Download

1 / 15

160 likes | 189 Views

IFC Response to Rising Food Prices Vipul C. Prakash Sr Manager, Agribusiness World Bank Group Donor Forum Paris May 20, 2008. Business Growth Reflects Increasing Importance of Private Sector and IFC Role in Agribusiness. IFC Investments in Agribusiness

E N D

IFC Response to Rising Food Prices Vipul C. Prakash Sr Manager, Agribusiness World Bank Group Donor Forum Paris May 20, 2008

Business Growth Reflects Increasing Importance of Private Sector and IFC Role in Agribusiness IFC Investments in Agribusiness (Measured by Annual Commitments, US$ million) • FY08 • IFC will invest USD 750m in Agribusiness • IFC Agribusiness Portfolio is USD 2 bn as of March 31, 2008 • 10% of expected transactions include cross-border, emerging market sponsors CAGR 31% IFC Agribusiness is well diversified across sectors IFC invests in Agribusiness globally

Sustainability: Setting Global Industry StandardsIFC/WWF Industry Sustainability Roundtables With IFC’s participation and the World Wildlife Fund’s leadership, global roundtables bring together stakeholders with a common goal of sustainable production for major global commodities Soy – Roundtable on Responsible Soy (RTRS) Approved “RTRS Principles” in Nov. 2006 • 1st Roundtable – Mar. 2005, Foz do Iguaçu, Brazil • Moving forward quickly • Key IFC Client members: Amaggi, SLC Agricola (Brazil), AGD Palm Oil – Roundtable on Sustainable Palm Oil • Adopted Principles & Covenants (P&C) in Oct. 2005, Mar. 2006 • First certified products could go to market this year • Key IFC Client : Wilmar (Singapore) Sugar – Better Sugarcane Initiative (BSI) • Will complete draft principles for a global sugar cane standard in 2008 • IFC approved project supporting development of Better Management Practice handbook for clients and industry Cotton – Better Cotton Initiative • IFC resumed support Beef - Brazilian initiative supported by IFC (began 2007)

Trade The World Bank Group and IFC Contributes to Global Agribusiness on Many Levels “It is the vision of the World Bank Group to contribute to an inclusive and sustainable globalization.” - Robert B. Zoellick, President, World Bank Group, March 14, 2008 Global Economic Environment Local Economic Environment WB CIT – Access to Markets CIT CIN Infrastructure (incl. Water)/Logistics CAG COC Inputs Farm Production Agri. Marketing Processing Marketing Distribution Retail CFN CGF Risk Sharing Facilities Fertilizers and other Chemicals CGM Pre-Harvest Finance Trade Finance Land WB – World Bank CIT – IFC Information Technology CIN – IFC Infrastructure CAG – IFC Agribusiness COC – IFC Oil, Gas, Mining & Chemicals CFN – IFC Funds CGF – IFC Global Financial Markets CGM – IFC Global Manufacturing Services 4

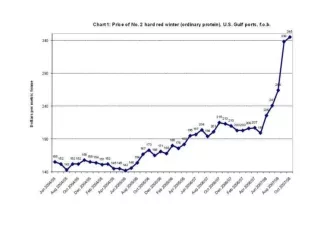

Agribusiness Action Plan for Rising Food Prices Food prices have risen substantially over past year Main drivers of food price inflation • Fundamentals • Supply and • Demand Financial Markets Supply and Demand • INCREASING DEMAND (food demand from emerging markets, diet changes, biofuel mandates) • LOWER SUPPLY (low stock to use ratio due to shortfalls in grain production, disappearance of reserve stocks, competition for land from biofuels) • DECLINING DOLLAR • SPECULATION AND INFLATION HEDGE Source: FAO, April 2008

IFC’s Response • Current crisis presents some risks but also provides significant opportunities for a vigorous supply response from the agricultural sector • The private sector will respond rapidly to the new price environment • IFC is well positioned to support private investors with a range of financial products and technical assistance • IFC nominated Agribusiness as a priority sector in 2006 • Significant budget increase in FY09 will underwrite a strategy of strong growth designed to: • Provide a short term response to the current food price situation • Significantly scale up new investments; and, • Reinforce focus on IDA countries, particularly in Sub-Saharan Africa

IFC is Well Positioned to Provide Interventions in the Short Term Short Term Response • Strengthen Supply Chain Coordination and Increase Liquidity via Working Capital Facilities • Prevent disruption of prefinancing • Ensure continued provision of essential inputs (seeds, fertilizers, chemicals, fuels). • Processors and traders in good standing eligible • Wings (Indonesia), Ecom (Africa/Asia), Noble (Argentina) • Increase rural credit through Wholesaling Facilities with Financial Institutions • Access to Finance - reach a new class of smaller clients (farmers, MSMEs) • Channel technical assistance to financial institutions (agribusiness credit analysis) and clients (environment and social, linkages, etc) • Agrofinanzas (Mexico), TSB (Tajikistan), Aval Bank (Ukraine)

IFC is Well Positioned to Provide Interventions that Address Long-Term Imbalances Fundamentals Of Supply • Productive land strategy • Bring land into sustainable production (CIS, Africa, Brazil) • Work with World Bank to improve land titling reform • Improve productivity/practices (seeds, fertilizer, chemicals, methods) • Regional focus on countries with upside potential: Argentina, Brazil, Russia, Ukraine • Investment Funds (Atera, Bulgaria), Input distribution (Rise, Ukraine), Farming (Rise, Ukraine; BGK, Russia; Salala, Liberia; GOPDC, Ghana) • Vertically integrated Agri Supply Chain Infrastructure • Strengthen and support the development of • Bulk ports and Terminals (Timbues, Aguirre) • Land, Rail and Sea Transport (UABL, TransAmerica) • Logistics and Warehousing (Merec, Trio, Ransa) • Modern retail (Rubliovskiy, EvroTech, Agrokor) • Water Efficiency and Irrigation Infrastructure (especially through PPPs and Municipalities) • Wholesaling Facilities with Financial Institutions, Processors and Traders toincrease rural credit to farmers and MSMEs. • Explore the systematic development of Financial Instruments related to Agiculture that deepen markets and allow for efficient intermediation of financing and risk management (e.g. warehouse receipts, GIRIF parametric insurance, weather-index insurance) Financial Markets

Access to Finance – Wholesaling to Agribusiness Significant increase in agricultural finance activities requires: Appropriate crop insurance technology targeted to small farmers Adequate underwriting capacity Adequate scale of micro-finance institutions to penetrate rural finance space Transfer of product development skills to interested micro-finance institutions IFC provides access to finance through: Banks Leasing companies Other non-bank financial intermediaries Other market participants IFC Loan or risk sharing to agri-focused lending or leasing facility Farmers Pre-harvest loans to certified farmers IFC Local Bank, Company or Financial Institution • Wholesaling projects committed and in preparation (FY08): • Agrofinanzas (Mexico) • Finterra (Mexico) • Ecom 9

IFC Will Prioritize Agribusiness Development in Sub-Saharan Africa Renewed investor interest for African natural resources: land, labor High agricommodities prices provide production opportunities that were only marginally competitive in the past Wholesale financing facilities often provide an entry point into IDA countries where direct investment possibilities may be limited. Current Partnerships: World Bank and the Gates Foundation: Doing Business report will provide new Agribusiness-related indicators in six pilot countries in Africa International Labor Organization: “Better Work” program in Advisory Services to identify and improve labor practices in Africa’s agri-product supply chains Explore other potential partnerships (e.g., African Development Bank) In Portfolio In Pipeline Past Client IFC Agribusiness Commitments (USD in mil) IFC Agribusiness will significantly scale up its investment program in Africa through the package of direct investment, wholesale financing and technical assistance 10 * Projected

Agribusiness Advisory Services are a Significant Part of IFC’s Value Addition Business Enabling Environment • Business enabling environment supported by FIAS • In collaboration with the World Bank, Doing Business report will provide new Agribusiness-related indicators in six pilot countries in Africa • Resource Management • Carbon footprint: clean production program • Water use efficiency • Renewable energy/ Energy use efficiency Sustainability • Malnutrition • Signed Agreement with GAIN (Global Alliance for Improved Nutrition) • Support clients to develop fortified foods for infants (6-24 months) • Supply Chain Management • Supporting small farmers to increase productivity and incomes. • Collaborating with IFC clients to develop traceability systems and apply standards to their supply chain Industry Specific Programs • Enterprise Value Addition • Corporate Governance practices • Environmental and Social standards • Food Safety / Quality Management Certification

Conclusions: IFC Agribusiness Development Plan Short Term Response Medium Term Response Long Term Response • Immediate budget increase for most impacted industry departments and advisory services business lines • Provide liquidity throughout the value chain • Trade finance • Working capital • Wholesaling finance • Supply side responses through global agricommodity players • Trade finance • Productive land • Improve supply chain infrastructure • Agribusiness development in Africa • Technical programs on the ground: productivity, access to finance • Improve logistics, product-to-market efficiencies • Reform agenda: regulatory / land / trade policy • Drive integration of small farmers to global agrisupply chain • IFC has already scaled up its activities and will continue to do so, to effectively provide financial and advisory services to its private sector clients and partners • Early results indicate that supply side, market driven responses to rising food prices will deliver results on the ground

IFC Investment in the Agribusiness Value Chain is Expected to Exceed US$1.3 Billion in FY 2008 IFC’s Goal: Deliver development impact along the global agri-supply chain, through investments and advisory services with the private sector, to create opportunities and improve peoples’ lives Note: in US$ Million Fertilizers and other Chemicals $152 $640 Project/CorporateFinance CIT – Access to Markets $143 Land $25 Inputs Farm Production Agri. Marketing Processing Marketing Distribution Retail Market Infrastructure Infrastructure/Logistics $11 Financial Institutions $245 Pre-HarvestFinance TradeFinance $87 Risk Sharing Facilities Note: The aggregated amounts listed next to categories above denote potential IFC investment size, subject to approvals

THANK YOU IFC GLOBAL AGRIBUSINESS TEAM Oscar Chemerinski Director, Global Agribusiness Vipul Prakash Senior Manager South and East Asia, Africa, Southern Europe Alzbeta Klein Manager Latin America, Eastern Europe, Central Asia Graham Smith Manager Portfolio Richard Henry Lead Economist