Download

1 / 25

250 likes | 420 Views

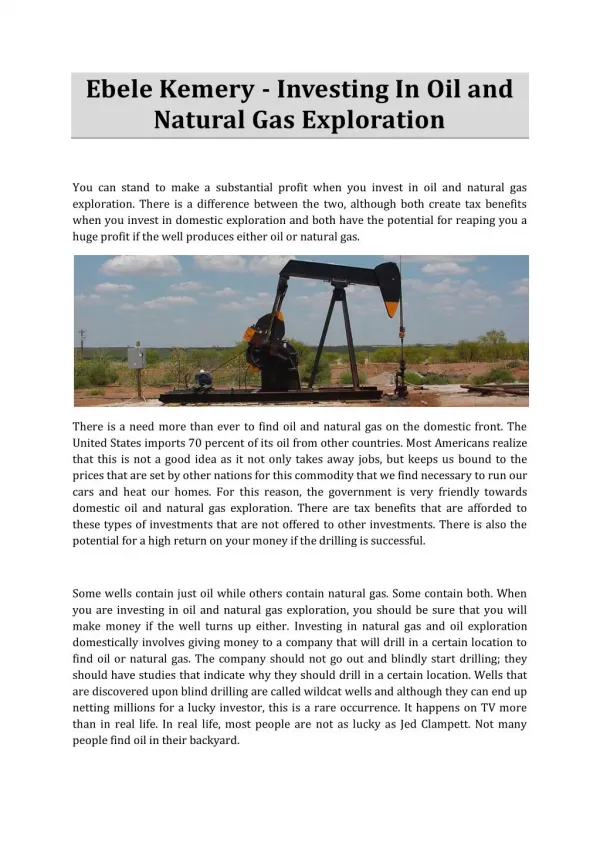

Presentation to the IPAA Private Capital Conference January 19, 2006. Investing in Growing Oil and Gas and Midstream Energy Companies. GasRock Capital LLC. Development drilling projects and midstream gas “Mezzanine” debt with royalty or other participation Start-ups to large companies

E N D

Presentation to the IPAA Private Capital Conference January 19, 2006 Investing in Growing Oil and Gas and Midstream Energy Companies

GasRock Capital LLC • Development drilling projects and midstream gas • “Mezzanine” debt with royalty or other participation • Start-ups to large companies • Engineering risk rather than exploration • $5 to $50 million +

Investment Focus • Oil and gas development drilling projects and acquisitions • Typically at least a small amount of PDP reserves to start • Substantial PDNP and PUD development opportunity • Some types of exploitation (Probable) may be acceptable • Very low risk PUD development projects may not require initial PDP • Midstream gas • Gathering, processing, pipelines • Other toll based business Focus Knowledge

Targeted Risk Profile Target Investments

What We Want • Usually some PDP • Initial collateral value comparable to first advance • Exceptions for some projects like coal seam gas • Development project risk • Significant PUD drilling opportunity; not exploration • Also mid-stream gas assets • Total return: more than bank debt, less than equity • Coupon usually 9% to 11% • Royalty in adequate size to reach target return, based on risk • Some owner / sponsor investment • Needs to be significant to the individuals, not to the project • Lien on the assets • Typically first lien; will accept second lien in larger deals

What You Get • Early stage capital • No fixed minimum equity investment • Focused on quality project, not long track record • Fast growth • Substantial development capital • Much larger and faster advance than bank • Non-recourse • Debt and liens in project company only • Other assets/projects unencumbered • Control • Generally no sale of equity (e.g. majority) • No board seats or control of acquisitions or divestitures • Nearly all of the upside • GasRock usually keeps ORRI only • After debt paid, nearly all cash flow reverts to sponsor

Typical Investment Structure • First lien debt • Coupon • ORRI • Advances • Repayment • Pay off any other debt with proceeds • Lien on all assets in the project • Usually 9-11% • Floating rate with fixed minimum rate • Current pay; will consider funding early coupons if needed • Royalty sized as required to meet target return • Sizing based on project economic model • May begin immediately or after loan repaid • Based primarily on PDP value • May equal or exceed PV10 • Typically sponsor pays for leases, seismic • Proceeds applied to approved development plan • “Sweep” of cash flow to pay interest and principal • Typically 80%-90% • Structured to accommodate overhead • 3 to 4 year maturity • Early repayment allowed; no penalty

Benefits of Project / Mezzanine Finance “Project financing allows companies to grow rapidly without giving up a big share of their economics or control of their future.” Accelerated Funding • Often two to three times bank advance • Faster increase as wells come on • Much faster project growth Reasonable Cost • Higher than bank debt; lower than equity • Applies only to specific project assets • Prepay at any time Retained Control • No sale of a share of ownership • No board seat • No control over sale of company, IPO, etc. + +

Choose Experience and Knowledge • Our four transaction leaders average 24 years of experience • Engineering knowledge results in speedy evaluations • Greater surety of closing, without change in terms • Appreciation of potential results in • Aggressive terms • Patience for results • Experience helps in crafting unique structures tailored to specific needs

Choose People You Can Trust • Project financing is relatively hands-on • Pick someone you can live with • Shared perspective from history working on behalf of operators • Reasonable and balanced approach • Reputation for persistence and creativity

How We Are Different • Ability to start small (under $5 million) • Yet can grow large ($50+ million) • Long on energy deal experience • Creative, responsive, and quick

Portfolio Company • First GasRock Deal • Closed in 28 days • Initial funding about one-third • Balance for development • Workovers • Recompletions • Drilling

Case Study: Mythos, Inc. • Owns a largely undeveloped field • Type Well: • Net reserves: 572 MMCF • Cost to drill: $650k • R/P ratio: 8.5 • Life: 25+ years • IRR: 35% • ROI: 4.5 • Payout: 2.5 years

Case Study: Mythos, Inc. • Some PDP • 3 wells drilled so far • PV10: $4.4 million • Production: 400 MCFD • Undeveloped acreage • 72 locations • 42+ BCFE net reserve potential • $47 million, two-year drilling program • Project Economics • Field level IRR: 37% develop and hold 76% develop and sell • Sale price: $87.4 million in 30 months

Mythos: Options for Growth • Bank debt • Industry joint venture • Private equity • Mezzanine

Mythos: Bank Debt • 7% interest rate • Advance equals 60% of PDP • Semi-annual borrowing base re-determination • Slower drilling

Mythos: Industry Partner • One eighth carry through all 72 wells • Carried on all CAPEX (“to the tanks”) • No constraint on pace of drilling • Partner IRR is 31%

Mythos: Private Equity • Raise $20 million of institutional equity • Plus a little bank debt • Mythos contributes PDP for 14% of equity • PDP valuation at $8000 per mcfe/d of production; $2.34/mcf • Mythos can ‘claw-back’ to 34% of equity • Assumed sale after 30 months • Results in equity investor IRR 50%; ROI 3.4

Mythos: Mezzanine • $47 million facility • 10% coupon • 5% ORRI • 2% advance fee • 90% sweep of field profit • Mezzanine earns 18.5% IRR • ROI is 1.5 over 4.5 years without sale • 23% IRR with sale in 2.5 years

Case Study: Sharing the Profit Management retains a larger share of the profit with mezzanine financing as compared to alternatives.

Summary • Accelerate funding and development • Avoid dilution of equity ownership • Maintain control • Capture a larger share; finish strong!

Contacts Houston • Frank M. Weisser • 713-425-7052 • fweisser@gasrockcapital.com • Scott W. Johnson • 713-425-7051 • sjohnson@gasrockcapital.com • David R. Taylor • 713-425-7053 • dtaylor@gasrockcapital.com • Marshall Lynn Bass • 713-425-7056 • lbass@gasrockcapital.com 1 Houston Center 1221 McKinney Suite 3180 Houston, TX 77010-2026 713-300-1400 Fax 713-300-1401 www.gasrockcapital.com