Download

1 / 6

0 likes | 70 Views

Smartphones and mobile networks will drive banking convenience and internet penetration making it the most important consumer platform for Digital banking in India. Artificial Intelligence has made rapid strides and offers the ability to learn from large amounts of existing data to make more accurate credit-score predictions or product recommendations.

E N D

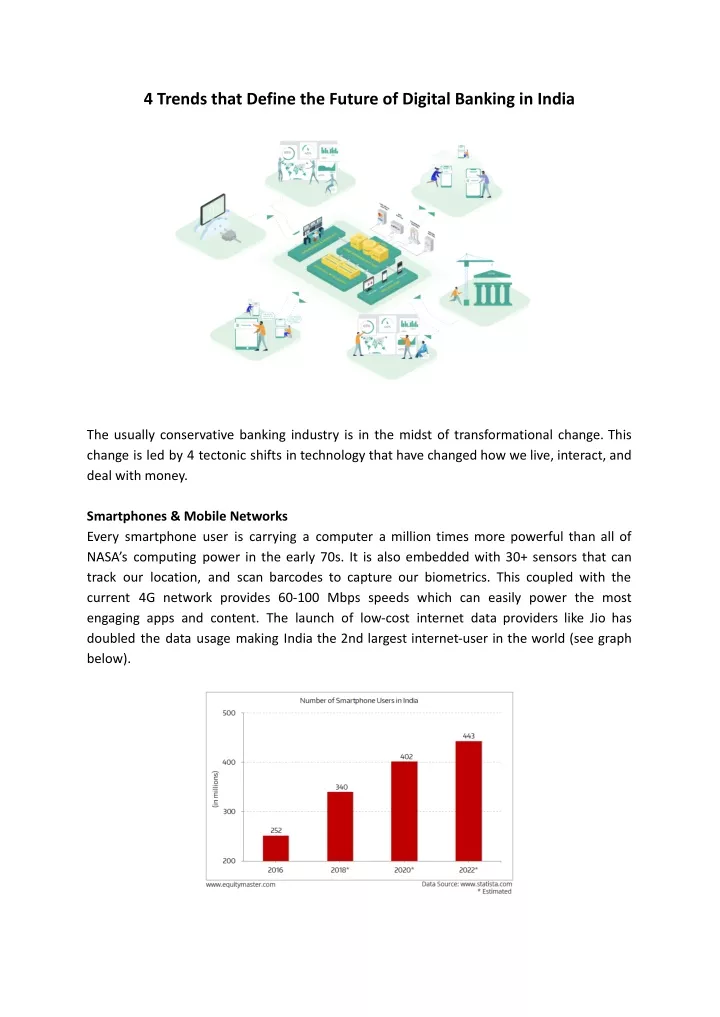

4 Trends that Define the Future of Digital Banking in India The usually conservative banking industry is in the midst of transformational change. This change is led by 4 tectonic shifts in technology that have changed how we live, interact, and deal with money. Smartphones & Mobile Networks Every smartphone user is carrying a computer a million times more powerful than all of NASA’s computing power in the early 70s. It is also embedded with 30+ sensors that can track our location, and scan barcodes to capture our biometrics. This coupled with the current 4G network provides 60-100 Mbps speeds which can easily power the most engaging apps and content. The launch of low-cost internet data providers like Jio has doubled the data usage making India the 2nd largest internet-user in the world (see graph below).

This is the device for banking of the future be it deposit accounts, taking loans, buying insurance or buying mutual funds. You will do all your banking – anytime anywhere on the smartphone. The smartphone sensors can help make your banking personalized and location-specific. Connectivity ensures you can do all your payments and banking activities on the move at your convenience. Mobile alerts and notifications will help keep your money safe and secure. Artificial Intelligence in Banking The last decade has seen huge advances in Machine Learning(ML) algorithms that provide enormous power to transform banking as we know it. The ability of machine learning methods to ingest large amounts of existing data and hence behavior to learn and improve Digital banking in India outcomes has remarkably improved.

According to a McKinsey report, more than half a dozen banks in Europe have already replaced the antiquated statistical-modeling approach with machine-learning techniques, which have resulted in a 10% increase in the sale of new products, 20% savings in capital expenditures and a 20% decline in churn. Credit scoring attempts to predict human behavior when it comes to loan repayment. Traditional credit scoring methods looking at one variable at a time cannot unearth complex hidden relationships between parameters. Deep learning more closely mimicking the human brain can fit the data with more accurate non-linear models that will result in better loan decisions and hence small NPAs (non-performing assets). Other Banking Applications There are several areas where AI has been used in Banking applications and the diagram below highlights the maturity of these applications. API Banking Despite Banks offering smartphone apps and web app frontends to their customers, the future portends a more dynamic way in which the banking products will be consumed. Not all the customers of a Bank’s products will come from the Bank’s Apps be it mobile or Web. Various aggregators, intermediaries, and partners could sell the bank’s lending, insurance, or

investment products through their apps hence bringing in new-to-bank customers dynamically. The weaving of new dynamic services and distribution channels for banking products is possible through APIs – Application Programmatic Interfaces. The new core banking system architecture will need to support APIs that wrap key products to provide your partners with access to the bank offering in a simple yet secure system. These APIs need to be sufficiently granular so that the partner can deliver a differentiated and rich customer experience. A Capgemini Financial Services Analysis study shows that there are several benefits that a Bank accrues when it supports APIs. See the diagram below for a quick summary of the analysis results. Online Authentication and KYC As smartphones grow and become the dominant mode of internet and online access the mobile device with its camera and other sensors allows for more convenient modes of verifying the mobile online customer – be it for authentication or performing KYC. The dominant smartphone platforms of Apple and Google Android have supported built-in biometric authentication using fingerprint or face, which have in turn been used to provide approval for payments be it for app purchase or for other online purchases – as in the case of Apple Pay or Google Pay.

These smartphone-based online verification mechanisms bring enormous convenience literally at people’s fingertips while simultaneously increasing the level of assurance and security. These biometric modes can also be used in conjunction with OTP or pin/password making it a much stronger 2-factor authentication method. The adoption of biometric-based authentication and KYC is increasing in banks the world over. A Deloitte study that highlights the growth of biometrics authentication by US consumers is shown in the diagram. Banks are increasingly performing transactions using an

online device be it a smartphone, tablet, or PC. Both dominant mobile platforms iOS and Android support built-in biometric sensors or attach biometric accessories through a USB cable or a Wi-Fi connection. In India Aadhaar (biometric-based ID) has gained tremendous momentum in seamlessly verifying consumers using biometrics and other methods over smartphones and PC platforms. In the US and other Western economies, the use of biometrics for payment authentication using mobile devices like smartphones has been gaining traction after the launch of Apple Pay on iPhones and other Apple devices, which uses a built-in fingerprint scanner or face-matching system to verify customers instantly. These methods of online authentication and KYC will reduce friction and improve not only the speed of acquiring customers but also product purchase and registration. In Conclusion Smartphones and mobile networks will drive banking convenience and internet penetration making it the most important consumer platform for Digital banking in India. Artificial Intelligence has made rapid strides and offers the ability to learn from large amounts of existing data to make more accurate credit-score predictions or product recommendations. API Banking allows for the bank’s products to be unbundled and distributed using various partners and distribution channels in dynamic ways that the bank in itself would not have reached. Biometric and other online authentication and KYC methods provide for customer verification to happen on the customer’s mobile device, delivering customer convenience but at the same time providing a high level of assurance on customer verification and KYC. The productivity gains of these innovations will also drive down the processing cost, allowing for smaller ticket-size financial products and transactions – hence delivering on financial inclusion. These four megatrends fundamentally change the nature of core banking services and bring a level of automation, convenience, customer focus & productivity that will transform and usher in a much more responsive and differentiated future bank.