Download

1 / 3

40 likes | 597 Views

Approaches to Econometrics Forecasting AR, MA, and ARIMA Modeling of Time Series Data The Box-Jenkins (BJ) Methodology Identification Estimation of the ARIMA Model Diagnostic Checking Forecasting Further Aspects of the BJ Methodology Summary and Conclusions . 22- Time Series Econometrics F

E N D

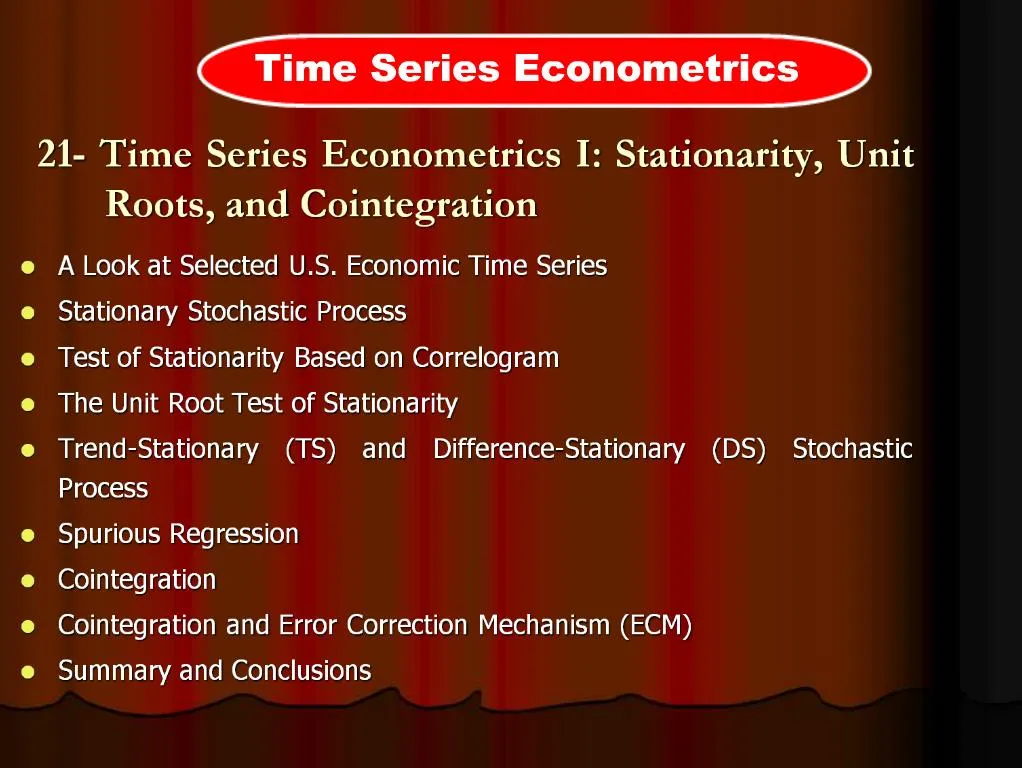

1. A Look at Selected U.S. Economic Time Series

Stationary Stochastic Process

Test of Stationarity Based on Correlogram

The Unit Root Test of Stationarity

Trend-Stationary (TS) and Difference-Stationary (DS) Stochastic Process

Spurious Regression

Cointegration

Cointegration and Error Correction Mechanism (ECM)

Summary and Conclusions 21- Time Series Econometrics I: Stationarity, Unit Roots, and Cointegration

2. Approaches to Econometrics Forecasting

AR, MA, and ARIMA Modeling of Time Series Data

The Box-Jenkins (BJ) Methodology

Identification

Estimation of the ARIMA Model

Diagnostic Checking

Forecasting

Further Aspects of the BJ Methodology

Summary and Conclusions

22- Time Series Econometrics Forecasting with ARIMA and VAR Models

3. A- A Review of Some Statistical Concepts

B- Rudiments of Matrix Algebra

C- A List of Statistical Computer Packages

D- Statistical Tables

Selected Bibliography

Indexes

- Name Index

- Subject Appendixes