Download

1 / 22

360 likes | 1.48k Views

The Concepts Of Interest, Usury And Riba. Introduction Definition of riba The prohibition of riba Types and classifications of riba The differences between riba and profit Conclusion. INTRODUCTION. Interest in the modern financial world is commonplace.

E N D

The Concepts Of Interest, Usury And Riba • Introduction • Definition of riba • The prohibition of riba • Types and classifications of riba • The differences between riba and profit • Conclusion

INTRODUCTION • Interest in the modern financial world is commonplace. • It is a staple feature of capitalist system that values profits above everything else, via competition rather than co-operation. • Despite the amount of wealth that the Western economic system has created, there are major concerns over the huge disparities that have developed between rich and poor.

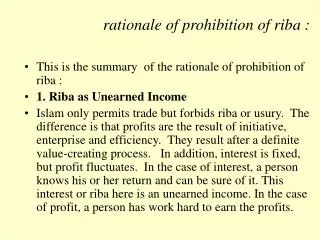

THE MEANING OF RIBA • Riba has been extracted from Raba. It means addition, increase. So, riba literally means to increase, to grow to rise, to add, to swell. It is, however, not every increase or growth which has been prohibited by Islam

THE MEANING OF RIBA • In the Shari’ah, “riba” technically refers to the premium that must be paid by the borrower to the lender along with the principal amount as a condition for the loan or for an extension in its maturity. • In this sense riba has the same meaning as interest in accordance with the consensus of all jurists without any exception. • So the Holy Qur’an and the Hadith do not make any such difference between usury and interest. Interest and usury both are taken as synonymous for the Arabic word riba.

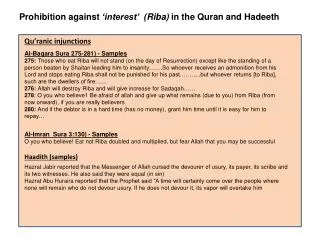

PROHIBITION OF RIBA IN THE HOLY QURAN • In several verses of the Holy Qur’an, Allah(swt) has mentioned the consequences of riba. • The Qur’an did not declare the prohibition of riba in the early stage of revelation, rather we find that the complete prohibition of interest came sequentially.

“Those who devour usury will not stand except as stands one whom the evil one by his touch hath driven to madness. That is because they say: ‘Trade is like usury.’ But Allah hath permitted trade and forbidden usury. Those who after receiving direction from their Lord, desist, shall be pardoned for the past; their case is for Allah (to judge). But those who repeat (the offence) are companions of the fire, they will abide therein (forever)” (2:275) • “That they took riba (usury), through they were forbidden and that they devoured men’s substance wrongfully – We have prepared for those among men who reject faith a grievous punishment.” (4:161)

PROHIBITION OF RIBA IN THE HADITH • Jabir reported: The Prophet (saw), cursed the receiver and the payer of interest, the one who records it (the contract) and the two witnesses to the transaction and said, “they are all alike (in guilt).” • Abu Hurayrah (ra) narrated that the Prophet (saw) said: “”God would not allow four persons to enter paradise or to taste its blessings: he who drinks wine, he who takes riba, he who usurps an orphan’s property without right and he who is undutiful to his parents.”

TYPES OF RIBA • RIBA AL- NASI’AH • The term nasi’ah means to postpone or to wait and it refers to the time period that is allowed for the borrower to repay the loan in return for the addition of the premium. • Hence it refers to the interest on loans. The prohibition of riba al nasi’ah essentially implies that the fixing in advance of a positive return on a loan as a reward for waiting is not permitted by the Shari’ah[i][14].

TYPES OF RIBA • RIBA AL-FADL • Riba al-fadl is the excess over and above the loan paid in kind. It lies in the payment of an addition by the debtor to the creditor in exchange of commodities of the same kind. • It is related that Abu Said al-Khurdi said: “the Prophet Muhammad (saw) has said that gold in return for gold, silver for silver, wheat for wheat, barley for barley, dates for dates and salt for salt, can be traded if and only if they are in the same quantity and that is should be hand to hand. If someone gives more or takes, then he is engaged in riba and accordingly has committed a sin.”

TYPES OF RIBA • Riba al-Qard • The term qard means to borrow; • Ribaqard refers to a benefit or profit which creditor has to pay along with the amount of loan because of duration (late payment). • The benefit/ profit can be a cash or an usufruct (manfa’ah/ benefit from object). • Any attempt to get profit from loan contract is considered ‘akl riba’ (taking interest) as in maxim of fiqh: “Kull qard jarra naf’an fahuwa riba”, which means: All loans lead to a benefit are riba (i.e. interest). • Riba al-qard is a part of riba al-nasiah. (riba a-duyun)

TYPES OF RIBA • Riba al-Yad • The term yad means hand. • Riba yad refers to a benefit derived from the duration between delivery and acceptance of contracted item and price. • In money exchange (e.g. RM to USD), the delivery of money from money changer to a buyer shall take place at the same time and place (same majlis) where the money changer accepted the buyer’s money. • In cash and carry contract, the seller has to surrendered the contracted item whereby he holds the payment from buyer. • Delay in surrendering the contracted item or the payment, in cash contract, from any side of the parties involved, is prohibited because that party can access to the benefit of received item but not the other party.

• If merchant can sell a commodity for a price higher than his cost, he can also sell his money for a higher price than its face value • If one can lease his property and charge a rent against it, he can also lend his money and claim interest thereupon The Nature of Money One of the presumptions of the theory of interest is that MONEY HAS BEEN TREATED AS A COMMODITY ISLAMIC PRINCIPLES DO NOT SUBSCRIBE TO THIS

In Islam, MONEY and COMMODITY have different characteristics and uses

MONEY COMMODITY • has no intrinsic utility • cannot be utilized in direct fulfilment of human needs • can only be used for acquiring some goods & services has intrinsic utility • can be utilized directly without exchanging it for some other thing • Money has no quality except as a measure of value and medium of exchange - all same denomination money equals 100% to each other A commodity can be of different qualities • Money cannot be pin-pointed in a tansaction of exchange Commodity sold or purchased are identified to a particular unit

Islamic alternatives to interest Rates • Trading as a way to avoid interest. • Trading through various types of contracts such as sale and purchase contracts, partnership contracts, leasing and so on.

The differences between interest and trade • Firstly: • In trade the purchaser and the vendor exchange on the basis of equality. For the purchaser derives profit from that which he purchased from vendor, while the latter gets profits in consideration of the labour and time. • In interest the creditor get for himself a definite amount of money for his loan but all that the debtor is certain of is the time to use the money. During this time period it is not always possible for debtor to make a profit.

Secondly: • From the point of view of trade, the moment a commodity is exchanged for its price, the transaction come to an end. • But in the case of interest, the debtors actually spends the amount borrowed from the creditor and has to return the same amount with an addition by way of interest.

DIFFERENCE BETWEEN PROFIT AND INTEREST (1) • The settlement of profit between the buyer and the seller is made on equal terms. The buyer purchases the article he needs and the seller gets profit for the time, labour and brains he employs in providing that article to the buyers. • In the case of interest, obviously the debtors cannot settle the transaction on equal terms with the creditor because of his weaker position. • As far as the money lender is concerned, he gets that fixed sum of interest which he considers as his profit.

If the debtors spends the borrowed money in fulfilling his personal needs, the time factor definitely does not bring any profit at all. • And if he invests that money in trade, commerce, industry, agriculture, then there are equal chances of profit or loss. • Thus lending money at interest might bring a guaranteed and fixed profit to one party and loss to the other, or a guaranteed and fixed profit to one party and an uncertain and indefinite profit to the other.

DIFFERENCE BETWEEN PROFIT AND INTEREST (2) • The trade charges his profit, however high it may be, once and for all, but money lender goes on charging interest over and over again and goes on increasing with the passage of time. • The profit which the debtor make on money of the creditors, however, large it may, has after all its own limits, but there is no limit to the interest the creditor may charge on his money. • He may, as something actually happens, receive all the earning of the debtor, may even deprives him of all the means of livelihood or of the articles of his personal use and still might have the same amount of debt against him that was at the time of borrowing.

DIFFERENCE BETWEEN PROFIT AND INTEREST (3) • The transaction in trade comes to an end as soon as the article and its price change hands. After this the buyer is not required to return anything to the seller. • As regards the rent of furniture, house, land, the lent thing is not itself spent up but it returned to the owner after the term. • But in the case of the principle the debtor has to spend it first and the reproduce it and return it, to the creditor along with the interest. Thus the debtor runs a double risk, he has to reproduce the principle and also to produce its interest.