Download

1 / 22

• 230 likes • 320 Views

Learn about U.S. Treasury bill and bond futures, EuroDollar time deposits, hedging strategies, pricing mechanisms, and settlement processes in the interest rate futures market. Explore examples and strategies for effective risk management.

E N D

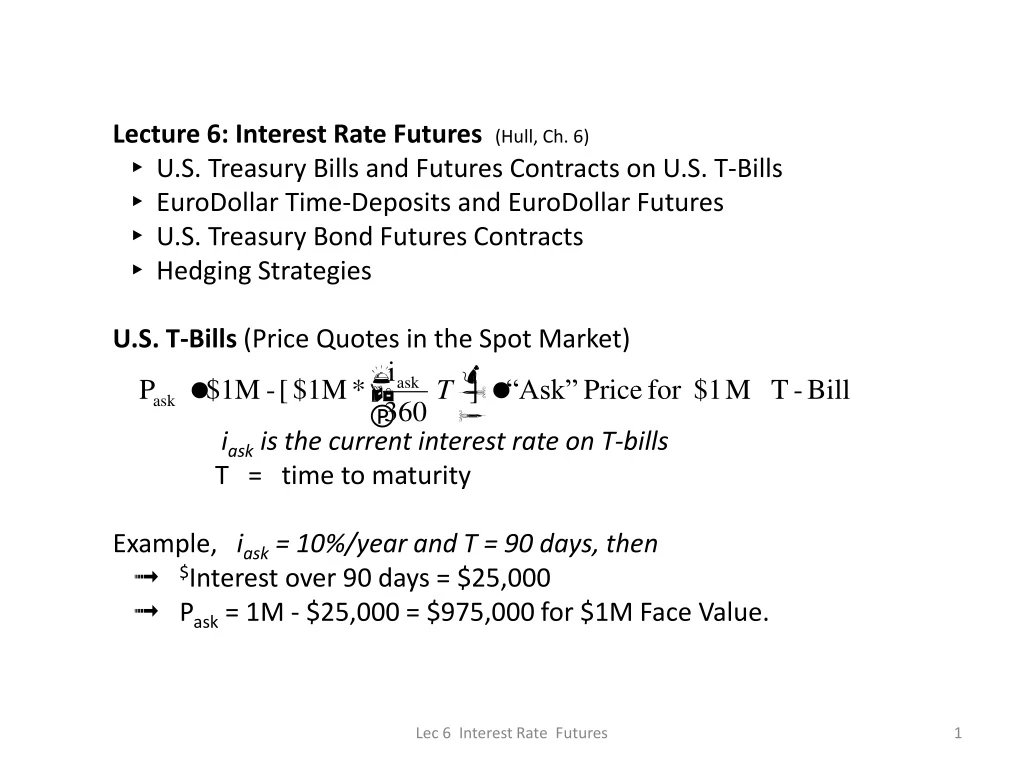

Lecture 6: Interest Rate Futures (Hull, Ch. 6) ▸ U.S. Treasury Bills and Futures Contracts on U.S. T-Bills ▸ EuroDollar Time-Deposits and EuroDollar Futures ▸ U.S. Treasury Bond Futures Contracts ▸ Hedging Strategies U.S. T-Bills (Price Quotes in the Spot Market) iask is the current interest rate on T-bills T = time to maturity Example, iask = 10%/year and T = 90 days, then ➟ $Interest over 90 days = $25,000 ➟ Pask = 1M - $25,000 = $975,000 for $1M Face Value. Lec 6 Interest Rate Futures

U.S. T-Bill Futures Contract Contract: 90-day U.S. Treasury bills Exchange: IMM at CME Delivery: Mar, Jun, Sep, Dec. Contract Size: $1M (FV) Example: Go long one Dec T-Bill futures at IMM index = 90.00 In English, I have agreed to: • Buy $1M (FV) of U.S. T-Bills with 90 days to maturity • actual trade will take place 3rd week in December • IMM index = 90.00 ➟ Forward Rate = (100-IMM index)/100 = 0.10 ➟ Futures Price = $1M { 1 – (0.10/360) x 90} = $975,000 Thus, the Index is like a price: Price of a zero coupon bond with Face Value = $100. if IMM index ↑ Long gains, if IMM index ↓ Long loses. Just like stocks. Lec 6 Interest Rate Futures

Daily Settlement (i.e., Daily Mark to Market) Lec 6 Interest Rate Futures

What Happens at Expiration? Suppose the last Settle IMM = 92.50 ➟ Forward Rate = 100-92.50 = 7.5% = Spot Rate ➟ Spot Price = Futures Price = $1M { 1 – (0.075/360) x 90} = $981,250 Cumulative Δ = $981,250 - $975,000 = + $6,250 ➟ Long gained $6,250, ➟ Short lost $6,250 A. Long Buys T-Bills thru futures. ▸ Long receives $1M (FV) of T-Bills from short. ▸ Long pays $981,250 to short. ▸ But, Long gained $6,250 in the futures market. Therefore Actual cost = 981,250 - 6,250 = $975,000. (Just as originally agreed) Lec 6 Interest Rate Futures

B. Close futures position, and buy in the spot mkt ▸ Go Short 1-Dec-futures at 92.50 (to close long position). ▸ Long pays $981,250 in the spot market. ▸ But, Long gained $6,250 in the futures market. Therefore Actual cost = 981,250 - 6,250 = $975,000. (Just as originally agreed) Lec 6 Interest Rate Futures

Euro$ Time Deposits ▸ U.S. Banks (e.g., BoA) will accept only US dollars for deposits ▸ Banks in London will accept US$ deposits: Euro$ Deposits ▸ LIBOR is the interest rate on these funds Euro$ Futures Contract Contract: 90-day EuroDollar Time Deposit Exchange: IMM at CME Delivery: Mar, Jun, Sep, Dec. Settlement in Cash Contract Size: $1M (FV) Notes 1. The underlying asset is a 90day Eurodollar deposit with FV = $1M 2. Daily “Mark to Market” is exactly the same as for US T-Bill futures 3. At expiration, Euro$ Futures are settled in cash. 4. Futures contracts range in maturity from 1-month to 10 years. Lec 6 Interest Rate Futures

Hedging Example 6.8: Use Euro$ Futures to Hedge Interest Rate Risk ▸ UTC needs to borrow $15M for 3-months (May, June and July). Interest paid monthly. ▸ Monthly interest rate (set at the beginning of each month) = LIBOR + 1% ▸ On April 30, LIBOR = 0.08/yr. ➟ interest due on May 30 = $15M*(0.08+0.01)/12 = $112,500 LIBOR ➀ 0.08 Borrow $15M ➀ $112,500 June Interest = ? July = ? |–––––––––––––––––|–––––––––––––|–––––––––––––––| 0 1 2 3 Apr 30 May 30 Jun 30 July 30 Problem: As of time 0, June and July LIBOR rates are unknown and random. Lec 6 Interest Rate Futures

For example, Assume LIBOR will evolve as follows: • ➁ 0.088 ➂ 0.094 ➀ $112,500 ➁ $122,500 ➂$130,000 • |–––––––––––––––|–––––––––––––––|––––––––––––––––| • 0 1 2 3 • Apr 30 May 30 Jun 30 July 30 • Under this scenario, interest payments will go UP • ➁ June 30 • At t=1 (Beginning of June) monthly LIBOR = 0.088/yr • Interest Pmt due June 30 = $15M*(0.088+0.01)/12 = $122,500 • ➂ July 30 • At t=2 (Beginning of July) monthly LIBOR = 0.094/yr • Interest Pmt due July 30 = $15M*(0.094+0.01)/12 = $130,000 • What to do? Set up a hedge strategy. How? Lec 6 Interest Rate Futures

Hedging Strategy for June: ▸ At t=0 (in April) Short 5 June futures @ IMM_L Index = 91.88 ➟ Forward Rate= (100-91.88)/100 = 8.12% ➟ Notional Value = $1M[ 1 - {0.0812/360} *90 ] = $979,700 ▸ May 30 buy back these 5 contracts.Suppose IMM_L Index = 91.12 ➟ Forward Rate=(100-91.12)/100 = 0.0888 ➟ Notional Value = $1M[ 1 - {0.0888/360} *90 ] = $977,800 Gain/Loss on 5 Futures = - 5(977,800 - $979,700) = + $9,500 Therefore, Unhedged Interest Pmt for June (paid June 30) = $15M*(0.0880+0.01)/12= $122,500 Hedged Interest Pmt = $122,500 - $9,500 = $113,000 ➟ Gains on short futures offset higher Interest Pmt. Lec 6 Interest Rate Futures

Hedging Strategy for July: ▸ At t=0 (in April) Short 5 September futures@ IMM_L Index = 91.44 ➟ Forward Rate= (100-91.44)/100 = 8.56% ➟ Notional Value = $1M[ 1 - {0.0856/360} *90 ] = $978,600 ▸ June 30 buy back these 5 contracts.Suppose IMM_L Index = 90.16 ➟ Forward Rate=(100-90.16)/100 = 0.0984 ➟ Notional Value = $1M[ 1 - {0.0894/360} *90 ] = $975,400 Gain/Loss on 5 Futures = - 5(975,400 - $978,600) = + $16,000 Therefore, Unhedged Interest Pmt for July (paid July 30) = $15M*(0.094+0.01)/12= $130,000 Hedged Interest Pmt = $130,000 - $16,000 = $114,000 ➟ Gains on short futures offset higher Interest Pmt. Lec 6 Interest Rate Futures

In sum: Q: in this example why short 5 contracts? Lec 6 Interest Rate Futures

Hedging Interest Rate Risk Def’n: Duration measures the sensitivity of the bond Price (B0) to changes in interest rates (Δy). This relationship applies to Bond futures also. ⇨ ΔF = - (DF x F0 ) x Δy To immunize a bond portfolio against changes in interest rates, Set ΔB + NF (ΔF) = 0 Lec 6 Interest Rate Futures

In our example, Interest rate changes monthly. ➟ Duration of the $15M bond (loan) =1/12 = 0.0833 years. Duration of the Futures Contract: 90/360 = 0.25 For June Hedge F0= Notional Value (as of April 30) = $979,700 ➟ ΔF = - (DF x F0 ) x Δy = - (0.25 x $979,700) x Δy ➟ ΔB = - (DB x B0 ) x Δy = - (0.0833 x $15M) x Δy Set NF such that [ Δ Bond Portfolio Value ] + NF (Δfutures) = 0 - (0.0833 x $15M) x Δy - NF (0.25 x $979,700) x Δy = 0 NF = - 5.1 Short 5 contract For July Hedge F0 = Notional Value (as of April 30) = $978,600 - (0.0833 x $15M) x Δy - NF (0.25 x $978,600) x Δy = 0 NF = - 5.1 Short 5 contract Lec 6 Interest Rate Futures

US Treasury Bonds : Spot (Cash) Market ▸ Prices in the spot market are quoted as 117-16 ➟ 117+16/32 = $117.50 (per $100 FV) ▸ Cash Price = Quoted Price + AI (seller wants cash for AI) Example: Spot Price is 117-16. CI = $5.50 (per $100) on Jan 10 and July 10 (181 days apart) if you buy this bond March 5, then Invoice Price =117.50+(5.50/181)*54 = $119.14 per $100 If you buy this bond June 30, and Spot Price is still 117-16 Invoice Price = 117.50+(5.50/181)*171 = $122,696 per $100,000 FV Lec 6 Interest Rate Futures

US Treasury Bond Futures Contract: U.S. T-Bond with 15 years to maturity, and 6% CI rate Exchange: CBOT Contract Size: $100,000 Face Value Delivery: Mar, Jun, Sep, Dec. Any day during delivery month Example: Go long one Dec T-Bond futures at 97-18, In English, I have agreed to: • Pay 97+18/32 = $97,562.50 for a U.S. T bond with $100,000 (FV), 15 yrs to maturity and 6% CI • Short will decide the actual delivery day in Dec and the actual bond to sell. Lec 6 Interest Rate Futures

Daily Mark to Market Lec 6 Interest Rate Futures

What Happens at Expiration? Close futures position before Dec 1. Buy Bonds in the spot market. OR (You may Skip the rest below) B. Buy T-Bond thru the futures. Then, Long must pay the following price: Invoice Price = Futures Price*Conversion Factor + AI Explanations: Suppose the last settle Futures price is 94-15. Then, the Futures Price = 94,468.75 Lec 6 Interest Rate Futures

What exactly is a Conversion Factor? Short must deliver bonds with $100,000(FV), 6% CI AND 15 yrs Time to maturity Most likely, Short cannot find one! What to do? Solution: CBOT allows delivery from a wide variety of US T-Bonds. Any coupon rate is okay. Only requirement: 15 or more YTM. For example, consider these two bonds (CI paid semiannually) Bond A: 6% CI (semiannual, FV = $100,000 and 15 YTM. (a long Futures position is the obligation to buy this bond) Bond B: 10% CI rate, FV = $100,000 and 20 years to maturity Lec 6 Interest Rate Futures

Assume a discount rate of 6%/yr. Then, PriceA = $3,000 [PVIFA, 0.06/2, 15yrs*2 ] + + $100,000[PVIF, 0.06/2, 15yrs*2 ] = $100,000 PriceB = $5,000 [ PVIFA, 0.06/2, 20yrs*2 ] + $100,000 [ PVIF, 0.06/2, 20yrs*2 ] =$146,230 Suppose Short wants to deliver Bond B. Should Long pay $100,000 or $146,230? Clearly, Long should pay $146,230 ➟ $146,230 = (same as) 1.4623 * $100,000 Lec 6 Interest Rate Futures

Definition of Conversion Factor Co Fac = {Value of deliverable bond priced to yield 6%} / {Value of underlying bond (Bond A) priced to yield 6%} = = 146,230/ 100,000 = 1.4623 NOTE: The Conversion Factor is just a mechanical formula. It converts a bond with any coupon and any Term to Maturity into Bond A, Assuming a YTM of 6%. Lec 6 Interest Rate Futures

One more complication: Cheapest to Deliver Bond At time of delivery, short has the option to deliver any long term bond. Example: Suppose 3 bonds are available Quoted (spot) Bond Bond Price Conversion Factor X $99.50 1.0382 Y $143.498 1.519 Z $119.75 1.2615 At delivery, to buy any bond in the spot market Short must pay: Invoice Price = Quoted Bond Price + AI To settle the futures, Short delivers this bond and receives: Invoice Price = Futures Price*Conv. Factor + AI Suppose the last Settle Futures Price = 94.46875. Then, the net CF for short is: Net CFX = - $99,500 + ($94,468.75*1.0382) = - $1,423 Net CFY = -$143,498 + ($94,468.75*1.5190) = $0 Net CFZ = -$119,750 + ($94,468.75*1.2615) = - $578 Short will buy and deliver $100,000 FV of bond Y Lec 6 Interest Rate Futures

Thank You (a Favara) Lec 6 Interest Rate Futures