Download

1 / 28

290 likes | 585 Views

Mechanics of Options Markets. The size of option market and importance of options . The size of option market size is far smaller than futures markets. However, as a nonlinear derivative product, its theoretical significance is far greater than other linear products. .

E N D

The size of option market and importance of options • The size of option market size is far smaller than futures markets. However, as a nonlinear derivative product, its theoretical significance is far greater than other linear products.

A call option is an option to buy a certain asset by a certain date for a certain price (the strike price) A put is an option to sell a certain asset by a certain date for a certain price (the strike price) Options

Types of Options • A European option can be exercised only at the end of its life • An American option can be exercised at any time before the contract expires • There are many other types of options • Parisian option: Many convertible bonds are Parisian options • Asian options: Average price as strike price

Specification ofExchange-Traded Options • Expiration date • Strike price • European or American • Call or Put (option class)

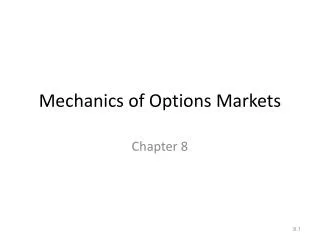

Profit ($) 30 20 10 Terminal stock price ($) 30 40 50 60 0 70 80 90 -5 Long Call on Microsoft Profit from buying a European call option on Microsoft: option price = $5, strike price = $60

Profit ($) 70 80 90 5 0 30 40 50 60 Terminal stock price ($) -10 -20 -30 Short Call on Microsoft Profit from writing a European call option on Microsoft: option price = $5, strike price = $60

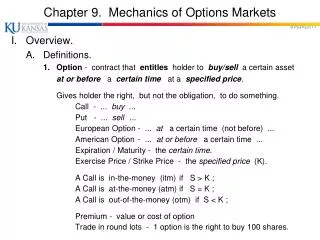

Profit ($) 30 20 10 Terminal stock price ($) 0 60 70 80 90 100 110 120 -7 Long Put on IBM Profit from buying a European put option on IBM: option price = $7, strike price = $90

Profit ($) Terminal stock price ($) 7 60 70 80 0 90 100 110 120 -10 -20 -30 Short Put on IBM Profit from writing a European put option on IBM: option price = $7, strike price = $90

Payoff Payoff K K ST ST Payoff Payoff K K ST ST Payoffs from OptionsWhat is the Option Position in Each Case? K = Strike price, ST = Price of asset at maturity

Terminology Moneyness : • At-the-money option • In-the-money option • Out-of-the-money option

Terminology • Intrinsic value • Value realized if exercised immediately • Time value • Value over level of intrinsic value • Example • Spot price: 53; strike price: 50; Call option price: 5 • Intrinsic value: 53 – 50 = 3 • Time value: 5 – 3 = 2

Market Makers • Most exchanges use market makers to facilitate options trading • A market maker quotes both bid and ask prices when requested • The market maker does not know whether the individual requesting the quotes wants to buy or sell

Warrants • Warrants are options that are issued (or written) by a corporation or a financial institution • The number of warrants outstanding is determined by the size of the original issue and changes only when they are exercised or when they expire

Warrants(continued) • Warrants are traded in the same way as stocks • The issuer settles up with the holder when a warrant is exercised • When call warrants are issued by a corporation on its own stock, exercise will lead to new stocks being issued

Executive Stock Options • Option issued by a company to executives • The purpose • When the option is exercised the company issues more stock • Usually at-the-money when issued • They cannot be sold • They often last for as long as 10 or 15 years

Executive Stock Options continued • What executives do when they are issued options? • Business Week, September 23, 2002 | Finance -- Stock repurchases can enrich execs at investors' expense • Execs may forfeit investing in projects with long term value so they have extra cash for repurchasing stocks, or the cash reserve becomes lower than it should be. • Discussion: Is there a perfect substitute?

Employee options • Startup or young companies often issue employee options. • If companies do well, early employees can become very wealthy. It is an very effective way to stimulate employees. • Bill Gates attributed the rapid growth of Microsoft in great part to its employee option program. • Do employee options have similar effect for large and mature companies?

Convertible Bonds • Convertible bonds are regular bonds that can be exchanged for equity at certain times in the future according to a predetermined exchange ratio

Convertible Bonds(continued) • Very often a convertible is callable • The call provision is a way in which the issuer can force conversion at a time earlier than the holder might otherwise choose • Amazon

Given that the value of an asset is affected by many factors and represented by relatively few financial instruments such as stocks and bonds, the financial market is far from complete. It is reasonable to expect that some derivative securities are created to better represent the values of the underlying assets. The convertible bond is an example.

For young and small firms not rated by a rating agency, it is difficult to issue straight bonds with low yield. At the same time, they may not want to issue additional shares at the current price level for this will dilute their ownership. Usually, small firms are volatile, which is often considered an unfavorable feature of a firm. However, the design of the convertible bond turns this feature into a positive one. The call options are highly valued since volatility is high for small firms. Because of the call option on the equity, convertible bonds pay lower coupon than the straight bonds. Since the convertible bonds properly “represent” the features of young and small firms, they have become increasingly popular among these firms, especially among high tech start-ups.

Price and volume of China Travel: Why trading volume is so high on some days?

Some background information • Parisian option. The option can be exercised only after the stock prices are over the strike price for a period of time. This feature is designed to prevent manipulation of share prices. • To force the conversion of the China Travel convertible bond into common shares, the daily closing price of China Travel stock had to stay over 5.49 HK dollars, the call price, which was 150% of the conversion price, for more than twenty of thirty consecutive trading days.

On August 6, 1997, the share price of China Travel went over the call price of HKD 5.49 for the first time. At that time, share prices of China Travel were higher than its CB prices, which is theoretically impossible. Figure shows the unusually high trading volume around that time, indicating strong market manipulation. However, the financial markets around Asia turned very bearish soon and China Travel managed to support its share price over the call price for nineteen days before it succumbed to the sharp fall of the general market. • For all its effort, China Travel could not convert the bond into equity.[1] The failure of conversion of China Travel gave a clear sign of the trend reversal. [2]

[1] According to the equity value of China Travel at the end of 1998, it would have made over sixty six million US dollar profit if the conversion had been successful, comparing with the total profit of seventeen million US dollar for the first half of the 1998. • [2] A trader confirmed that he spotted this signal and used it in trading. Several traders in different firms told me that borrowing shares of China Travel at that time was very difficult, although they didn’t understand why.

Homework • A trader buys a call option with a strike price of $45 and a put option with a strike price of $40. Both options have the same maturity. The call costs $3 and the put costs $4. Draw a diagram showing the variation of the trader’s profit with the asset price.

Homework • Explain why an American option is always worth at least as much as a European Option on the same asset with the same strike price and exercise date. • Explain why an American option is always worth at least as much as its intrinsic value.