Download

1 / 21

210 likes | 324 Views

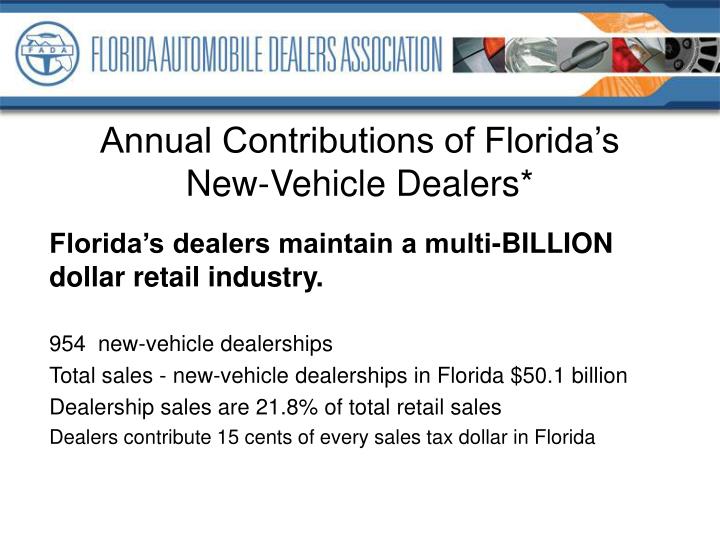

Annual Contributions of Florida’s New-Vehicle Dealers*. Florida’s dealers maintain a multi-BILLION dollar retail industry. 954 new-vehicle dealerships Total sales - new-vehicle dealerships in Florida $50.1 billion Dealership sales are 21.8% of total retail sales

E N D

Annual Contributions of Florida’s New-Vehicle Dealers* Florida’s dealers maintain a multi-BILLION dollar retail industry. 954 new-vehicle dealerships Total sales - new-vehicle dealerships in Florida $50.1 billion Dealership sales are 21.8% of total retail sales Dealers contribute 15 cents of every sales tax dollar in Florida

Annual Contributions of Florida’s New-Vehicle Dealers* Dealers provide thousands of well-paying jobs in Florida. • 77,314 new-vehicle dealership employees in Florida • $3.8 billion in total annual payroll of new-vehicle dealerships • 13% of total state retail payroll • Dealerships are many times one of largest employers in a locality

DEP Workshop – December 5, 2007 As a major economic engine in Florida’s economy we want a clean environment for the citizens of Florida today and for future generations We recognize that Florida should be a leader and should be a pace-setter among the states because of our size and geo-political importance.

DEP Workshop – December 5, 2007 • We heartily endorse action to enable Florida to become more energy efficient and the US more energy independent and less reliant on foreign sources of oil. • We also support rigorous but achievable fuel efficiency standards and actions which will stimulate more technological advancements by our manufacturer partners as long as expectations due not disrupt Florida consumers’ vehicle choices (availability) or affordability • Many of the new cars we sell today meet federal standards for cleaner operation.

What the Florida Marketplace Looks Like To understand the impact of CAL-LEV on Florida lets take a look at what Floridians drive today -

FLORIDA REGISTERED PASSENGER CARS“ON THE ROAD”July 2007 Cars: 7,988,884 Source: AutoCount by Experian Automotive

FLORIDA REGISTERED TRUCKS , VANS AND SUVS“ON THE ROAD”July 2007 Trucks/SUVS: 6,958,157 Source: AutoCount by Experian Automotive

FLORIDA REGISTERED VEHICLES “ON THE ROAD”July 2007 Total vehicles: 14,947,041 Cars: 53% Trucks: 47 % Source: AutoCount by Experian Automotive

FLORIDA NEW VEHICLE SALES 2006 Total Vehicles: 1,045,906 Cars: 50% Trucks/SUV: 50% Source: AutoCount by Experian Automotive

FLORIDA NEW VEHICLES SALES 2006 Of Total Sales: # 1,045,906 Non-Hybrid Top Ten Sales: # 183,103 / 18% *Carbon Footprint/avg. tonnage per year: 8.7 Hybrid Top Ten Sales: # 12,916 / 1% *Carbon Footprint/avg. tonnage per year: 7.1 *The carbon footprint measures greenhouse gas emissions expressed in CO2 equivalents. The estimates presented here are "full fuel-cycle estimates" and include the three major greenhouse gases emitted by motor vehicles: carbon dioxide, nitrous oxide, and methane. Full fuel-cycle estimates consider all steps in the use of a fuel, from production and refining to distribution and final use. Source: AutoCount by Experian Automotive and www.fueleconomy.gov

DEP Workshop – December 5, 2007 We support action to curtail GHG emissions and we believe that Florida should consider a host of initiatives that would include : reducing miles driven by Florida motorists new incentives for mass transit solutions, ride sharing, etc. vehicle inspections - reductions in emissions from used vehicles on Florida roads and highways since 90% of our vehicular traffic is “used” and less efficient automobiles market driven incentives for consumers who purchase fuel-saving vehicles (tax credits for new car purchases from funded program)

DEP Workshop – December 5, 2007 Market driven incentives to remove 14 million older vehicles on Florida highways A fuel efficiency standard that is achievable Incentives for other techno advances such as clean diesel, alternative fuels and other new technologies A phased in approach that recognizes the huge impact on Florida driving patterns and seeks to affect Vehicle Miles Driven rather than vehicle choice As we await action from the EPA on the waiver, we would emphasize the need to consider all options rather than placing the entire emphasis on fuel efficiency

DEP Workshop – December 5, 2007 There is no harm in going slowly and assessing all costs and benefits – California took 2-3 years to implement their regulations Lastly, we believe a major component of this regulatory framework should be a massive public education effort with town hall meetings conducted around the state to get feedback from our customers on vehicle choices and lifestyle needs

DEP Workshop – December 5, 2007 The Dealer’s focus is on vehicle availability and affordability While we do not speak for the manufacturers we are troubled about their testimony regarding their options under the CAL-LEV guidelines as the result may be: Fewer vehicles allocated to dealers Inability to meet our customer’s lifestyle choices or safety needs Impacts such as pre-implementation sales bonanza followed by sales delays due to higher pricing Sales shift to sellers outside Florida and our sales tax revenue is impacted (sales across borders or Internet)

DEP Workshop – December 5, 2007 Dealer concerns include: Affect on sales as Florida cars add $1,500 to $3,000 to costs of vehicles –slowing purchase of new cars Buyers respond to sellers in neighboring states, Internet sellers, buyers from other states register vehicles there and Florida law creates opportunity for auto brokers If Florida regulations create registration denials and a 7500 miles driven requirement, Florida dealers will lose the benefit of dealer trading network

DEP Workshop – December 5, 2007 • Of the approximately 13.4 million vehicles registered in Florida in 2006, only 10% or fewer were new vehicles. Forcing citizens to remain in older vehicles does not take advantage of newer technologies. • Florida consumers with other state domiciles will react to higher taxes by purchasing in their home state rather than Florida and will not register their vehicles here.

DEP Workshop – December 5, 2007 • Vehicle purchases across state lines will directly impact Florida sales tax revenues. Purchases in Alabama reduce Florida taxes received upon vehicle registration by 2%. With 50% of Florida vehicle sales consisting of light trucks and SUV’s, the potential negative impact could easily reach $50 million in lost revenues.

DEP Workshop – December 5, 2007 • FADA is also concerned about abdication of all rulemaking, leaving Florida consumers exposed now and in the future to California regulatory standards • We would urge that regulatory timeframes take into consideration the likelihood of an EPA waiver denial, especially given the passage of a new Congressional CAFE bill

DEP Workshop – December 5, 2007 • FADA is deeply concerned about the economic health and stability of automakers so we urge caution as options are explored • With so much pressure on DEP and due to the complexity of this concept we feel that the Florida legislature should ultimately be the focal point for these discussions, as this represents a broad policy change

This association stands ready to work with you to develop proposals that are consistent with the overall goal of emission reductions but that also respond to the needs and economic realities of our great State. DEP Workshop – December 5, 2007