Download

1 / 20

200 likes | 356 Views

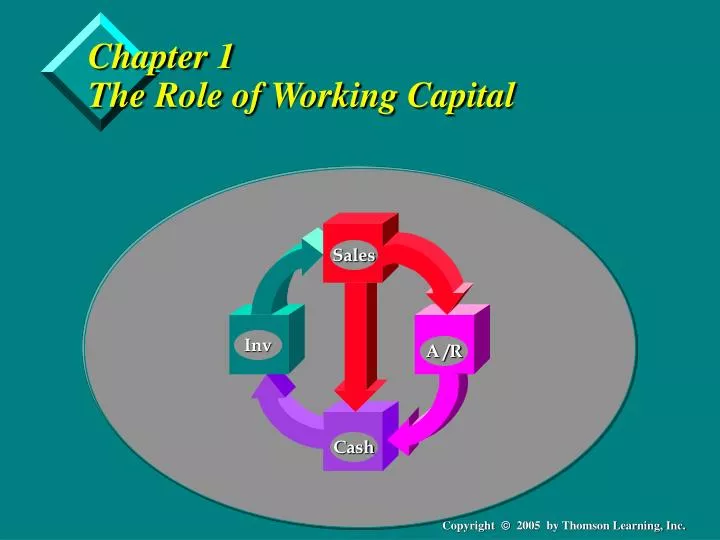

Chapter 1 The Role of Working Capital. Sales. Inv. A /R. Cash. Objectives. View firm as a system of cash flows How WC and depreciation create disparities between profit and cash flow Management aspects of various WC accounts. The Cash Flow Timeline.

E N D

Chapter 1The Role of Working Capital Sales Inv A /R Cash

Objectives • View firm as a system of cash flows • How WC and depreciation create disparities between profit and cash flow • Management aspects of various WC accounts

The Cash Flow Timeline • Order Order Sale Payment Sent Cash • Placed Received Received • Accounts Collection • < Inventory > < Receivable > < Float > • Time ==> • Accounts Disbursement • < Payable > < Float > • Invoice Received Payment Sent Cash Disbursed

...in the beginning • Balance Sheet - June 1 • Cash $1,000 Debt $500 • Common Stock 500 • Total $1,000 Total $1,000

The Next Day, June 2 • Balance Sheet - June 2 • Purchase Fixed Assets (cash) and Inventory (net 45) • Cash $ 400 A/P $ 300 • Inventory 300 Debt 500 • Fixed Assets 600 Common Stock 500 • Total $1,300 Total $1,300

End of June • Balance Sheet - June 30 • Sale of product (net 60), incur operating expenses, • incur depreciation, and generate profit • Cash $ 325 A/P $ 300 • A/R 700 Accruals 200 • Inventory 0 Debt 500 • Fixed Assets 600 Common Stock 500 • (Accum Depr) (100) Retained Earnings 25 • Total $1,525 Total $1,525

July 1 • Balance Sheet - July 1 • Pay operating accruals with cash • Cash $ 125 A/P $ 300 • A/R 700 Accruals 0 • Inventory 0 Debt 500 • Fixed Assets 600 Common Stock 500 • (Accum Depr) (100) Retained Earnings 25 • Total $1,325 Total $1,325

July 15 • Balance Sheet - July 15 • Pay payables with cash • Cash $ ( 175) A/P $ 0 • A/R 700 Accruals 0 • Inventory 0 Debt 500 • Fixed Assets 600 Common Stock 500 • (Accum Depr) (100) Retained Earnings 25 • Total $1,025 Total $1,025

July 31 • Balance Sheet - July 31 • Collect accounts receivable • Cash $ 525 A/P $ 0 • A/R 0 Accruals 0 • Inventory 0 Debt 500 • Fixed Assets 600 Common Stock 500 • (Accum Depr) (100) Retained Earnings 25 • Total $1,025 Total $1,025

Profit versus Cash Flow • Question: Why did the firm end up with $125 in additional cash while earning a profit of $25? • Answer: Some expenses are not cash expenses. • Question: Why did the firm run out of cash during its operating cycle? • Answer: The cash deficit was due to the differences between the timing of cash disbursements and cash receipts.

Important Points • The firm must manage its cost structure to generate a profit • WC accounts must be managed so that liquidity is maintained.

Relationship Between Accrual Income and Cash Flow (example) Income StatementAdjustment AccountCash Flow Account Sales - Change in accounts receivable = Cash collected from customers Cost of goods sold - Change in accounts payable + Change in inventory = Cash paid to suppliers Operating expenses - Change in operating accruals (including Dep.) - Depreciation = Cash paid for operating expenses Interest - Change in accrued interest = Cash paid to creditors Taxes - Change in accrued taxes - Change in deferred taxes = Cash paid for taxes _________________ ___________________ Net Profit Operating Cash Flow

Managing the Cash Cycle • Managing Inventory- slide 14 • Managing Receivables- slide 15 • Managing Payables- slide 16 • Electronic Commerce - slide 17

Managing Inventory • JIT • Trade-offs between: • stock out costs • cost of excess inventory • ordering costs

Managing Receivables • Who should receive credit and how much? • Credit terms • Monitoring the outstanding balance • Speeding up the receipt of payments through lockboxes

Managing Payables • Search for terms that match with cash receipts • Timing of payment • Controlled disbursement

Electronic Commerce • Revolutionizing management of cash cycle • Proprietary systems • Impact of Internet

How Much WC is Enough • One view • optimal level is zero • WC is an idle resource • Provides little value • How much in resources to commit? • Why inventory? • Why receivables and payables? • Why short-term investments? • Chrysler’s $5 billioin cushion of investments

Summary • Firm must operate at a profitable level. • A profitable firm may still struggle financially. • Working capital soaks up cash flow and may cause an otherwise profitable firm to fail. • A successful firm’s operation is managed from a • profit, and a • cash flow perspective.