Download

1 / 19

1.09k likes | 2.57k Views

LEVERAGE. Concept of Leverage. Leverage indicates the tool which can lift heavy weight by using a little force. Leverage in financial terms means any financial technique which can serve this purpose. It shows the magnification of force. That is why it is also termed as Gearing .

E N D

Concept of Leverage • Leverage indicates thetool which can lift heavy weight by using a little force. Leverage in financial terms means any financial technique which can serve this purpose. It shows the magnification of force. That is why it is also termed as Gearing. • Leverage is the employment of an asset or fund for which the firm pays a fixed cost or fixed return.

Significance • The term leverage refers to a relationship between two interrelated variables. • In financial analysis, the leverage reflects the responsiveness or influence of one financial variable over some other financial variable. • It quantifies the relative changes in profit due to change in the sales. It depicts the change in fixed costs incurred to sell the goods.

Contd. • It helps the management in controlling operating costs or varying the profit with an element of risk. • It also helps in forecasting. • It helps in understanding the relationship between any two variables. • However, the two variables for which the relationship is to be established should be interrelated, otherwise, the leverage study may not have any useful purpose to serve.

Contd. • The two variables when varied show the relative changes. This variation is called “Degree of Leverage.” % Change in dependent variable Degree of Leverage = % Change in independent variable

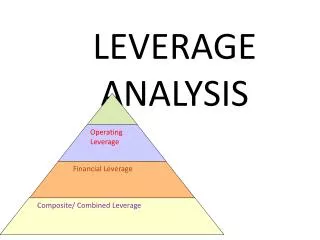

Types of Leverages: • Operating Leverage • Financial Leverage • Combined Leverage

Contd. • The relationship between sales revenue & EBIT is defined as Operating Leverage & relationship between EBIT & EPS is defined as Financial Leverage.

Contd. • The increase in the EBIT indicates fast recovery of fixed cost from sales revenues. • Lesser the fixed cost, more will be the EBIT and operating leverage.

Contd. • Increase in the Earning per Share (EPS) refers value addition in the shareholder’s wealth & vice- versa. • So, more the financial leverage more will be EPS.

Operating Leverage • The operating leverage shows the relationship between EBIT & Sales revenues. Contribution Operating Leverage = EBIT

Contd. • The degree of operating leverage (DOL) can be expressed as follows. % Change in EBIT DOL = % Change in Sales Revenue

Financial Leverage • The use of fixed charge sources of funds along with owner’s equity is described as financial leverage. • It focuses on earn more return on fixed charges funds (debt) than their costs. • High rate of financial leverage shows fast growth in EPS in the growing profit era. But in the declining profit phase it also shows fast decrease in the EPS.

Contd. • So, in short, we can say the leverage shows the pace of profit or loss. • It also shows relationship of fixed (Interest) & variable (Dividend) compensation paid or payable on debt & equity fund respectively.

Contd. EBIT Financial Leverage = ` EBT EBT = EBIT – I I= Interest

Contd. • The degree of Financial Leverage can be expressed as follows. % Change in EPS DFL = % Change in EBIT

Combined Leverage: Combined leverage is combination of both the leverages. Combined Leverage = Operating Leverage X Financial Leverage or EBIT Contribution Combined Leverage = X EBT EBIT or Contribution Combined Leverage = EBT