Download

1 / 26

270 likes | 399 Views

ACA Health Coverage Enrollment Overview. Center on Budget and Policy Priorities September 24, 2013. Topics. Who is eligible for coverage under the health care law? What is the premium tax credit? How is the premium tax credit determined?. Overview of Major ACA Components.

E N D

ACA Health Coverage Enrollment Overview Center on Budget and Policy Priorities September 24, 2013

Topics • Who is eligible for coverage under the health care law? • What is the premium tax credit? • How is the premium tax credit determined?

Major Components of the Affordable Care Act Become Effective January 1, 2014 • Insurance reformsthat allow everyone to purchase coverage • Individual mandate to have coverage • Creation of Health Insurance Marketplaces(Exchanges)to make buying insurance easier • Help paying for insurance • Medicaid expansion • Premium tax credits for low- to moderate-income individuals and families.

Insurance Reforms Will Make Coverage More Accessible • Requirement to sell to everyone • Prohibition from charging more or excluding people based on health status or pre-existing conditions • Premium costs can vary only based on: • Age • Number of people covered in a policy • Geographic area • Tobacco use • Enrollment limited to defined “open enrollment” and “special enrollment” periods

Individual Mandate to Make Insurance Reforms Work • Individuals must have health insurance coverage or pay a penalty • Most existing coverage will satisfy the mandate (e.g., employer-sponsored insurance, Medicare, Medicaid) • Exemptions provided to certain groups, including people who can’t afford coverage • Penalty assessed as a tax

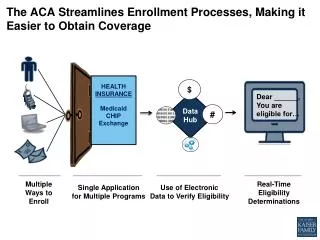

Health Insurance Marketplaces (Exchanges) Will Facilitate Enrollment in Coverage • A place to comparison shop for health insurance • Available in every state • Must be operational by October 1, 2013 for coverage starting January 1, 2014 • Run by state or federal government • Premium tax credits can only be used to purchase coverage sold in the Marketplace

ACA Provides Assistance to Help People Meet the Individual Mandate Medicaid Expansion Premium Tax Credit Income 100 – 400% FPL Available in every state 19 million will use the APTC by 2023 Average exchange subsidy will be $7,900 by 2023 • Expansion to individuals and families with income up to 133% FPL • States decide whether to expand • 13 million newly-eligible enrollees by 2023

Income Eligibility for Programs Determined Using 2013 Federal Poverty Level (FPL) • The FPL is calculated every year by HHS • Sets the precise income standard for determining eligibility for insurance affordability programs

Coverage Landscape in 2014 FPL Unsubsidized 400% 300% 250% Subsidized 185% 200% 133% 100% 61% Coverage Gap Current Medicaid / CHIP Eligibility Expansion 37% 0% Pregnant Women Childless Adults Children Working Parents Jobless Parents Medicaid and CHIP coverage, based on 2012 eligibility levels in a typical state Source: Kaiser Commission on Medicaid and the Uninsured

What Are Premium Credits? • Assistance with the cost of coverage for people purchasing coverage in the new Health Insurance Marketplaces (aka Exchanges) • Provided in the form of advanceable and refundable tax credits • Administered through the tax system and the Marketplaces • Available starting January 1, 2014

What Are the Eligibility Criteria for Premium Tax Credits? • Income between 100% to 400% FPL • US citizenship or lawful present in the US • Must not be eligible for: • Medicare, Medicaid, or most other public coverage • Employer coverage that meets certain requirements • Lawfully residing immigrants with incomes below 100% FPL who are not eligible for Medicaid because of their immigration status • Must file a return for the year in which credit is used • If married, must file a joint return

How Do People Get Premium Credits? • Submit application to the Marketplace for advance payment of credits • Marketplace estimates amount of advance payment based on projected income • Credit is sent directly to insurer, individual pays insurer balance of premium • Can also wait until tax filing and claim on return • Only available for months enrolled in a Marketplace health plan

How Is the Amount of the Tax Credit Determined? • Benchmark plan: Second lowest cost silver plan, as determined by the Marketplace • Expected premium contribution: A percentage of income someone is expected to pay, based on a sliding scale Credit amount = Cost of benchmark plan – Expected premium contribution

John: • Example 1: 150% FPL • Income: $17,235 • Expected Contribution: • Share of income: 4% • Amount: $689 • Premium Credit: $2,329 • Example 2: 250% FPL • Income: $28,725 • Expected Contribution: • Share of income: 8.05% • Amount: $2,312 • Premium Credit: $706 Age: 24 Plan Cost: $3,018

What Is the Benchmark Plan and How Is it Determined? • Second lowest cost silver plan available to each eligible household member • Number calculated by the Marketplace • Might be a single plan to multiple plans added together

Example: Single Individual • John: • 24 years old • Income of $28,725 (250% FPL) • Expected contribution: 8.05% or $2,312 • 3 Lowest Cost Silver Plans Covering John: • Plan A: $2,800 • Plan B: $3,018 • Plan C: $3,200 Benchmark Premium Credit: $3,018 - $2,312 = $706

Example: Family of Four (Reyes Family) Income: $52,988 (225% FPL) Expected contribution: 7.18% or $3,802 • 3 Lowest Cost Silver Plans that Cover Entire Family: • Plan A: $11,500 • Plan B: $12,000 • Plan C: $12,500 Benchmark Premium Credit: $12,000 - $3,802 = $8,198

Example: Household with Multiple Sources of Insurance • Reyes Family • Income: $52,988 (225% FPL) • State has CHIP up to 250% FPL • Mom and dad purchase coverage • Kids on CHIP • 3 Lowest Cost Silver Plans Covering Mom and Dad • Plan A: $7,800 • Plan B: $8,000 • Plan C: $8,200 • Premium Credit: • $8,000 – 3,802 = $4,198 Benchmark

Comparing Two Reyes Family Scenarios Income: $52,988 (225% FPL) Expected contribution: 7.18% or $3,802 Key takeaway: Choice of benchmark plan affects credit amount but not expected contribution

What Factors Affect the Amount of the Credit? • Age • Insurers can charge older people up to 3 times more than younger people • Family size • Geographic area • Health care costs vary by region

John: Age 24 Premium: $3,018 Premium Credit: $1,570 Age 64 Premium: $9,054 Premium Credit: $7,606 Income: $22,980 (200% FPL) Expected Contribution: 6.3% or $1,448

What Factors Affect What People Will Actually Pay for Coverage? • Tobacco use • Insurers can charge tobacco users 50% more • Difference due to tobacco use not accounted for in premium credit calculation • Plan chosen by consumer • Amount of credit pegged to second lowest cost silver plan • But consumer can purchase plans that are more or less expensive

Contact Info www.centeronbudget.org • Tara Straw, tstraw@cbpp.org • Judy Solomon, solomon@cbpp.org