Download

1 / 5

80 likes | 113 Views

Learn the importance of accounting for cash, control methods for cash receipts and disbursements, bank statement reconciliation, and petty cash management. Discover the essential steps to ensure accurate financial records and efficient cash handling procedures in business operations. Enhance your understanding of cash balances, deposits, outstanding checks, and bank reconciliation processes. Improve your control over cash flow and financial reporting with expert insights and practical tips in cash management.

E N D

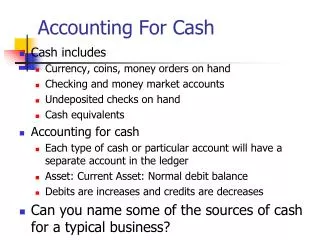

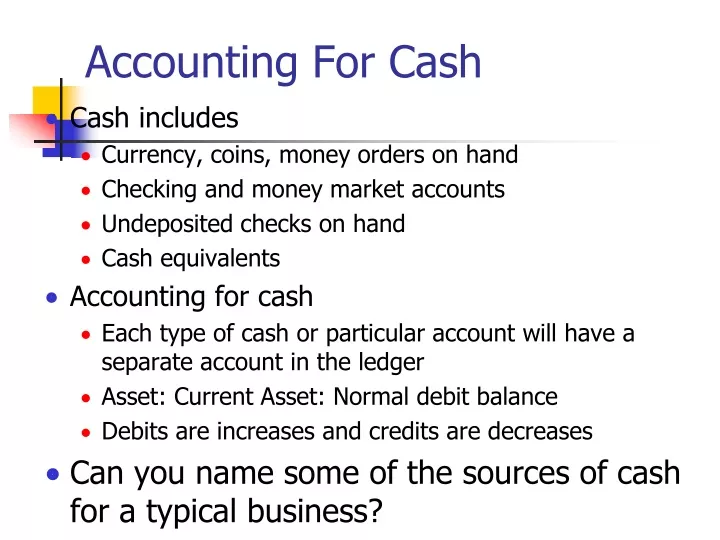

Accounting For Cash • Cash includes • Currency, coins, money orders on hand • Checking and money market accounts • Undeposited checks on hand • Cash equivalents • Accounting for cash • Each type of cash or particular account will have a separate account in the ledger • Asset: Current Asset: Normal debit balance • Debits are increases and credits are decreases • Can you name some of the sources of cash for a typical business?

Control of Cash • Cash Receipts: • Separation of custodial and accounting duties • Cash Registers • Recording cash receipts intact • What does this mean? • Bank statement reconciliation • Analysis of sales returns and discounts

Control of Cash Disbursements • Petty cash fund • Voucher system • All expenditures are paid as the result of submission of an approved voucher with attachments • Proper approval of cash disbursements • Separation of custodial and accounting duties • Bank statement reconciliation • Purchase returns and allowances

Balance per bank 200 Deposits in transit 25 Outstanding checks (15) Correct bank bal. 210 Balance per books 207 Interest earned 5 Bank charges ( 2) Correct book bal. 210 Bank Statement Reconciliation Correction of books would require journal entries Cash 5 and Bank Charges 2 Interest Revenue 5 Cash 2

Petty Cash Transactions • Establishment of the Fund • Debit Petty Cash and Credit Cash in Bank • Disbursements from the fund • Should be receipted and approved by the petty cash custodian • Replenishment of the fund • Debit expense accounts as indicated by the receipts and credit Cash in Bank • Additions (deductions) to the fund • Debit Petty cash for fund increases and credit Petty cash for fund decreases