UPON THE SIZE, TIMING AND RISKINESS OF EXPECTED CASH FLOWS 3 WAYS TO DETERMINE NPV: FINANCIAL CALCULATOR FORMULAS TIME VALUE FACTOR TABLES. A Recipe for Financial Decision Makers.

E N D

NET PRESENT VALUE • MATHEMATICS OF THE TIME VALUE OF MONEY • NPV DEPENDS UPON THE SIZE, TIMING AND RISKINESS OF EXPECTED CASH FLOWS • 3 WAYS TO DETERMINE NPV: • FINANCIAL CALCULATOR • FORMULAS • TIME VALUE FACTOR TABLES

A Recipe for Financial Decision Makers • 1. Identify the SIZE and TIMING of all relevant cash flows on a time line. • 2. Identify the RISKINESS of the cash flows to determine the appropriate discount rate. • 3. Find NPV by discounting the cash flows at the appropriate discount rate. • 4. Compare the value of competing cash flow streams at the same point in time.

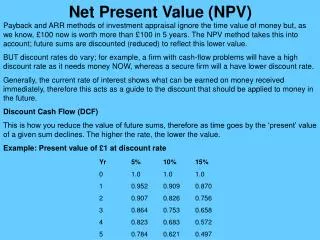

The Mathematics of Discounted Cash Flows • Compounding • Suppose we invest £1 at 9% for 2 years: 0 1 2 £1.00 £1.09 £1.1881 Future value = £1 ´ 1.09 ´ 1.09 = £1(1.09)2= £1.1881 Discounting Suppose we receive £1 discounted at 9% in 2 years: 0 1 2 £1.00 £0.917 £0.842 Slide T 4-2

–£1,000 £500 £700 0 1 2 -£1,000 £500 £700 0 1 2 Compounding Periods(first part) Annual Compounding At a discount rate of r = 9%: NPV = -£1,000 + £500/1.09 + £700/(1.09)2 = £47.89 • Semiannual Compounding • At a stated annual interest rate of 9% compounded semi-annually, the periodic discount rate is (9%/year) ¸ (2 periods/year) = 4.5% per six-month period: • NPV = -£1,000 + £500/(1.045) + £700/(1.045)2 = £44.86 • Effective annual interestrate = [1 + (r /m )] m – 1 • = [1 + (.09/2)] 2 – 1 = 9.2025% per year, • where m = 2 is the number of compounding periods per year. Slide T4-3a

EFFECTIVE ANNUAL INTEREST RATES • EAR = (1 + r/m))m -1 • Suppose that a cash flow stream of -£1,000, £500, and £700 is discounted at 9% compounded daily over a 2-year period. What is the NPV? • NPV = -£1,000 + £500/(1 + (.09/365))365 + £700/(1 + (.09/365))365 - 1 = £44.86 • EAR = (1 + .09/365))365 -1 = 9.42%

Example –£1,000 £500 £700 r = 9% 0 1 2 Future value = –£1,000(e.09 ´ 2) + £500(e .09) + £700 = –£1,197.28 + £547.09 + £700 = £49.87 Present value = –£1,000 + £500(e-.0 9) + £700(e-.09 ´ 2) = –£1,000 + £456.96 + £584.69 = £41.65 Verification £49.87 (e-.09 ´ 2) = £41.65 Compounding Periods(final part) • Continuous Compounding (e@ 2.718) • Future value = C0(erT ) • Present value = CT(e-rT ) • C0CT • 0 1 2 T-1 T … Slide T4-3b

… … Simplifications(first part) • Perpetuity: £100 per period forever discounted at 10% per period • C C C • 0 1 2 3 • PV = C/r = £100/.10 = £1,000 • Growing perpetuity: £100 received at time t = 1, growing at 2% per period forever and discounted at 10% per period • C C(1 + g) C(1 + g) 2 • 0 1 2 3 • PV = C/(r –g ) = £100/(.10 – .02) = £1,250 Slide T4-4a

Simplifications(second part) • Annuity: £50,000 per period for T = 20 periods • C C C C • 0 1 2 T-1 T • This cash flow stream is equivalent to • C C C C C • minus • 0 1 2 3 T T + 1 T + 2 • so that … … … [ ] ( ) ( ) 20 ( ) = £50 , 000 / . 1 ´ 1 - 1 / 1 . 1 = £ 425 , 678 Slide T4-4b

Simplifications(third part) • Growing Annuity: £50,000 growing at 2% per period for T = 20 periods and discounted at 10% per period • C C(1 + g) C(1 + g)2 C(1 + g)T-1 • 0 1 2 3 T • This cash flow stream is equivalent to • C C(1 + g) C(1 + g)2 • 0 1 2 3 • C(1 + g)TC(1 + g)T+1C(1 + g)T+2 • minus • TT + 1 T + 2 T + 3 … … … Slide T4-4c

Simplifications(final part) • so that Slide T4-4d

A Net Present Value Problem • What is the value of a 10-year annuity that pays £300 a year (at year- end) if the annuity’s first cash flow starts at the end of year 6 and the interest rate is 15% for years 1 through 5 and 10% thereafter? • 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 • 300 300 300 • • • • • • 300 • . • . • . Slide T4-5

TVM Problem • Your son just turned 5 today. You plan to start saving for his college education by making equal semiannual deposits in an investment account that pays a stated annual rate of 9.1% compounded semiannually with the first deposit to be made 6 months hence. You want to provide £24,000 per year for 4 years beginning when he is 19 years old. How much money should you deposits every six months until your son turns 18?

TVM Problem • You are 30 years old and wish to provide for your old age. Suppose you invest £5000 per year at an effective rate of return of 9% per year for the next 30 years, with the first deposit beginning one year hence. Beginning at age 61 you will tour the world for five years and will need £X per year at the start of each year. After you return to the U.S., you will withdraw £30,000 per year for the next 15 years. Assuming that the 9% return remains constant, what is the maximum £X you can consume each year during your world tour?