Download

1 / 3

30 likes | 52 Views

Learn About rate of depreciation as per Income tax 1961, we are leading Top Chartered Accountant Company in Jaipur, CA firms for articleship in Jaipur, also Best Business Consulting CA Company in Jaipur and Top Accounting Audit Services and Best CA Firms in Jaipur

E N D

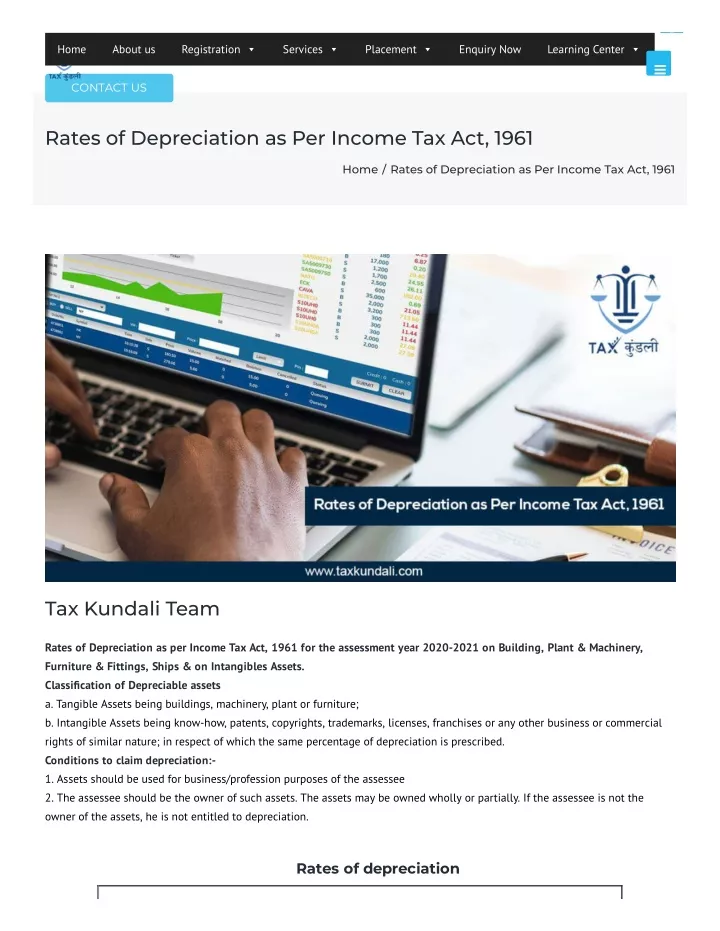

× Home About us Registration Services Placement Enquiry Now Learning Center type and press ‘enter’ CONTACT US Rates of Depreciation as Per Income Tax Act, 1961 Home / Rates of Depreciation as Per Income Tax Act, 1961 Tax Kundali Team Rates of Depreciation as per Income Tax Act, 1961 for the assessment year 2020-2021 on Building, Plant & Machinery, Furniture & Fittings, Ships & on Intangibles Assets. Classi?cation of Depreciable assets a. Tangible Assets being buildings, machinery, plant or furniture; b. Intangible Assets being know-how, patents, copyrights, trademarks, licenses, franchises or any other business or commercial rights of similar nature; in respect of which the same percentage of depreciation is prescribed. Conditions to claim depreciation:- 1. Assets should be used for business/profession purposes of the assessee 2. The assessee should be the owner of such assets. The assets may be owned wholly or partially. If the assessee is not the owner of the assets, he is not entitled to depreciation. Rates of depreciation

Block of assets Rate(% of WDV) 1. BUILDING (i) Residential 5 (ii) General 10 (iii) Temporary Structure 40 2. FURNITURE & FITTING 10 3. PLANT & MACHINERY (i) Motor Vehicles (a) Used in a business of running them on hire 30 If above(a) Acquired & put to use between 23-08-2019 to 31-03- 2020 45 (b) Other motor vehicles 15 If above(b) Acquired & put to use between 23-08-2019 to 31-03- 2020 30 (ii) Ships 20 (iii) Aircraft 40 (iv) Computer / Laptop(Including Computer Software) 40 (v) Books (a) Owned by assesses carrying on a profession 40 (b) Libraries business 40 (vi) Windmills & its equipments (a) Installed before 01-04-2014 15 (b) Installed on of after 01-04-2014 40 (vii) Pollution control equipments 40 (viii) Other plant & machinery 15 (ix) Oil wells 15 (x) Aeroplanes 40 (xi) Moulds used in rubber and plastic goods factories 30 4 INTANGIBLE ASSETS 25 Note:- 1. If the asset is put to use for less than 180 days during the previous year, then depreciation claim shall be restricted to 50 percent of the normal depreciation. Full depreciation as per the prescribed rate is allowed if the asset is put to use for 180 days

or more during the previous year. This restriction applies for the first year of acquisition and not in subsequent years. 2. Buildings include roads, bridges, culverts, wells, and tube-wells. 3. Intangible assets include know-how, patents, copyrights, trademark, licenses, franchises, or any other business or commercial rights of similar nature. COMPANY SERVICES Home Internal Audit About us Company Registration Enquiry Now Direct Taxation Contact Us Fill Your Return Finance SERVICES WORKING HOURS & ADDRESS GST Services TAXKUNDALI- Head Office 384-385, Tagore nagar , Ajmer Road, jaipur, Pin-302021 Indirect Taxation TAXKUNDALI- Branch Office Tax Filing 28, Sainipura, Post- Akoda, Teh- Phulera, jaipur ROC Email-id: info@taxkundali.com TDS Mobile phone: +91-9828107380 Working Hours: 09:00 AM – 08:00PM Sunday: Closed © 2019 taxkundali All rights reserved.

![Presumptive Income u/s 44AD of Income Tax Act, 1961 [w.e.f. AY 2011- 12]](https://cdn2.slideserve.com/4851709/slide1-dt.jpg)