Download

1 / 29

290 likes | 312 Views

This case study delves into the tax implications of a transaction involving two LPs selling shares in an Australian company and examines key legal issues addressed by the Full Court decision. The analysis explores whether LPs are separately taxable entities, the source of gains, the application of tax treaties, and the interpretation of relevant tax laws. It provides insights into the determination of tax liabilities for partnerships with foreign partners investing in Australian assets.

E N D

RCF IV: The Full Court DecisionChair: Andrew Broadfoot QCGareth Redenbach, Victorian BarJames Strong, Victorian BarTax Bar Association CPD

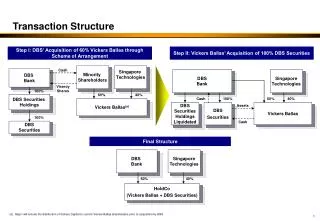

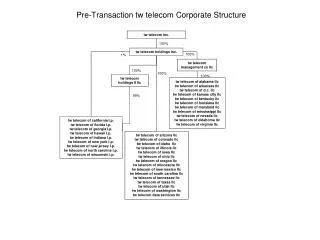

RCF IV Transaction Structure Two similarly structured LPs (RCF IV & RCF V) sold shares in Talison Lithium Ltd. Commissioner sought to impose tax on LPs as separately taxable entities pursuant to Division 5A of the ITAA 1936. Division 5A has been widely applied since 1992 on the basis that it creates a statutory fiction that an LP is a separate legal entity to its partners and taxed as a company. Limited Partners (US) Limited Partner (Other) Foreign Caymans RCF IV LP General Partner Caymans Australia Talison Lithium Ltd Australian Assets

RCF IV Transaction Structure RCF resisted the assessment on the grounds that: The partners had not derived a gain from an Australian source. The partners and not the partnership were the correct taxpayer. Taxing rights in respect of the US partners were allocated to the US under the US-Australia Double Tax Agreement. Any gain was not in respect of Real Property in Article 13 / Taxable Australian Property under Division 855. Limited Partners (US) Limited Partner (Other) Foreign Caymans RCF IV LP General Partner Caymans Australia Talison Lithium Ltd Australian Assets

At first instance the primary judge held: The gain on the Talison Lithium shares had an Australian source. Division 5A, and s 94V in particular, fixed liabilities on the partners as the correct taxpayers. RCF IV LP was not a taxable entity separate from its partners and the partners could assert treaty benefits against the assessment of the LP. Gain was Treaty protected as (subject to further calculation) not Div 855 ‘TAP’. RCF IV First Instance Limited Partners (US) Limited Partner (Other) Foreign Caymans RCF IV LP General Partner Caymans Australia Talison Lithium Ltd Australian Assets

Seven Issues Addressed by the Full Court Are LPs liable to tax separate from the partners? Who had been assessed – the LP or the partners? Was tax on the LP constitutionally invalid? Did the gain on disposal Talison Lithium Ltd have an Australian source? Can the RCF IV & V LPs rely on the US DTA? Can the RCF IV & V LPs rely on TD 2011/25? Did the primary judge err in accepting the valuation put forward by RCF IV & V? Limited Partners (US) Limited Partner (Other) Foreign Caymans RCF IV LP General Partner Caymans Australia Talison Lithium Ltd Australian Assets

Source Non-residents are, broadly, only taxable on gains with an Australian source. Source is a “hard practical matter of fact” (Nathan (1918) 25 CLR 183). The physical location of the mine in Australia and incorporation in Australia and some staff in Australia meant it was open for the primary judge to conclude there was an Australian source. The Full Court further emphasised that the sale was under a Federal Court of Australia scheme of arrangement and the locus of the scheme was analogous to the place of contract (Premier Automatic Ticket Issuers Ltd (1993) 50 CLR 268). Limited Partners (US) Limited Partner (Other) Foreign Caymans RCF IV LP General Partner Caymans Australia Talison Lithium Ltd Australian Assets

Is the LP a separate deemed company? The Full Court disagreed with the primary judge that s 94V required a conclusion the LP was not a separate “taxable entity” for the purposes of its assessment. The taxpayer and primary judge relied on section 94V of the ITAA 1936 providing: “The application of the income tax law to the partnership as if the partnership were a company is subject to the following changes…obligations that would be imposed on the partnership are imposed instead on each partner, but may be discharged by any of the partners” Limited Partners (US) Limited Partner (Other) Foreign Caymans RCF IV LP General Partner Caymans Australia Talison Lithium Ltd Australian Assets

Can the LP be assessed? The Full Court agrees at [33] that s 94V is capable of being read as implying that a corporate limited parentship is not liable to tax. However the Full Court prefers, for the reasons set out in the following slides, that the corporate limited partnership is assessed as a company and: s 94V recognises that a corporate limited partnership is not capable of being sued in debt for its tax liability; and instead provides that the persons who are capable of being sued (the partners) are liable in debt. Limited Partners (US) Limited Partner (Other) Foreign Caymans RCF IV LP General Partner Caymans Australia Talison Lithium Ltd Australian Assets

Can the LP be assessed? The Full Court relied on: Section 94J ITAA 1936 providing, “a reference in the income tax law [other than dividend, resident and resident of Australia and Div 355] to a company…includes a reference to a partnership.” Section 94K makes Division 5 ITAA 1936 (flow-through taxation) inapplicable to the partnership. Sections 6(1) ITAA 1936 and 995-1(a) ITAA 1997 providing person includes company and in turn a corporate limited partnership and each is a full self-assessment taxpayer. Sections 5-5, 4-5 and 4-1 ITAA 1997 providing income tax is due and payable by a company which, by reason of the foregoing, includes a corporate limited partnership. Limited Partners (US) Limited Partner (Other) Foreign Caymans RCF IV LP General Partner Caymans Australia Talison Lithium Ltd Australian Assets

Can the LP be assessed? Further, sections 94L - 94O ITAA 1936 and Divisions 960 and 202 ITAA 1997 provide for franking of distributions by a corporate limited partnership. The Full Court plurality at [30]: “These provisions operate on the basis that the corporate limited partnership is assessable on its income before distribution. These provisions also operate on the basis that the partners are only assessable under s 44 of the ITAA 1936 on distributions paid or credited…This is to be distinguished with the situation of partnerships under Division 5” [emphasis original] This analysis may create issues for taxpayers on future transactions. Limited Partners (US) Limited Partner (Other) Foreign Caymans RCF IV LP General Partner Caymans Australia Talison Lithium Ltd Australian Assets

The Full Court finds at [75] limited partners can invoke treaty benefits against recovery proceedings but not for the purposes of a Part IVC appeal by the LP against its liability. Instead, found the LP must contest the liability. The plurality (Davies J disagreeing on this point) state the LP can assert treaty benefits if it is formed in the US and its members are taxed in the US (RCF III (2013) 95 ATR 504per Edmonds J). Davies J preferred the view that provided the partnership gains are taxed in the US the treaty may be available. What does this mean in practice? Can the individual partners invoke treaty benefits? Limited Partners (US) Limited Partner (Other) Foreign Caymans RCF IV LP General Partner Caymans Australia Talison Lithium Ltd Australian Assets

RCF IV – Practical Considerations Recall the plurality (Davies J agreeing on this issue) at [30]: “the corporate limited partnership is assessable on its income before distribution… the partners are only assessable…on distributions paid or credited” What if the GP (or its bankers) receives a freezing order? Recall DCT v Bluebottle [2006] NSWCA 260 at [77], “the Commissioner may therefore trigger s255(1)(b) at an earlier point of time to when payment is required, in order to compel retention, pending there being a specified date to pay the tax by further notice.” Do partners with treaty benefits have any remedies? Limited Partners (US) Limited Partner (Other) Foreign Caymans Non-US LP General Partner Sale Caymans Australia Dispose Co Cash Proceeds

RCF IV – Practical Considerations Treaty benefits may be available if a US or other treaty partner LP is used. For PE / hedge funds / etc bringing foreign money onshore into the US is often very unappealing from a US regulatory perspective. How do you prove which partners are entitled to treaty benefits if a “good” LP is used? Partnership constitution is usually a highly guarded commercial secret. What about LLCs? Does the reasoning about “person” mean they can individually assert treaty benefits (c.f. the partners and n.b. hybrid rules). Limited Partners (US) Limited Partner (Other) US LP General Partner Sale US Australia Dispose Co Cash Proceeds

Issue 6 - Can the LP’s rely on TR 2001/25? (Extract) “Income tax: does the business profits article (Article 7) of Australia’s tax treaties apply to Australian sourced business profits of a foreign limited partnership (LP) where the LP is treated as fiscally transparent in a country with which Australia has entered into a tax treaty (tax treaty country) and the partners in the LP are residents of that tax treaty country?” Limited Partners (US) Limited Partner (Other) Foreign Caymans RCF IV LP General Partner Caymans Australia Talison Lithium Ltd Australian Assets

Issue 6 - Can the LP’s rely on TR 2001/25? “Ruling Yes, to the extent the business profits are treated as the profits of the partners (and not the LP) for the purposes of the taxation laws of the country of residence of the partners; the profits are not dealt with under another Article of the Treaty (such as Article 13); and the resident partners meet any other applicable tax treaty requirements.” [Emphasis added] Limited Partners (US) Limited Partner (Other) Foreign Caymans RCF IV LP General Partner Caymans Australia Talison Lithium Ltd Australian Assets

Issue 6 - Can the LP’s rely on TR 2001/25? What was the effect of Article 7 of the DTA if it applied? Art 7(1): The business profits of an enterprise of the US, shall be taxable only in the US unless the enterprise carries on business in Australia through a PE situated in Australia. To whom did it apply? Full Court at [85] “the benefit of the ruling is not confined to the partners of [the LP’s] but extends to any taxpayer who can benefit from it in a Part IVC tax appeal” Limited Partners (US) Limited Partner (Other) Foreign Caymans RCF IV LP General Partner Caymans Australia Talison Lithium Ltd Australian Assets

Issue 6 - Can the LP’s rely on TR 2001/25? Were the conditions in the ruling satisfied? Key condition: the profits were not dealt with under another article of the Treaty (such as Article 13) Court at [86]: “profits will be so “dealt with”, in our view, if they fall within the carve-out which is set out in Art 7(6). At [87]: It may be odd to ask whether business profits of a taxpayer, should be dealt with separately by another Article of the DTA, when the taxpayer is not itself otherwise eligible to invoke directly DTA protection. Limited Partners (US) Limited Partner (Other) Foreign Caymans RCF IV LP General Partner Caymans Australia Talison Lithium Ltd Australian Assets

RCF IV & V LP Issue 6 –Did Article 13 apply to the profits? Alienation of real property Article 13(1): Income or gains derived by a resident of [the US] from the alienation of..real property situated in [Australia] may be taxedin Australia. Article 13(2)(b) ‘real property’ in Art 13 means: 13(2)(b)(i) Real property as defined in Article6 (includes rights to exploit…natural resources situated in Australia) 13(2)(b)(ii) - [shares] in a company, the assets of which consist wholly or principally of real property situated in Australia..... …extension of Art 13(2)(b)(ii) by s 3A(2) of International Tax Agreement Act 1953 (‘Lamesa amendments’) Sale – Art 13? Caymans Australia Talison Lithium Ltd Minerals Australia WA mining project

RCF IV & V LP Division 855 disregards a capital gain by a foreign resident from sale of shares in a company where: Sum of Market value of TARP assets exceeds Sum of Market value of non-TARP assets TARP = Taxable Australian Real Property: Land (including leasehold interests) Mining quarrying or prospective right (MQPR) Non-TARP = Everything else Issue 6 –Why was Div 855 relevant here? Sale – Div 855? Caymans Australia Talison Minerals Australia WA mining project

‘Greenbushes Lithium Project’ Integrated Lithium Mining and Processing Operations at Greenbushes, WA. Pagone J found Div 855 would have exempted gain (had it applied) as: “Mining” authorised by Mining Lease (MQPR/TARP) was limited to (upstream) extraction activity and excluded further downstream processing’ Downstream Processing was authorised by a General Purpose Lease (non-MQPR/TARP). Scope of TARP assets? Valuation of TARP assets Mining Lease 2 General Purpose Leases Div 855 requires a capital gain derived by a foreign resident to be disregarded unless the relevant CGT Asset disposed is Taxable Australian Property (TAP) TAP relevantlyincluded an Indirect Australian Real Property Interest – a membership interest (share) that satisfied non-portfolio interest test (10% threshold) and the Prinicpal asset test. Issue 6 WouldDiv 855 have applied? MQPR defined in s995-1 included: (a) an authority, licence, permit or right under an * Australian law to mine, quarry or prospect for * minerals, * petroleum or quarry materials; or (d) any rights that: (i) are in respect of buildings or other improvements……that are on the land concerned or are used in connection with operations on it; a (ii) are acquired with such an authority, licence, permit, right, lease or interest.

ML 01/06 GPL 01/2 –’Tailings Dam’ GPL 01/1 – processing

RCF IV & V LP Full Court at [167]: Object of mine was to win lithium concentrate (Cf BHP) All processing took place at mine site Processing was a step in single integrated process to produce product (Robe River) Definition of verb “to mine” in Mining Act relevant (Henderson) “More like Henderson than BHP” Result: General Purpose Lease was MQPR Issue 6 – why was Lithium processing, “mining?” Sale – Div 855 Caymans Australia Talison Lithium Ltd Minerals Australia WA mining project

RCF IV & V LP Issue 7 – Valuation – netback methodology Full Court at [221]: “The [netback methodology] was inapt to determine the value of the assets in the present case because of the conclusion that we have earlier reached that the value of the mining leases lay beyond the right merely to extract minerals and that, irrespective of that, the general purpose leases were TARP……. ……Accordingly, the hypothetical and rigid divide in operations was artificial” Note : intangible value of lease extensions also TARP Sale – Div 855 Caymans Australia Talison Lithium Ltd Minerals Australia WA mining project

Some implications of Issues 6 and 7 Overall Result – Sale of Non-portfolio Interest in Mining Company with exclusively Australian operations by a foreign private equity LP ruled taxable on revenue account with no Treaty Relief for LP (except as provided by Ruling) (and in practice for partners also), however: • Scope of Article 13 vs Div 855 not established by Full Court: - Sale of 5% interest on revenue account? (Satyam) - Treatment of partnership interest? (Danvest) • Definition of “mining operations” for MQPR purposes a question of fact and degree (relevant for Division 40 for broadly) – WA Mining Act relevant • Valuation methodology criticized (compare methodology in RCF III) – although more due to outcome of MQPR analysis but note value of lease extensions.

RCF IV – Concluding Comments RCF IV could still seek special leave to appeal to the High Court. Possible Alternative Structure? Non-US Partners LP US Partners LLC Not US US Cayman GP Sale Caymans Australia Target

Thank You Tax Bar AssociationAndrew Broadfoot QCGareth RedenbachJames Strong